Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Growing pains, roaring 20s, or stagflation? Revisiting our scenarios

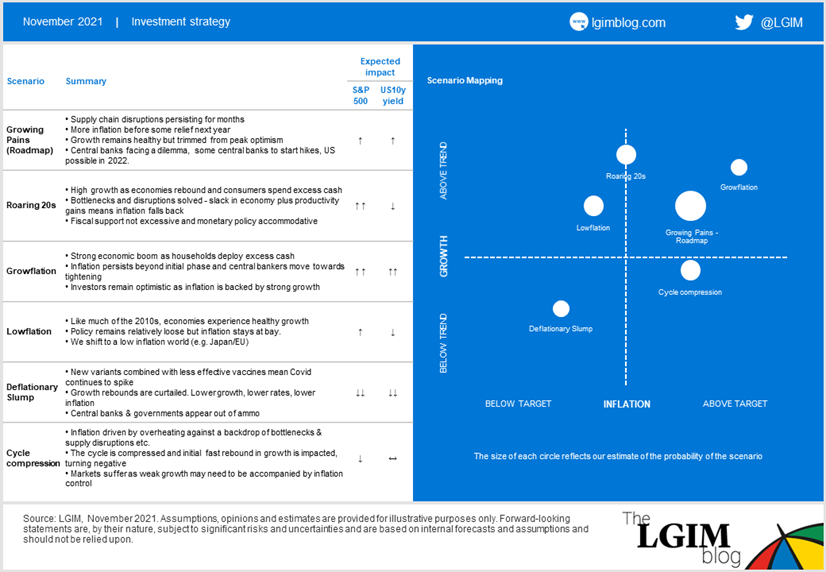

We are macro investors, and as such always try to look at market developments through that broader lens rather than focusing on new information in isolation. Individual inflation prints are interesting, for example, but what do they tell us about the broader inflationary environment and the associated implications for assets?

To help us answer such questions, we conduct regular scenario analysis and planning. As we described in July, we begin by discussing the potential scenarios that could shape the market narrative in the months ahead. We then estimate their likelihood of occurring and their probable impact on market prices.

So, what is our current thinking?

When we frame markets like this, we can look through individual data points and see there isn’t a great deal of cause for alarm – roughly only a 30% probability of us being in a scenario with negative implications for equities. That’s well below a typical average where the probabilities of negative equity returns are more finely balanced.

Admittedly, since the summer, uncertainty has risen again with supply chain difficulties and rising Covid cases across Europe that are leading to partial lockdowns and restrictions. The ‘cycle compression’ scenario – which can be seen as stagflation – attracts a lot of headlines, but in our view it should be considered alongside other more positive scenarios with higher probabilities of transpiring.

Travel towards such a scenario would put us in a late-cycle environment, and even there, our view isn’t necessarily negative for risk assets as long as recession risks remain very low, as they do today. We are wary of taking off risk too soon, and scenario analysis helps us back up that view.

Broad diversification will help, no matter which eventuality plays out – but as the majority of the possible outcomes are connected to above-trend growth, we are staying positive on equities for now.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.