Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Gold and the rates cycle – the outlook for 2025

Reduced expectations of rate cuts could represent a headwind, but central bank buying remains a support, and earnings suggest miners are reaping the rewards of a higher gold price.

My previous gold update came a month after the onset of the rate-cutting cycle in the US. Since then, expectations of future rate cuts have been revised down rapidly amid strong economic data.

Against this backdrop, here are the key factors we believe will influence the outlook for gold in 2025.

The macro picture

Markets are pricing only one or two rate cuts in the US this year, given robust jobs growth and sticky inflation. Fewer predicted rate cuts means that treasury yields have risen, which could act as a headwind for gold. This is because of the inverse relationship between the metal and the US dollar: higher interest rates can be expected to strengthen the dollar, which generally weakens gold.[1] A big ‘if’ here is the dollar – will it continue to dominate its rivals in 2025?

President Trump's policies represent another major unknown, alongside ongoing global geopolitical volatility. This uncertain landscape could potentially provide support for gold as a perceived safe-haven asset.

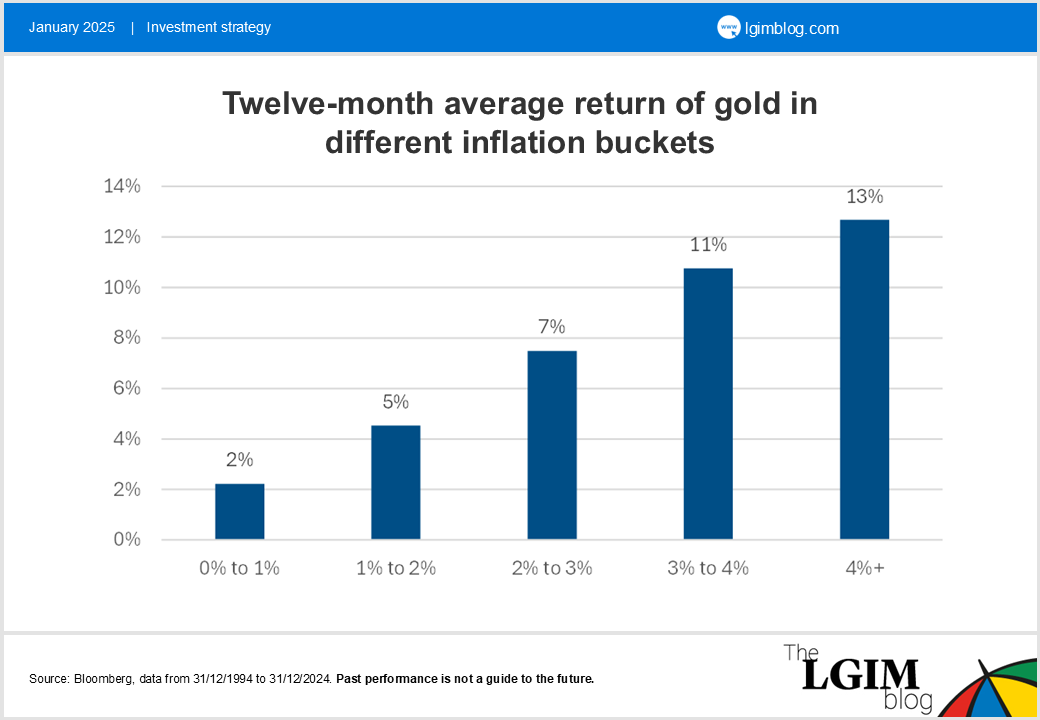

The sustainability of US debt, which has ballooned to $36tn, is a growing concern, especially with anticipated inflationary pressures under Trump's administration. This could turn into a tailwind for the precious metal, given its value generally rises with inflation. As shown below, gold has historically performed best during periods of high inflation.[2] The December US CPI print was 2.9%, above the Fed’s 2% target.

Central bank buying

Central banks, particularly China’s, continue to play a pivotal role in the gold market. In Q3, gold demand surpassed $100bn for the first time, highlighting the metal's enduring appeal as a store of value.[3]

Central banks are adding gold to their reserves, recognising its historic performance during crises and its lack of credit risk amid rising sovereign debt and geopolitical uncertainty.

China, in particular, is striving to reduce its exposure to the US dollar amid trade tensions with the US. In 2023, the People's Bank of China recorded the largest increase in gold reserves, adding 225 tonnes. The share of gold in China’s total foreign exchange reserves has risen to 6%, up from 4.6% at the beginning of last year.[4] And, despite high gold prices, it continued its buying spree in Q4.[5]

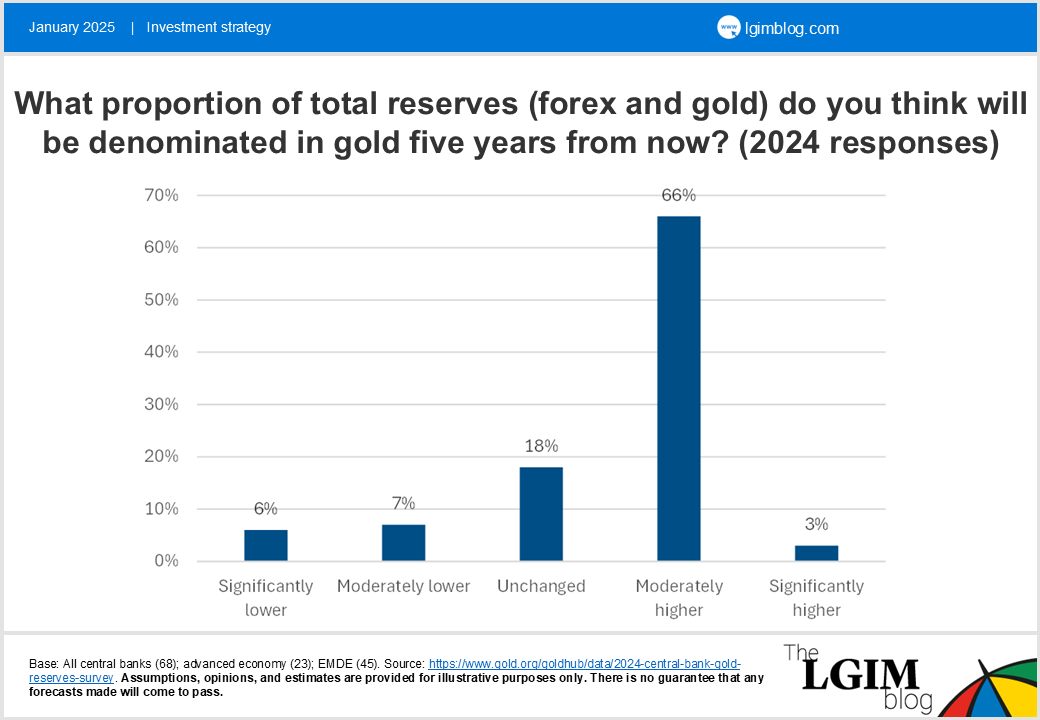

As shown below, central banks’ expectations of their own gold buying has steadily risen over the past few years.

Company-specific developments

The gold mining sector is, in our view, ripe with potential value opportunities and significant M&A activity. In Q4, several high-profile transactions underscored the sector's dynamism:

- Northern Star Resources* announced the acquisition of De Grey Mining* for over $2.5bn , at a 40% premium.

- Anglogold Ashanti* completed the acquisition of Centamin* for over $2.5bn, at a 38% premium.

- Gold Fields* acquired Osisko Mining* for over $1.3bn, becoming the sole operator of the Windfall project in Quebec, which would rank among the top 10 highest-grade mines globally if in production today.

From a financial perspective, the gold mining sector is experiencing robust earnings and revenue growth, supported by the gold price. Two-thirds of companies have reported Q3 results, with most showing double-digit growth. More companies are expected to report in February, with double-digit growth anticipated for at least the first half of 2025.[6]

We continue to believe gold mining equities provide a potentially useful way of expressing a view on the direction of the gold price with additional beta.

For these investors, we’d stress the importance of identifying a basket of miners with a pure focus on gold, and weighting exposure on actual gold production rather than straight market capitalisation. This aims to maximise the purity of exposure to the gold price while mitigating the impact of other minerals and company-specific factors that may be more strongly correlated with global industrial production and broad equity market performance.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an LGIM portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Past performance is not a guide to the future.

[2] Past performance is not a guide to the future.

[3] Source: https://www.gold.org/news-and-events/press-releases/global-gold-demand-reaches-record-high-value-over-us100-billion

[4] Source: Central Banks Gold Reserves by Country | World Gold Council

[5] Source: PBOC, Bloomberg, as at January 2025.

[6] Source: Bloomberg as at 20 January 2025.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.