Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

ETF misconceptions: three myths busted

In the first instalment of a three-part series, we unpick three common ETF misunderstandings.

The exchange traded fund (ETF) market has recorded remarkable growth in recent years, with European ETFs recording $162 billion of inflows in 2021 alone.1 This surge of inflows was supported in part by the market’s weathering of the March 2020 storm, which shows the potential of ETFs to trade even amid extreme market disruptions.

Investors are increasingly exploring ETFs as they seek convenient and economic market access, but the product has also inevitably faced criticism. Like all investments, ETFs entail risks as well as opportunities, some of which stem from the investment structure and others that stem from the underlying assets.

Let’s investigate three common charges levelled against ETFs, and find out if the criticisms hold water.

Misconception 1: ETFs are unsuitable for long-term investors

One of the defining features of ETFs is that they offer intraday trading. However, some argue that the ability to buy and sell ETFs with minimal lag encourages a short-term trading mentality rather than a long-term investor mindset.

In reality, however, the liquidity of ETFs does not make them any less suitable as long-term investments. Just like mutual fund holdings, ETFs can be held for the long term. But, in times of market distress like the pandemic or the war in Ukraine, ETF investors have the option to enter and exit their positions quickly during market hours.

Misconception 2: ETFs aren’t liquid

‘Liquidity’ means the ease with which investors can buy and sell their holdings. But when it comes to ETFs, this is frequently misunderstood. For instance, the average daily volume (ADV) of an ETF is often cited as the gauge of an ETF’s liquidity, but looking at the ADV alone could be misleading. The true liquidity of an ETF resides in its underlying, and only this can tell you how easy it is to buy into or sell out of the ETF.

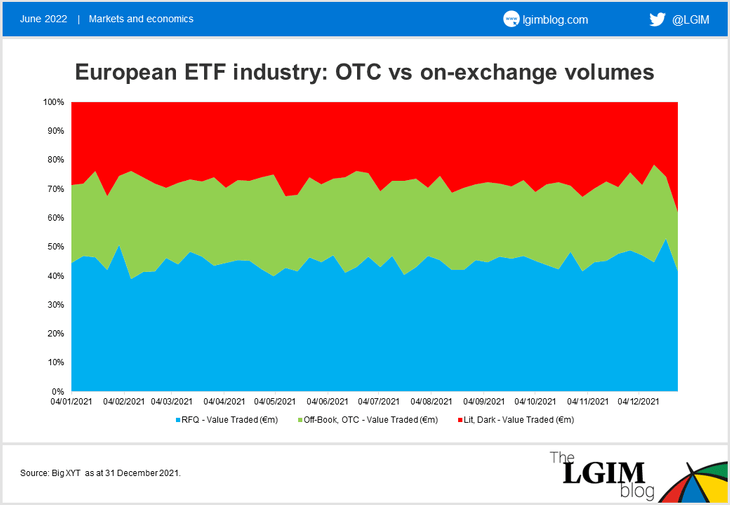

On-exchange volumes represent only 20-25% of the total volume traded in the ETF European market, with the remaining 75-80% trading over the counter (OTC) via request for quotes (RFQ) platforms (e.g., Tradeweb and Bloomberg ).2 This suggests that most liquidity in the ETF market cannot be captured using metrics such as ADV, but is still very much present.

The graph below shows the proportion of on-exchange flows versus OTC for the ETF European industry in 2021. It is evident that the majority of flows take place OTC via RFQ platforms or off-book (approximately 70%).

‘Lit’ markets and ‘dark’ markets are types of stock exchanges. Dark venues do not provide visibility on the prices at which market participants are willing to trade, whereas lit venues show the various bid and offer prices.

Additionally, if secondary market liquidity is not enough to absorb new orders, ETF authorised participants (APs) can access the primary market to create additional shares or redeem existing shares. APs play a significant role by providing an additional layer of liquidity in the ETF market.

Misconception 3: ETF spreads are confusing

Understanding ETF spreads is essential, as this is the price you pay to trade an ETF. The ‘spread’ is the difference between the bid price and the ask price. The ‘bid’ is the highest price at which a buyer is willing to purchase ETF shares, and the ‘ask’ is the lowest price a seller is willing to accept to sell. The wider the spread, the more expensive the ETF is to trade.

Many factors determine the spread, which we believe investors should consider when comparing ETFs. ETFs with tighter spreads on-exchange usually have larger assets under management (AUM), more market participants on the order book (which increases price competition between market makers), and higher trading volumes on exchange. ETFs with wider spreads tend to have much smaller AUMs, fewer market participants on book and lower volumes on-exchange.

It is possible, however, that ETFs with lower AUMs can still benefit from tighter spreads. If an ETF’s underlying basket can be easily hedged against and there are many hedging instruments available a lower AUM ETF may still have a tight spread. The easier it is to hedge against an ETF’s underlying, the tighter the spreads market makers can quote as the risk for market making in that ETF is perceived to be lower. Current market conditions will also influence spreads. During times of market volatility, spreads will usually widen to account for additional market risk.

In part two of this blog series, we will turn to ETF misconceptions surrounding the total cost of ownership.

1. Source: https://www.etfstream.com/features/european-etf-industry-outlook-2022/

2. Source: Big XYT, as at 31 December 2021

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.