Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Equity valuations uncovered (part 3): Short-term insights

A common refrain is that valuations are irrelevant over short horizons, but that they become strong predictors in the longer term. What motivates such statements and is there any truth in them?

The first cut is the deepest

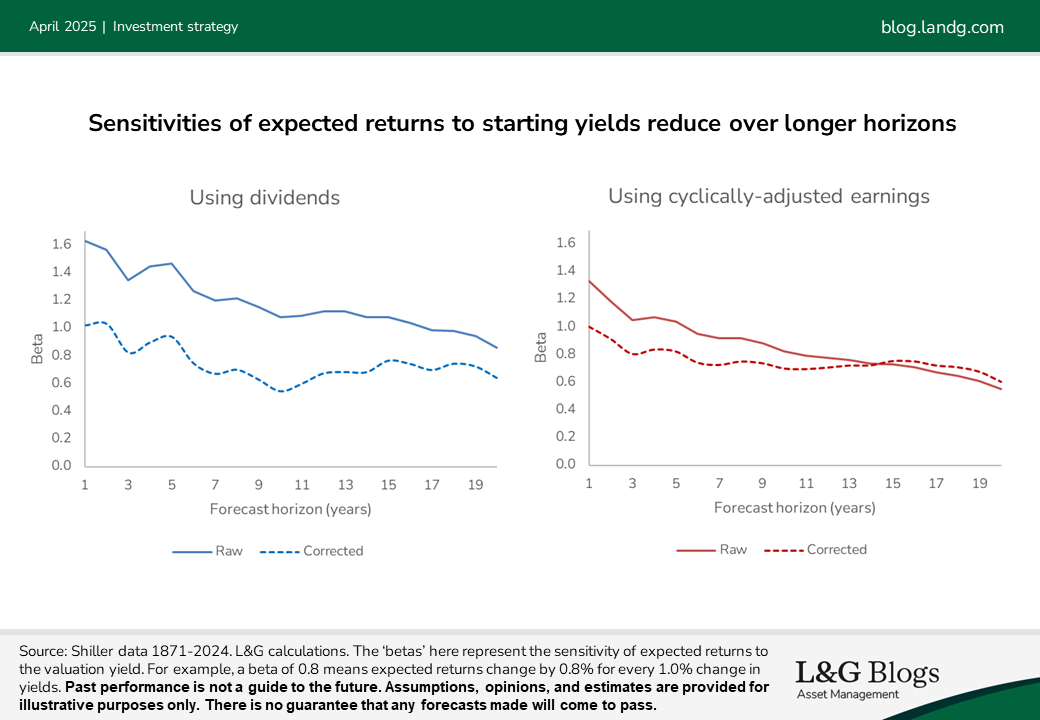

In a previous blog I presented the following charts. They indicate the sensitivity of expected returns to starting valuation yields over different forecast horizons. The good news is that they suggest that valuations are still useful for setting expected returns on equities, even after correcting for statistical biases.

Putting aside some wiggles, you’ll note that the dotted lines are downward sloping. This implies the sensitivity of expected returns to valuations is greatest in the short run.

Lowly correlated yet highly committed

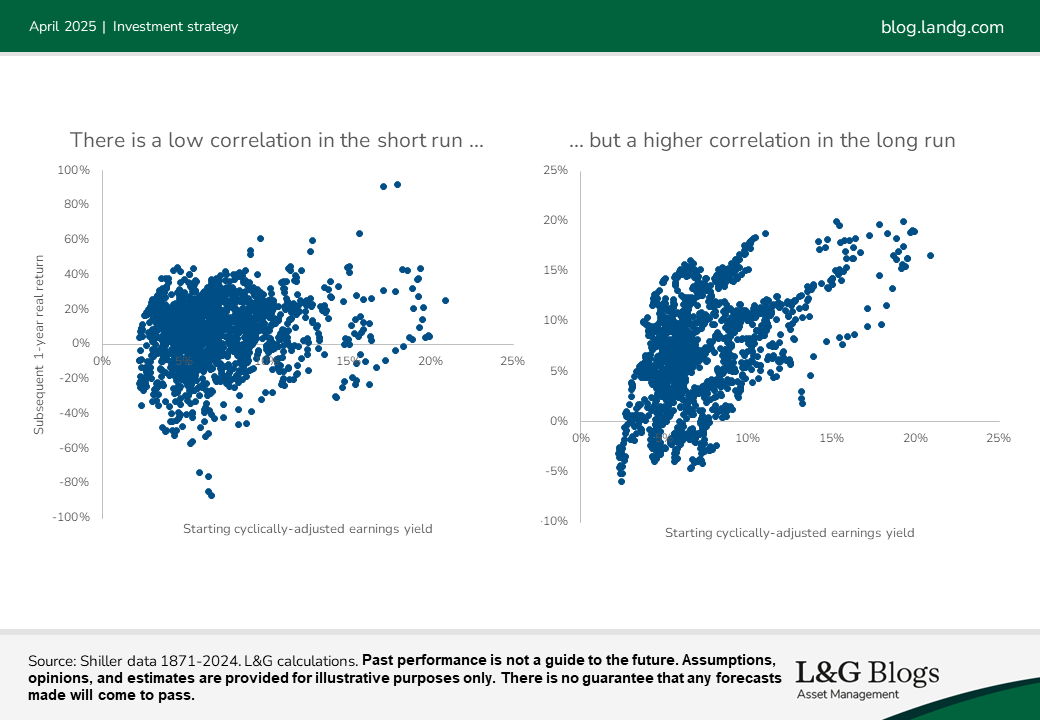

That result might surprise some readers. Scatter plots such as the pair below indicate a low correlation between starting yields and subsequent return in the short run, but a higher correlation in the long run.

What gives?

One issue is that overlapping data leads to overstated correlations. The longer the forecast is relative to the size of the dataset, the more overlapping there is. However, even correcting for that, it’s true that correlations between starting yields and realised returns are much lower over short horizons. So this doesn’t solve the puzzle.

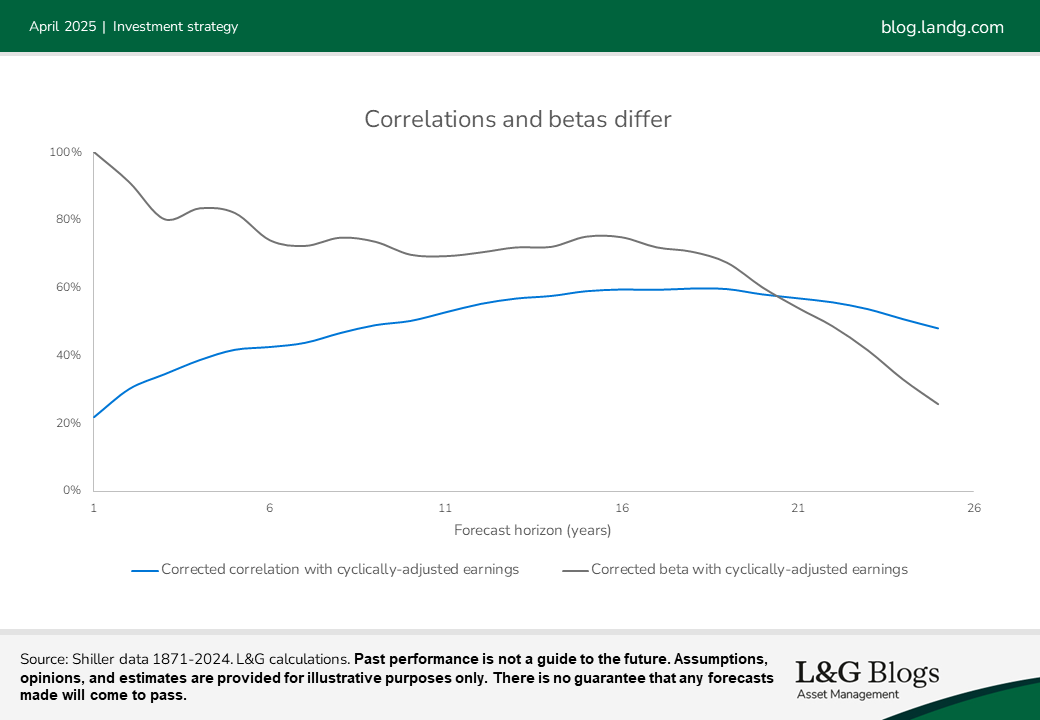

The solution is to appreciate there’s a big difference between beta and correlation, as shown in the chart below:

Beta measures the magnitude of the sensitivity of expected returns to changes in valuations, while correlation only measures the tightness and direction of the relationship (giving a number from -1 to +1).

Betas of expected returns to valuations are highest over short horizons despite low correlations, and the reason for that is noise.

Beta stays cool, correlation gets confused

Adding noise to any dependent variable (such as equity returns), you can reduce the correlation with a predictor (such as valuation yields). But noise does not reduce the beta to the predictor. There are many factors that influence equity returns in the short run including changes in sentiment. These obscure the influence of valuations, but that do not mean valuations aren’t having an impact.

An analogy may help. If, just for the sake of argument, a fund manager changed through time how much they charge investors, the beta of net returns to the level of charges would be -1, regardless of their investment strategy. This is because charges directly reduce net returns. But the correlation of returns to charges may well be close to zero if the gross returns on the strategy are volatile relative to the changes in charges. The noisy gross returns disguise the relationship between net returns and charges, and shrink correlations, but that doesn’t mean the relationship isn’t there.

Step by step, the long run unfolds

As the Chinese philosopher Lao Tzu’s once said, ‘a journey of a thousand miles begins with a single step.’ The long run is merely a collection of short runs glued together. If you are always investing for the short run, and persistently neglecting valuations given low short-term correlations, the danger is that you end up neglecting an important signal of expectations, akin to an investor neglecting costs.

Please stay tuned for the next blog in this series, when we’ll find that this counter-intuitively short-term perspective can be helpful when devising dynamic strategies.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.