Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Solutions chart update: Government bonds in focus

What do rising long-dated bond yields mean for pension schemes?

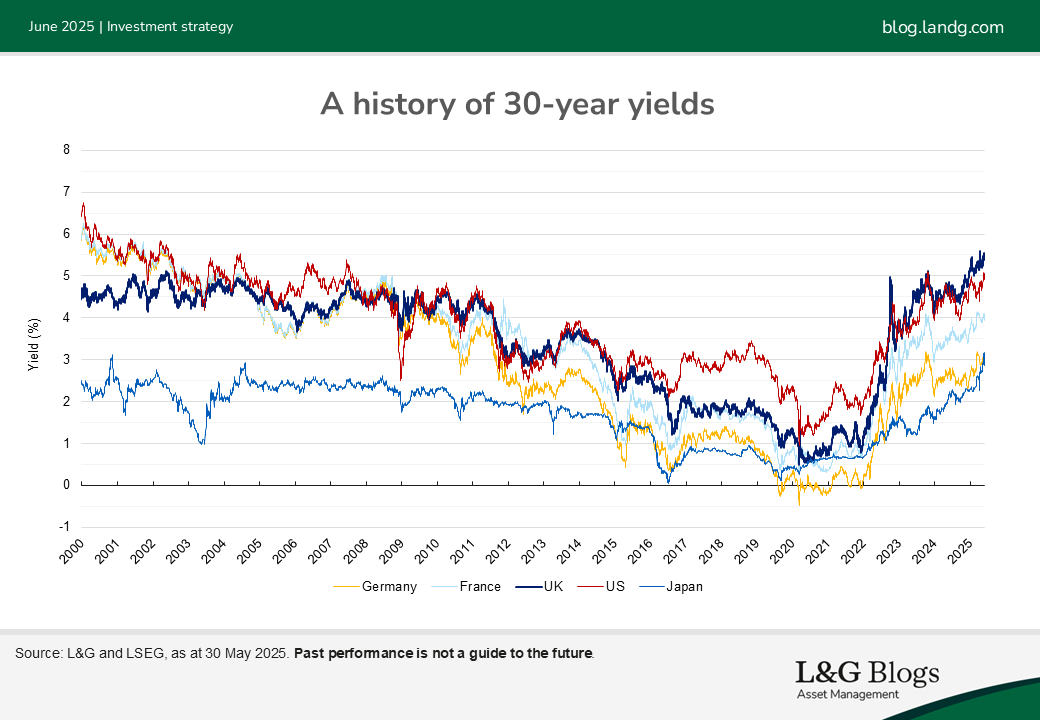

Globally, government bond yields are at elevated levels and are close to or have exceeded the previous peak in Q4 2023. At that time, long-dated yields were typically rising off the back of a steady stream of increases in central bank rates, which in turn came as a result of very high inflation prints and general uncertainty around when inflation might fall.

The current landscape is different, with central banks in the midst of a cutting cycle. The rise in longer-dated yields is therefore in part reflective of greater term premia (i.e. longer-dated yields have risen relative to shorter-dated yields). The chart below provides a snapshot of 30-year yields across five major government bond markets including the UK since 2000:

There are a confluence of factors impacting longer-dated yields but some common themes which many government debt markets are facing are as follows:

- Less structural demand for debt

- High debt supply

- Fiscal concerns

- Political instability

- Inflation persistence

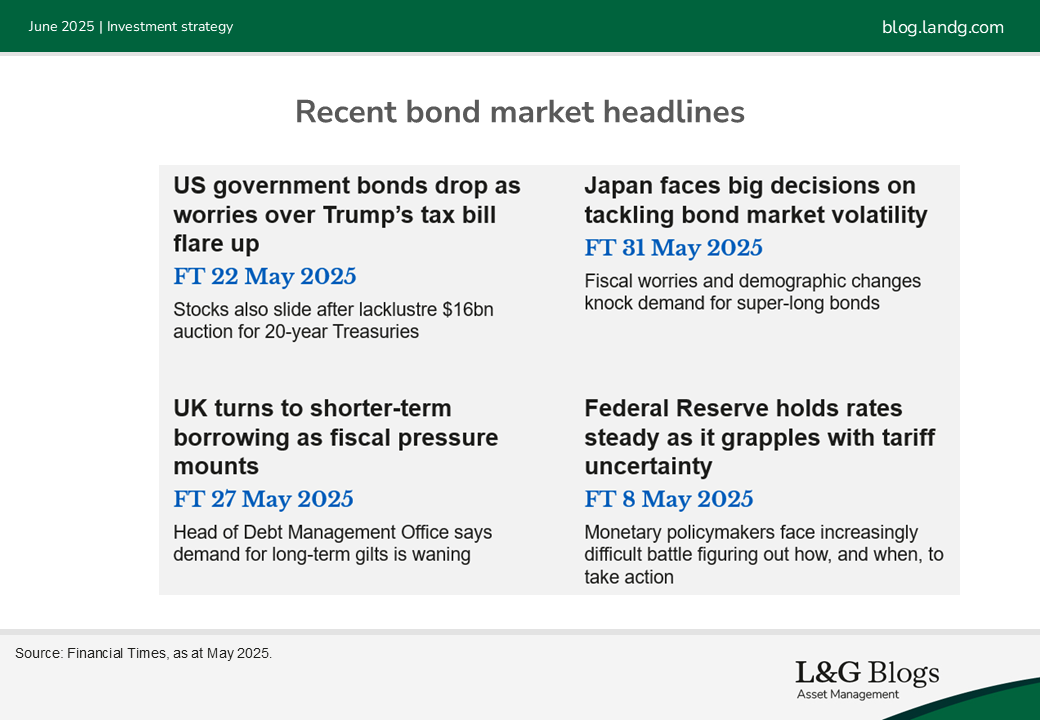

Each market has its own specific challenges, and recent headlines are helpful in providing an idea about sentiment:

To offer some balance, it is worth being aware that China is a notable exception in light of a (relatively) challenging growth environment and very low inflation.

What does this mean for UK DB pension schemes?

“The UK is not an island”

1. Be aware of the potential impact of global yield moves and themes on the UK market

In addition to its own specific factors, we believe the UK is likely to be pulled and pushed by market moves in Europe and the US. This is clear from the earlier chart.

“The journey matters as well as the destination”

2. Be prepared for sharp moves in yields

In 2025 the five-day move higher in US 10-year yields in April 2025 was c.50bps which ranked around the 10th highest going back to 1991. Perhaps more notably these moves came in the face of falling equity markets, thereby posing further questions around whether US treasuries can always be considered a ‘risk-off’ hedge.

Even in Europe – arguably the potential beneficiary of any loss of investor confidence in the US – things have not been straightforward. In Germany, the additional commitment to fiscal spending, while generally received positively, resulted in a 30bps daily move in 10-year yields which is the biggest daily move this century.

In our view there remains potential for sharp moves in the future, given banks’ reduced capability to warehouse risk and central bank quantitative tightening placing more pressure on bank balance sheets (albeit central banks are treading carefully in light of these issues and the potential risks).

“Test and then test again”

3. Ensure collateral headroom levels remain robust

We believe that ensuring that collateral headroom levels remain robust in this environment is key. Pension schemes are generally in strong positions with regards to collateral headroom, however given the potential volatility mentioned above, this can quickly be eroded.

As a very simple practical test, pension funds could consider the implications of a 50bp and 100bp increase in yields. This would be consistent with 30-year gilt yields at around 6% and 6.5% respectively – admittedly very high, but perhaps not unthinkable.

Schemes could approach this from an automated angle, but also via a more qualitative consideration around governance. For example, it may be that a collateral waterfall or existing headroom is easily able to absorb such moves but is there then a plan for topping up the collateral waterfall? If there is no automated collateral waterfall, then would these moves necessitate action or potential future action?

“No bad assets, just bad prices”

4. An opportunity to continue to chip away at long-term hedge ratio targets?

Yields are high and at least partially reflective of the many of the challenges facing bond markets. As long as pension schemes can withstand the mark-to-market volatility, we believe this could potentially provide opportunities to add interest rate hedging.

Past performance is not a guide to the future. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.