Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Could exposure to securitised credit enhance portfolios?

Despite being a huge market, US securitised debt is often overlooked by investors. We ask whether adding exposure to the asset class could help improve a portfolio’s diversification.

US securitised debt is a market worth around $13 trillion. For context, that’s almost half the size of the US treasury market. However, the asset class’s inherent complexity and the role that some parts of the securitised market played in the global financial crisis mean that it can be overlooked by investors.

There are several types of securitised debt. However, they all typically share a common theme; they each take a pool of loans, whether that’s residential or commercial mortgages, consumer loans, or corporate loans, and package them into a securitisation vehicle with principal and interest payments then due to investors.

U.S. agency mortgage-backed securities (MBS) are the largest part of the market and comprise roughly 70% of the space. Agency MBS carry an explicit or implicit U.S. government guarantee on the timely repayment of principal and interest. As such, investors here can seek to avoid credit risk and instead are exposed to the interest-rate cycle through prepayment risk, which is the risk that borrowers will overpay their mortgages faster or slower than expected. This, in turn ,shortens or lengthens the overall duration of the security. That risk helps drive an option-adjusted spread premium – which has recently been around 50 bps for agency MBS over U.S. treasuries.

Securitised credit products comprise the remaining 30% of the market with non-agency mortgage-backed securities, commercial mortgage-backed securities, asset-backed securities and collateralised loan obligations, each representing reasonably sized $500 billion to $1 trillion-plus markets. With each of these asset classes, investors take on the credit risk of the underlying loans to varying degrees, depending on what tranche of the securitisation they invest in. Senior AAA-rated tranches tend to be relatively more insulated from credit events, while below investment-grade subordinated and equity tranches are more exposed to the credit risk of the underlying pool of loans.

While parts of the market, notably U.S. subprime mortgage securitisations, were at the epicentre of the global financial crisis, much has changed in the subsequent 17 years following the crisis. Both regulatory and investor-driven improvements helped to uphold investor rights in the space. Changes include improved underwriting standards, U.S. and E.U. regulations for issuers to retain at least a 5% stake in securitisations, increased regulation of credit rating agencies and greater credit enhancement to provide more insulation from potential losses. These changes have helped the securitised credit markets experience steady growth in issuance and deliver strong risk-adjusted returns over the last decade.

We believe the space is potentially attractive to investors as securitised credit typically carries a shorter interest rate duration along with a notable spread advantage relative to corporate credit. There are a number of sectors, such as collateralised loan obligations (CLOs), that pay a floating rate coupon and as such carry a duration of less than half a year, while those that are fixed rate still often carry lower interest-rate risk.

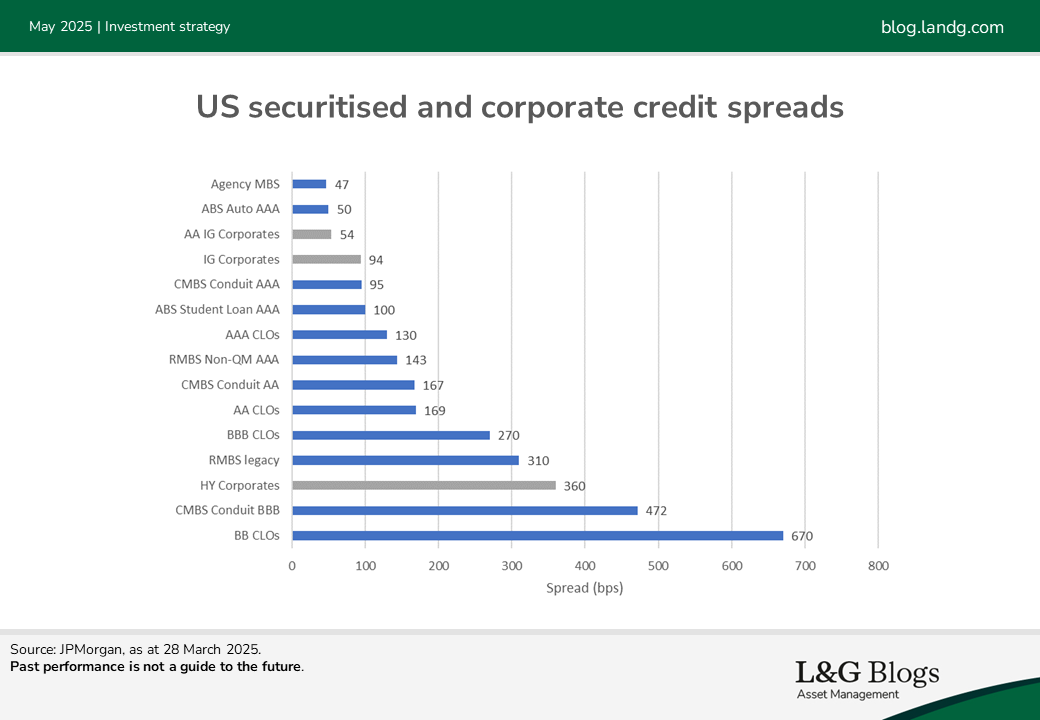

For instance, the Bloomberg U.S. ABS Index carries a duration of 2.6 years as of March 2025, while the Bloomberg U.S. Corporate Bond Index has a duration of 6.9 years. As shown in the chart below, some securitised credit sectors currently carry a roughly 100 bps spread advantage over corporate bonds of an equivalent credit quality.

For instance, AA-rated CLOs had a spread of 169 bps as of March 2025, while AA corporate bonds had a spread of 54 bps. That notable spread advantage has been driven in part by a ‘liquidity premium’ as the securitised markets are smaller than the vast corporate credit market. Still, FINRA data indicates strong trading volumes in investment-grade US securitised credit, with roughly $3 billion traded daily in March 2025. The spread advantage has also been also driven by a complexity premium – securitised credit requires more analytical horsepower to analyse tranches, underlying collateral and loan data.

Thanks to its lower duration and higher spread profile, along with its unique exposure to areas such as the housing and consumer markets, we believe that securitised credit can potentially be an attractive portfolio construction tool.

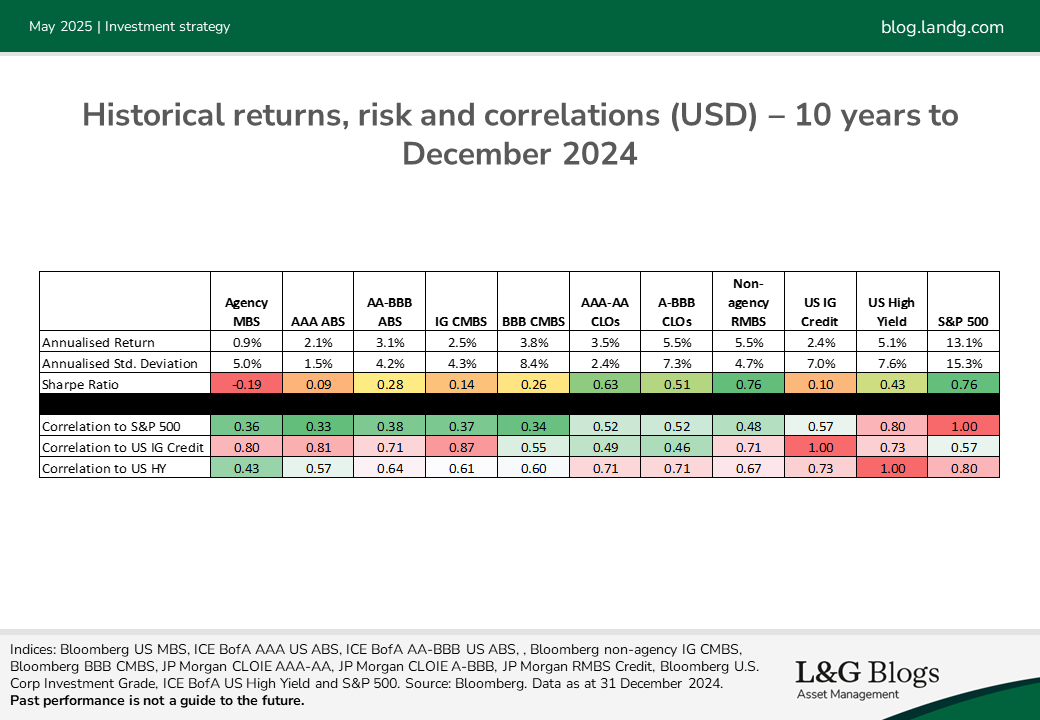

The table below shows the 10-year annualised returns, standard deviations, Sharpe ratios and correlations of US securitised credit indices, US corporate credit indices and the S&P 500. It highlighted that thanks in part to their lower volatility, all securitised credit indices bar the ICE BofA AAA ABS index have historically exhibited a better Sharpe ratio than investment-grade corporates, while AAA-AA CLOs, A-BBB CLOs and non-agency mortgage credit indices have also delivered a higher Sharpe ratio than high yield corporate bonds.

The table below also shows that securitised credit has historically exhibited a lower correlation to equities than traditional corporate credit, while demonstrating lowering correlations to investment-grade and high yield bonds.

As such, we believe that adding securitised credit to a fixed income allocation can potentially help to improve a portfolio’s risk-adjusted return profile and reduce its correlation to equity and bond market movements.

Despite this, the credit side of the securitised market represents less than 1% of the Bloomberg Global Aggregate Index, in part because it is a smaller space than the corporate bond market, and as such, it can be often overlooked in fixed income allocations. While securitised credit has long appealed to pension schemes and insurers as part of a liability-driven investment approach, its potential benefits indicate that it could have a place in portfolios as part of a broader fixed income allocation.

Past performance is not a guide to the future. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.