Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Could a defensive equity strategy defend DC savers?

By providing access to possible equity market upside, with the potential for reduced volatility and drawdowns, we believe defensive equity may be a suitable component of defined contribution (DC) strategies, particularly in the later stages of retirement saving.

Changes in pension provision, particularly in the private sector, have led to approximately 90% of employees now accruing DC pensions, according to the IFoA’s Pension Gap Working Party1. Additionally, the number of DC savers transitioning from the early growth stage of their retirement journey to the mid and later stages is on the rise.

DC savers approaching retirement typically can’t afford the risk of large equity market drawdowns, so traditionally have de-risked from equities into fixed income strategies. However, if portfolios are de-risked too quickly members may miss out on valuable and potentially significant equity market upside. For example, the S&P 500 Index returned more than 20% over both 2023 and 20242.

In today's climate of heightened uncertainty, the pensions industry is increasingly concerned about retirement adequacy and inequalities in retirement savings. Striking the right balance between risk and return is crucial, particularly for those approaching or at retirement.

A place for defensive equity in DC?

Although a relatively new idea for DC savers, option-based strategies have been used by defined benefit (DB) pension schemes to manage equity risk for more than 15 years. While arguably less of a consideration for DC retirement savers in early career stages, a defensive equity strategy could complement traditional diversification to help meet the challenges of the mid-growth/later savings stages, by seeking to provide equity-like returns with reduced volatility and drawdowns.

A defensive equity strategy provides equity market exposure combined with a systematic equity option hedging overlay. This may allow DC savers to retain meaningful participation in equity market upside, while also providing some downside risk management in equity market falls. Such a strategy can be executed via exchange-traded futures and options and be fully rules-based, to ensure transparent and cost-effective implementation.

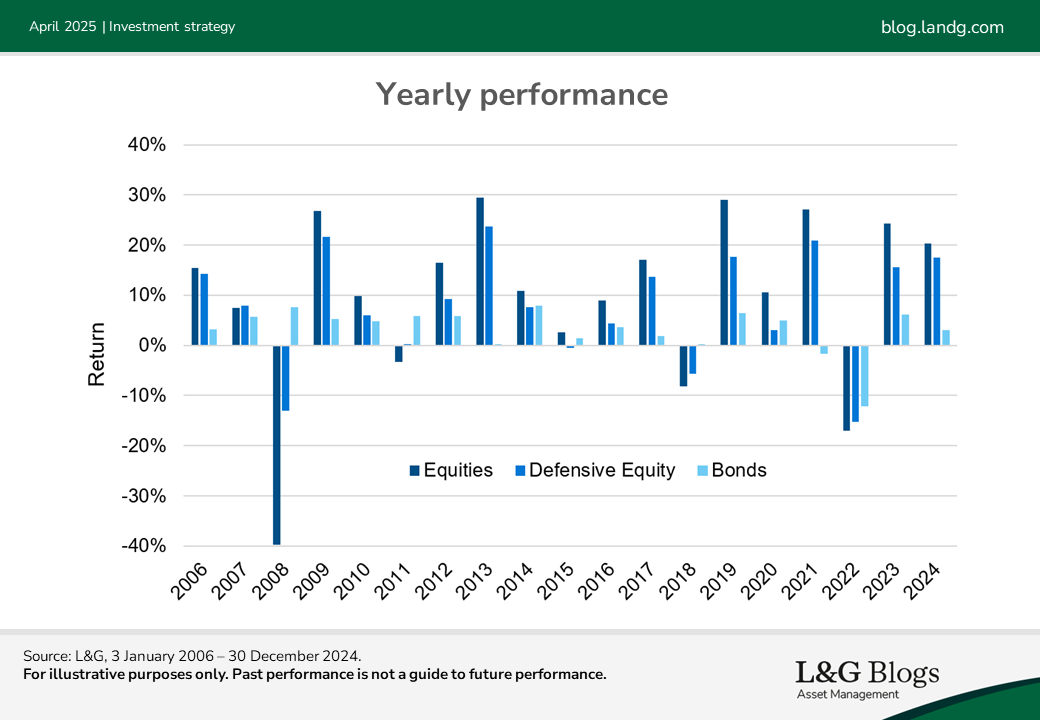

It can be seen from the chart below that historically, a defensive equity strategy has been able to retain a meaningful amount of equity market upside in years when equity market performance is strong (for example 2023 and 2024). But it has also had the potential to reduce drawdowns in downturns, as highlighted in 2008 on the chart. The extent of the reduction, however, will depend on the market scenario, such as timeframe and magnitude of drawdown, and would be expected to be greater in a prolonged period of market stress than in a short-lived downturn or choppy markets (for example 2022).

As highlighted in the chart, when equity markets fell in 2008, bonds provided a positive return, helping to offset losses from equities. However, this may not always be the case. In 2022 equities and bonds fell in tandem, as could be expected in an inflationary environment. Therefore, a defensive equity strategy could complement traditional diversification by incorporating hedging within the equity allocation. Such a strategy may also allow a higher allocation to equities and hence higher growth potential within a diversified portfolio than would otherwise be the case.

Shielding savings inadequacy

DC savers are facing numerous retirement challenges including savings inadequacy, declining homeownership, and longer life expectancy.

Against this backdrop, we need to consider different growth levers, while still striking the right balance between risk and return, particularly important for those approaching retirement.

Therefore, a defensive equity strategy could, in our view, be a valuable tool to complement more traditional DC strategies, allowing for equity market upside, with reduced volatility and drawdowns.

Interested in reading more about DC pensions and investments? You can find our latest content on our designated DC blog page.

1 Levelling up: How to close the pensions gap | The Actuary

2 Bloomberg

Key risks

It should be noted that diversification is no guarantee against a loss in a declining market.

Past performance is not a guide to the future. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Risk management cannot fully eliminate the risk of investment loss.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

The above information does not constitute advice.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.