Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Commercial real estate: the best and the rest

Some sectors in commercial real estate may prove surprisingly resilient.

Along with falls in numerous other asset classes in 2022, UK commercial real estate values fell by a staggering 20% over the second half of 2022;1 the second sharpest six-month correction in history.2

During the first half of last year, in the face of rising inflation and interest rates, real estate looked increasingly expensive relative to other asset classes. While this pattern was true of many global real estate markets, the impact of the UK’s mini-budget turned modest decline into something more extreme.

Market liquidity became challenging; investment volumes dropped 40% below their historic averages3 and low-yielding asset classes (with low cashflow risk or strong growth potential) proved particularly sensitive to rising interest rates. The pace of value reduction started to slow in December 2022 and by March 2023 values increased by a modest 0.2%.

Some market commentary suggests values have bottomed out; we remain cautious for 2023. Our yield models, for instance, suggest market interest rates and penal real-terms rental growth will keep the pressure on real estate’s relative value. We expect more asset disposals from maturing DB funds, with pressure on some investors looking to re-finance properties bought, or financed, in 2018 or 2019.

Many of these investors face the biggest swing in finance costs recorded, necessitating injections of equity to reduce leverage. Where the building or income quality is lower, or that equity is unavailable, we believe there will be pressure to sell quickly.

Office costs

There are specific sector risks too, in our view. Offices remain exposed, not only to new ways of working, but also to rising management and refurbishment costs in order to attract occupiers. But the sector ‘only’ corrected by 15% in the second half of 2022. We expect recessionary conditions to accelerate occupier decision-making. And, as deadlines to meet sustainability legislation near, additional capital expenditure requirements will create a toxic combination for certain assets, in our view.

By contrast, the pricing correction in certain sectors has moved expected returns more in line with investors’ target rates. Real estate debt returns have been boosted by high interest rates, while reticent traditional lenders have left a market gap for others to exploit, subject to underwriting.

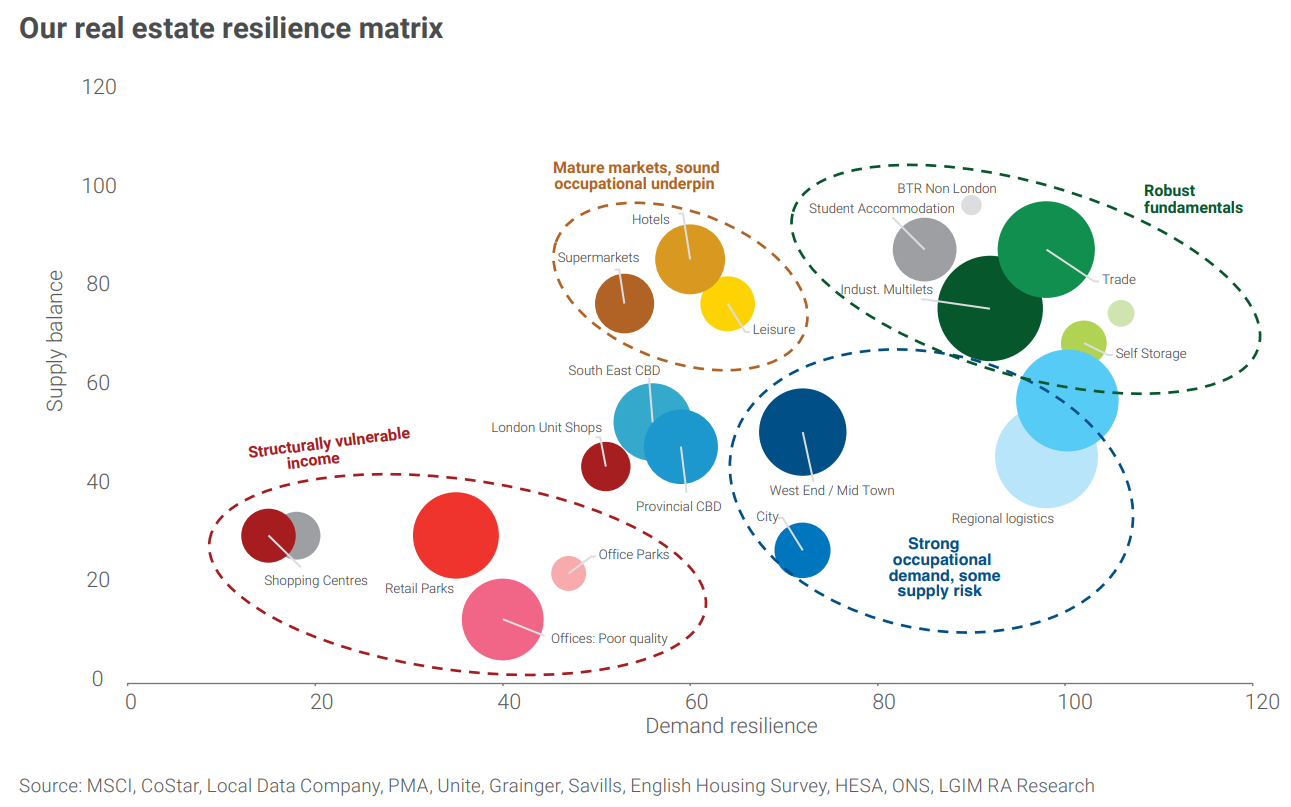

More specifically, the residential segments of build-to-rent residential and purpose-built student accommodation have proved resilient over the last 12 months and, we believe, offer good rental growth prospects for well managed and located assets. Secondly, parts of the industrial market, in particular self-storage and multi-let industrial, look good value, in our view, based on higher yields and consistent expectations for long-term income growth. Thirdly, we believe there is value in good quality well-let assets with income protection: prices of long-income real estate with indexation which were hit hard in the second half of 2022 due to interest rate sensitivity.

To some extent, the pricing correction seen in the second half of 2022 punished ‘the best’. 2023, in our view, is set to be much more challenging for ‘the rest’.

This blog is an extract from our CIO Outlook. Read our full CIO Outlook.

1. MSCI Monthly Digest, June to December 2022.

2. Since 1986 on the MSCI Monthly Digest. The largest was -23% during the GFC (six months to March 2009).

3. PropertyData.com as at April 2023.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.