Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

CDS: A credit-sensitive subject

What are the considerations when sizing credit default swaps (CDS) in your credit hedging portfolio? While lower volatility (versus physical credit spreads) may imply a higher exposure is warranted, this factor is likely offset by its lower correlation.

The substantial improvement in scheme funding levels has led to potentially two thirds of schemes being able to afford a buyout (based on data from the PPF). For those targeting buyout as their preferred endgame, there is a focus on best matching buyout pricing while preparing for a transaction. This has led to a substantial uptick in schemes looking to hedge credit spreads (as well as interest rates and inflation); reflecting this is the third key economic driver of buyout pricing.

What role might CDS have?

We believe buyout liabilities have credit sensitivity of around 40-60% of total PV01.

The cornerstone strategy to match this level of credit sensitivity is typically a buy and maintain credit approach. This is broadly aligned with how insurers invest, as it is a potential means of replicating the credit sensitivity inherent within insurer pricing.

As well as allocating more to physical credit, schemes are increasingly using CDS as part of their credit sensitivity hedge (usually to complement a physical credit allocation). There are several attractive features of CDS in our view.

|

Capital efficiency |

CDS derivatives are a capital-efficient way to increase credit exposure and can be supported from the same collateral pool as a scheme’s rates/inflation hedge. |

|

Low transaction costs |

Transaction costs are much lower than physical credit. We believe this is particularly attractive for schemes who are concerned around the ability to transfer all physical credit to an insurer. |

|

Dynamism |

The CDS market has greater liquidity versus physical credit, so can typically be used quickly to seek to access more attractive credit spreads if a potential opportunity presents itself. |

However, CDS is less sensitive to buyout spreads than physical credit, which isn’t ideal given that schemes typically want that sensitivity! There are two reasons for the lower sensitivity. First, it is less volatile. Second, it is less correlated to buyout spreads. As we shall see, these drivers need to be dealt with differently.

Dealing with lower volatility

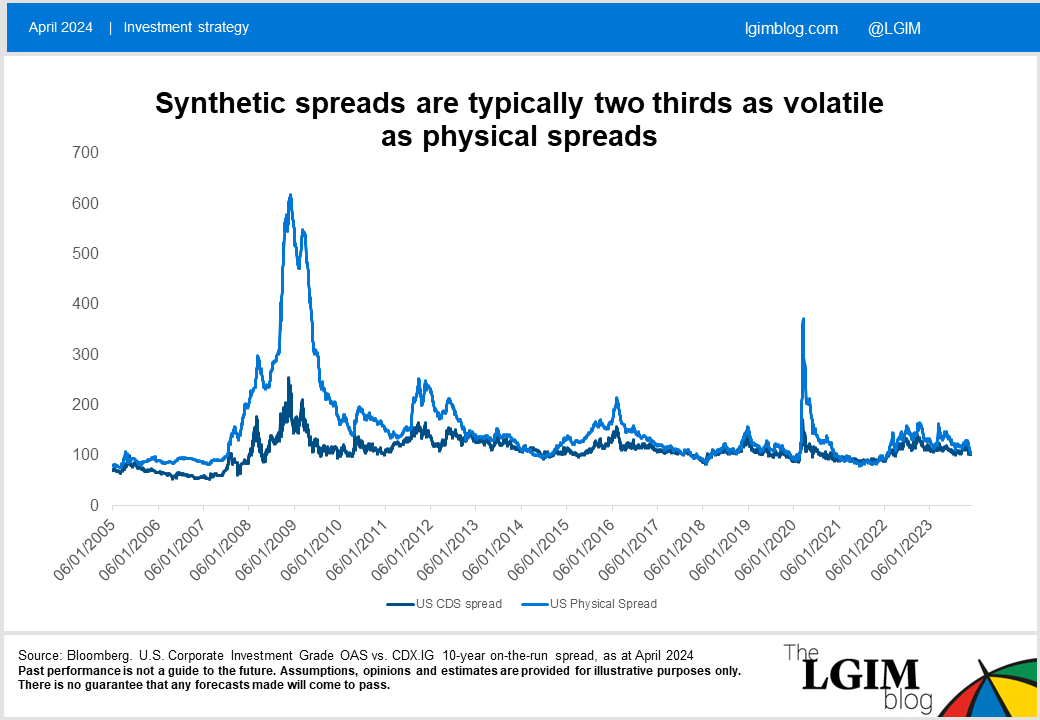

Tackling the lower volatility aspect first, CDS spreads typically are around two thirds as volatile as physical credit spreads, as can be seen below:

This means that if CDS and physical spreads were perfectly correlated and physical credit spreads fell by 30bps, for example, then we’d expect CDS spreads to fall by only 20bps. This can be compensated for simply by holding more CDS. Assuming the same duration of physical credit and CDS, you could replace £100m of physical credit with £150m of CDS and achieve the same effective exposure.

Dealing with a lower correlation

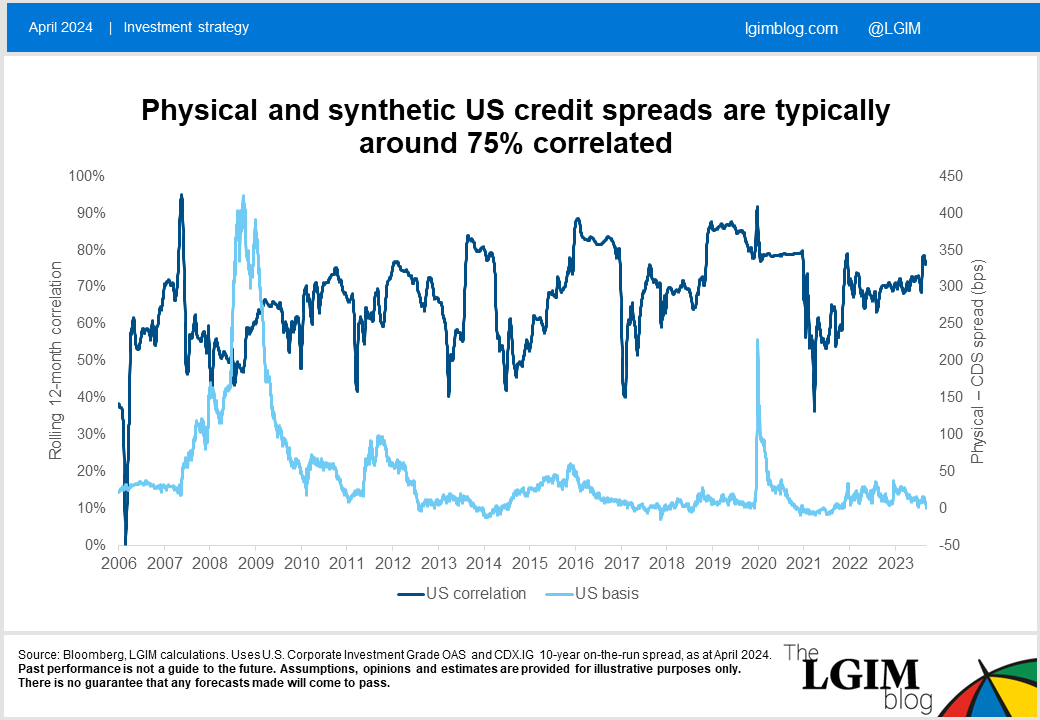

Physical US spreads and CDS spreads are around 75% correlated, as can be seen below. The US basis here refers to the difference between the physical spread and the CDS spread:

This lower correlation also means you get less ‘bang for your buck’ from CDS[1]. Continuing the example above, a correlation of 75% implies that CDS has a beta of only 0.5 to physical credit (2/3 x 0.75).

However, we believe the right response, from a risk management angle, is not to compensate by increasing your CDS exposure. To take an extreme, if the correlation were 1% the right answer is not to increase exposure 100-fold!

To minimise overall risk, that includes basis risk of CDS being an imperfect match, it turns out the right answer could be to hold less in CDS, in line with the correlation. Although ramping up the CDS allocation improves the credit hedge ratio, it introduces basis risk which offsets this benefit.

Putting this together: What does this mean for a target CDS allocation?

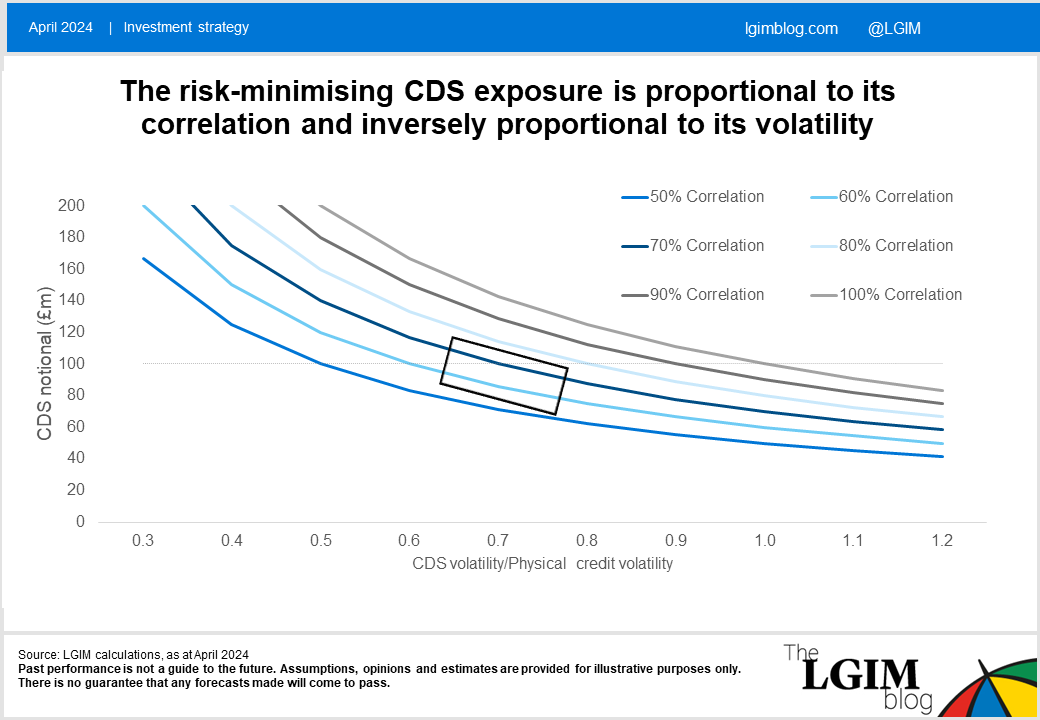

Historical analysis points to a similar figure for both the volatility ratio and the correlation i.e. in the range of 60%-80%. These roughly offset each other so the right answer may be to target a similar notional allocation, even though it only gives you about half the credit beta. The chart below illustrates this idea in general:

In practice, the relative volatilities and correlations vary with market conditions. This makes for a complicated story but on average we expect to be near the black box highlighted.

When are credit hedge ratios useful?

The above analysis illustrates the CS01 hedge ratio isn’t the whole story in terms of credit risk management – targeting a 100% hedge of the credit beta in buyout liabilities isn’t necessarily the best thing to do. But when is and isn’t it the right answer?

The key is whether the uncorrelated basis risk varies with what you are optimising for. For example, suppose you have a fixed CDS allocation, and are deciding how much physical credit to hold. We believe the ideal thing to do is to acknowledge CDS only gives you half as much sensitivity as physical and top the hedge up to 100% using a physical allocation (if you can).

A similar thing could happen if you hold some equity – you might allow for its implicit CS01 when deciding how much more you need and top it up with explicit CS01 from physical credit. You are likely holding the equity for growth purposes and its credit sensitivity is just a nice side effect.

But if the physical allocation is fixed and you are varying your CDS allocation, in our view you should acknowledge that upping the hedge ratio also incurs basis risk so needs to be moderated. That may seem paradoxical but isn’t once you remember CDS isn’t being held because it is the best hedge of buyout credit sensitivity (it isn’t) but because of its other potentially attractive qualities.

If you’ve enjoyed this blog post, please click here to discover more of our content that’s specifically tailored for DB schemes.

You can also sign up here to receive the latest content most relevant for you via email.

[1] assuming it is physical spreads that drive buyout prices, which is not unreasonable in our view given this is what insurers hold

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.