Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Catastrophe bonds: Is the party over?

Insurance-linked bonds, also known as cat bonds, have had three exceptionally good years. But spreads are now tightening fast. We explore what’s driving the shift and how multi-asset investors could position from here.

Key takeaways

|

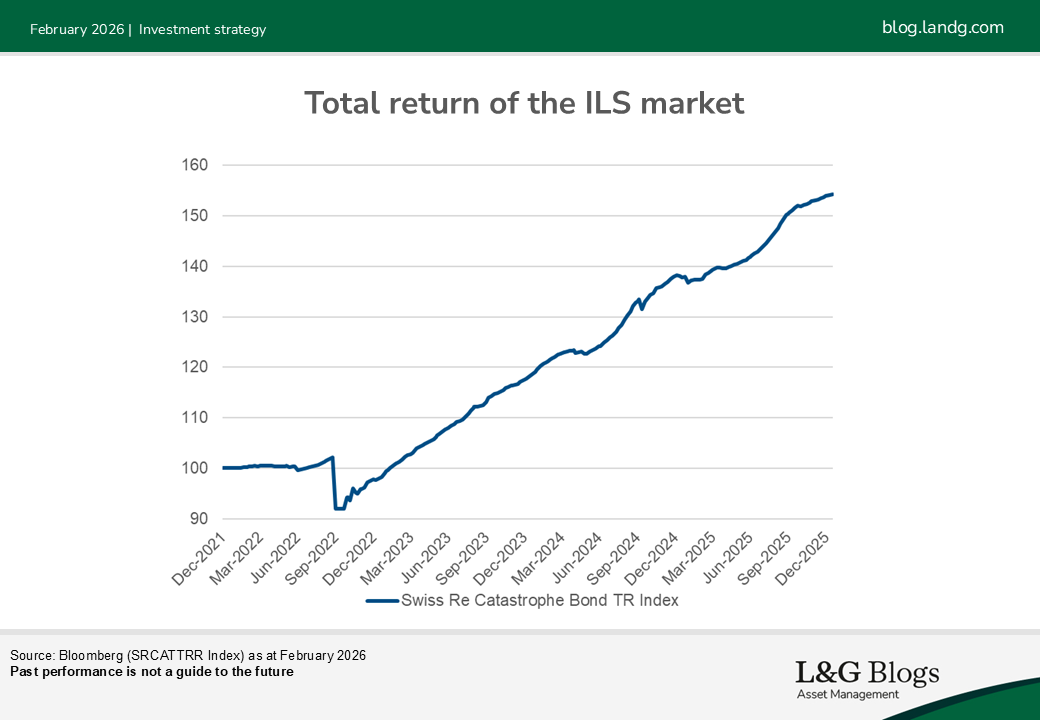

Since our first blog, catastrophe bonds have delivered their best three-year performance on record, with a total return of nearly 50%. This remarkable run followed an unusually benign period for insured losses and the generous spreads available at the end of 2022 after Hurricane Ian. Cat bonds subsequently made headlines and attracted both investor and public interest when Fortune magazine identified them as the top-performing investment strategy in 2023.

However, success has a habit of eroding future return potential. Since then, increasing capital flows and a string of quieter years for major natural catastrophes have steadily eroded the excess premia that once characterised the asset class. Now, with spreads tightening and record issuance meeting surging investor demand, the question arises: is the most attractive part of the cycle behind us?

Resilient performance amid recent hurricane activity

Despite the hurricane activity over the past three years, the cat bond market has benefited from limited insured losses. For example, Hurricane Helene in 2024 was ranked among the 15 most costly natural disasters globally since 1900, and Hurricane Milton (also in 2024) was one of the strongest Atlantic hurricanes on record. Yet, neither had any meaningful impact on cat bonds due to the high levels of market reinsurance and fortunate locations of landfall, avoiding the largest urban centres.

In 2025, we saw five hurricanes develop in the Atlantic Basin, but for the first time in a decade none made landfall in the US. In effect, there have been a series of notable catastrophe events, yet none has been material to the cat bond market.

Market dynamics: Spreads and capital flows

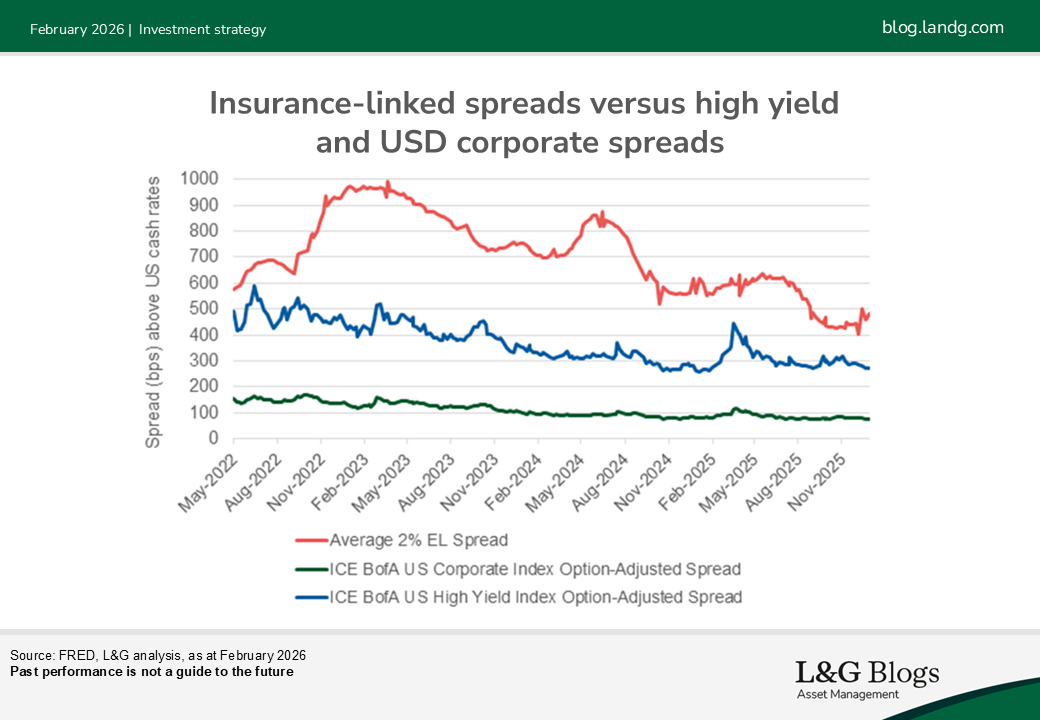

Strong realised returns, combined with growing maturity in the insurance-linked security (ILS) ecosystem, have encouraged meaningful inflows of new capital. As supply has struggled to keep pace with this influx, spreads have compressed. This comes despite record issuance of new bonds with 2023, 2024 and 2025 each breaking records in turn for most risk capital issued during the year.[1] The market’s partial insulation from traditional capital and insurance markets can produce a boom-bust cycle driven more by issuance patterns and recent loss activity than by fundamentals alone.

We also observed the cat bond market expanding into new geographies and peril types, some of which are less rewarded than the traditional US storm and earthquake risks due to the added intra-asset class diversification[2] benefits offered.

Although these lower spreads may challenge net returns, cat bonds still deliver a notable premium over investment grade and high yield corporate bonds. While, in our view, this provides an opportunity for investors to selectively invest in well-rewarded risks to maintain performance in a declining spread environment, institutional investors face governance considerations when taking concentrated exposure. Large, event-driven drawdowns can attract heightened scrutiny, even when they reflect the nature of the asset class rather than deficiencies in process.

Despite these headwinds, catastrophe bonds have retained their defining strength of low correlation with mainstream asset classes. In our view, for investors adopting a total-portfolio perspective, selective exposure to the most attractively priced insurance risks can still play a potentially valuable strategic and dynamic role. As multi-asset investors we aim to maintain exposure to the asset class whilst awaiting more favourable entry points without sacrificing broader portfolio integrity.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. Past performance is not a guide to the future.

[1] Catastrophe bonds & ILS issued and outstanding by year - Artemis.bm

[2] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.