Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Capital market assumptions: estimating long-term returns

How should investors go about setting long-term return estimates across different asset classes?

Our CAMERA (Capital Market Expected Return Assumptions), which we introduced previously and updated recently, brings together our valuations-based medium-term asset-class return expectations and our long-term risk-based equilibrium model. In this blog we reach for the binoculars and focus on our long-term model. We outline different potential ways to go about setting long-term returns and explain the approach we settled on.

Different possible methods

There are three main approaches used to set long-term returns:

(1) Starting valuations

These are measures of how expensive an asset class is, with cheaper valuations corresponding to higher assumed future returns. The yield on gilts is a good starting point to estimate the future return on gilts even for long horizons (and is their return for buy-and-hold investors of long-dated gilts), provided the yield is pulled from the right part of the curve. However, for risky assets the impact of valuations over multi-decade forecast horizons is likely to be diluted, so other approaches can make more sense in judging expected returns.

(2) Historical average returns

This method uses the average annual return of an asset class over a long period to estimate its future return. This method is simple and intuitive. However, you need surprisingly large amounts of data to get anything remotely statistically reliable, and by the time you’ve obtained such a large volume the data is likely to have lost much of its relevance to today’s markets. Another issue is that the historical record may contain one-off headwinds or tailwinds that are unlikely to repeat. As the standard disclaimer rightly states, ‘past performance is no guarantee of future results’.

(3) Risk-based models

Markets are best assumed efficient until proved otherwise. In efficient markets, excess returns should be compensation for bearing systematic risk[1]. As such, understanding the risk of an asset class is important to understanding its long-run expected return.

Our approach

Our long-term returns assumptions draw on a combination of these three methods. For a given horizon, we use the spot government bond yield over that horizon as the risk-free rate i.e. a valuation-estimate as per (1)[2].

Our starting point for return in excess of that rate uses a risk-based approach i.e. (3). This tells us the relative risk of different asset classes and helps us rank asset classes. But we still need a reference point to calculate the excess return numbers. To calibrate on this front, we use various estimates from academia of the developed market equity risk premium. The literature includes studying long-term historical performance (100+ years), so effectively uses (2).

Finally, some important overrides are used, informed by quantitative and qualitive analysis. This also involves a combination of approaches (2) and (3), as we shall see.

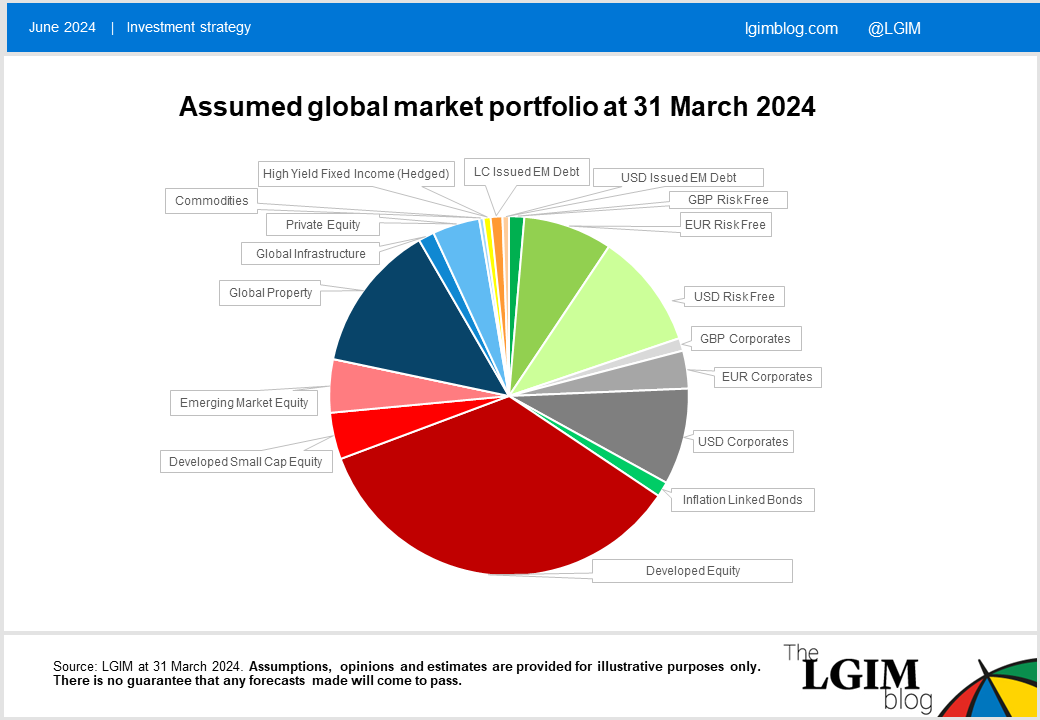

Equilibrium returns and the market portfolio

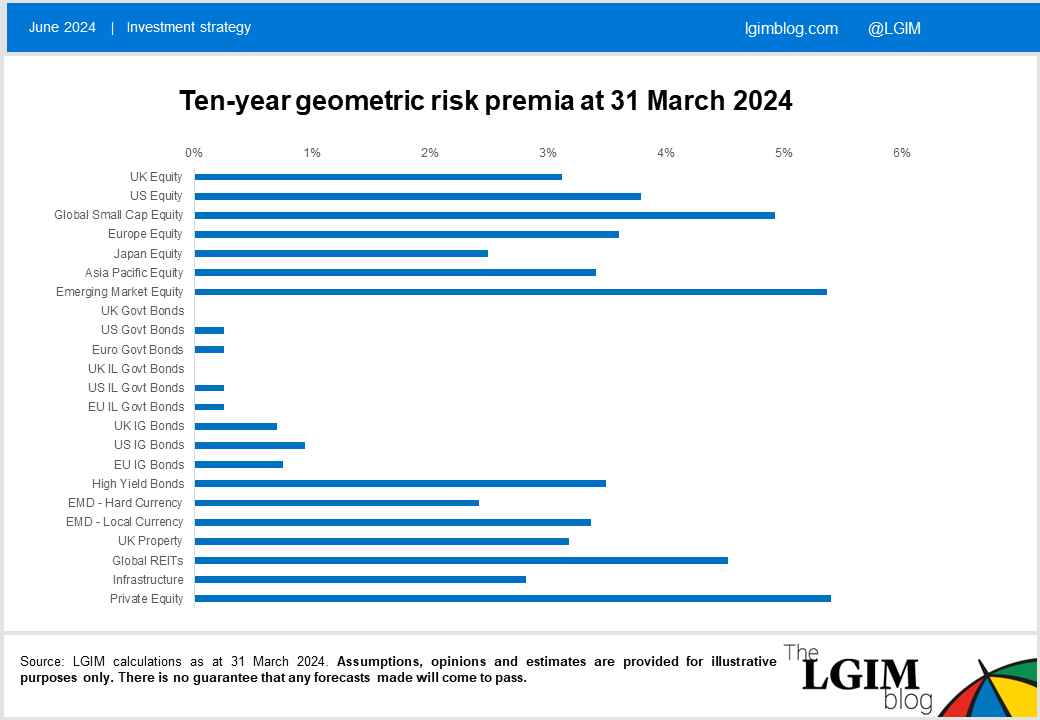

The risk-based model we use as a starting point is based on a version of the Capital Asset Pricing Model (CAPM), an equilibrium model. We derive initial return estimates for different asset classes by estimating the marginal contribution of each asset class to the risk of the market portfolio. By ‘market portfolio’ we mean the global investible universe, including equities, fixed income and alternatives. This can be surprisingly hard to pin down exactly, but our assumption as at 31 March 2024 is shown below:

The marginal contributions to risk are computed using beta – a combination of the volatility of the asset and its correlation to the market. The betas are scaled so we get an answer for developed market equity that is consistent with our estimate based on academic studies[3].

The American economist John Cochrane, among others, pointed out an important theorem: the average investor must hold the market portfolio. This can be useful in formulating a strategic asset allocation, given portfolio theory is difficult. Unless you have good reasons to believe that your portfolio problem is different from the average investor you’re done – “off to the total market portfolio with you,” as John puts it.

Why is this relevant for return assumptions? Well, if we set excess returns in line with their beta to the market portfolio a nice feature emerges. Seeking to maximise the Sharpe ratio from a model that uses the same risk assumptions neatly recovers the market portfolio. This matters because ideally you only want your optimised portfolios to differ from the market portfolio for genuine and identifiable reasons, as opposed to inconsistencies in the treatment of risk and return estimates[4].

Deviating from CAPM

While we believe multi-asset CAPM is a great starting point, there are some good reasons to deviate from it. For example:

- Few investors are average. Some like central banks are not mainly focused on return generation. Others might be restricted in which assets they can invest. This heterogeneity can lead to uncertainty around the most appropriate market portfolio weights to use

- Investors might request a reward for risk factors other than just market exposure. For example, some assets are illiquid, and investors with longer horizons can tolerate this better than short-term investors. As another example, a term premium on bonds can arise reflecting preferences to invest/lend at different maturities

- Leverage constraints can mean stocks are bid up by investors seeking a higher expected return (which in turn can lower future expected returns for stocks). This phenomenon can result in lower-beta asset classes earning more than they ‘should’ according to CAPM

- CAPM can be difficult to apply and/or a poor guide to the return on credits such as corporate bonds and emerging market debt. Higher credit spread duration leads to higher short-term volatility but doesn’t necessarily lead to a higher expected return. It may make more sense to base long-term excess returns on long-term average spread levels less an allowance for losses from downgrades and defaults

- There’s evidence investors place additional weight on downside tail scenarios - asset classes with negatively skewed returns may require higher risk premia[5]

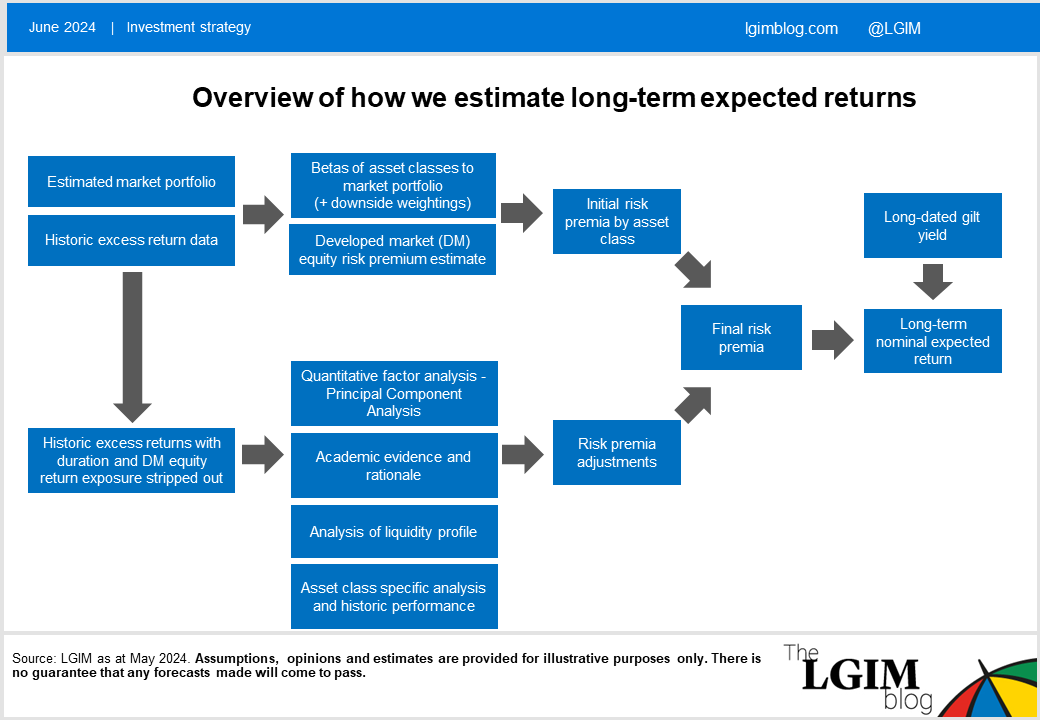

There is no single ‘right’ way to set long-term returns but the steps we take to formulate adjustments to the CAPM estimates are outlined at a high level in the flow chart below. This is followed by our estimates as at 31 March 2024.

For more detail on the overall framework, please speak to your LGIM representative.

Past performance is not a guide to the future. Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1] Or market risk. It should be noted that diversification is no guarantee against a loss in a declining market.

[2] We assume no long-run term premium for UK bonds, so this is the same as our long-term assumption for cash returns.

[3] We use studies such as ‘The Triumph of the Optimists: 101 Years of Global Investments Returns’ (Dimson, Marsh and Staunton, London Business School) and the Barclays Equity Gilt Study to derive our geometric risk premium estimate of 3.5%-4.0% pa.

[4] We take care to ensure that our models are not driven by arbitrary inconsistencies between models for return and models for risk. For example, we use the same return history and exponential weighting.

[5] A current area of research we are working on involves replacing the quadratic utility function underpinning CAPM that ignores skew, kurtosis and higher moments with power utility that allows for them.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.