Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Can UK housing association bonds help to drive social impact?

We assess the opportunities for local government pensions schemes (LGPS) to invest in UK productive finance via the physical infrastructure exposure inherent in housing associations.

As LGPS funds find themselves better funded than ever[1], schemes are looking for ways to de-risk and simultaneously target returns, generate cashflows and deliver in terms of social purpose. In this vein, we believe that de-risking via a buy and maintain credit approach could offer potential opportunities.

This approach tends to be characterised by low turnover, which seeks to mitigate drawdown risk while also targeting long-term returns. As such we believe there is potentially a close match with the qualities of the housing associations (HA) sector.

Social purpose?

All housing associations in the UK are mandated by The Regulator of Social Housing and the UK government to perform the same task, namely, to maintain and/or increase the UK social housing stock. The sector therefore provides exposure to long-term physical asset-backed infrastructure projects.

UK housing associations tend to have a strong social purpose. They are not-for-profit and the majority of their surplus capital is reinvested into both existing housing stock and building new homes in the affordable and social housing market. These sectors form a crucial part of the UK housing industry by providing homes for low-income tenants on a regulated rental formula.

Avoiding a one-size-fits-all approach

Within UK housing associations, we believe intensive fundamental research is key to potential success, as is avoiding a one-size-fits-all approach. Recently, following several high-profile incidents, there has been increased scrutiny on the sector and its social performance.

Standards vary substantially between HAs. As such, reviewing management actions and responses is crucial when analysing the sector. Deep sector experience and in-depth knowledge and understanding of disclosure is also key when seeking to distinguish between the top and bottom performers in the sector.

Intensive fundamental research includes substantial due diligence before investing in a HA as well as continued engagement once an investment has been made e.g. meeting senior management at least once a year.

Screening for impact

At L&G, our coverage spans the sector and includes HAs we do not currently invest in, though may consider for investment in the future. Furthermore, the level of positive social impact achieved is feature of our creditworthiness assessment.

We welcomed the regulator’s introduction of a ‘Customer’ grading as part of its oversight process in July 2024. This grading focusses on whether housing associations are delivering on the consumer standards they have set out.

There are four gradings from ‘fully delivering’ to ‘serious failings’. We have already seen this new ranking system have an impact. Individual HAs have the ability to self-refer to the regulator for inspection, when they fear non-compliance. Several HAs have already done so.

We see the role of investment in housing associations, potentially via a low-turnover, buy and maintain approach, as being key in the ongoing social improvements being made within the sector.

We focus our investment on HAs who carry out their business according to an acceptable positive social footprint. We have a proprietary independent assessment and rating approach which we apply to calculate a score for each HA. For example, customer management processes and disclosure are graded as part of our assessment framework.

Should the score fall below our minimum threshold we reengage with the HA specifically on our concerns. In the past, based on how issues have been addressed, we have taken the decision to purchase or dispose of the bonds of low-scoring HAs.

As such, through engagement with sector laggards and the threat of our divestment, we have been able to drive change in the HA sector – a sector that we believe is potentially well-suited to the objectives of LGPS funds.

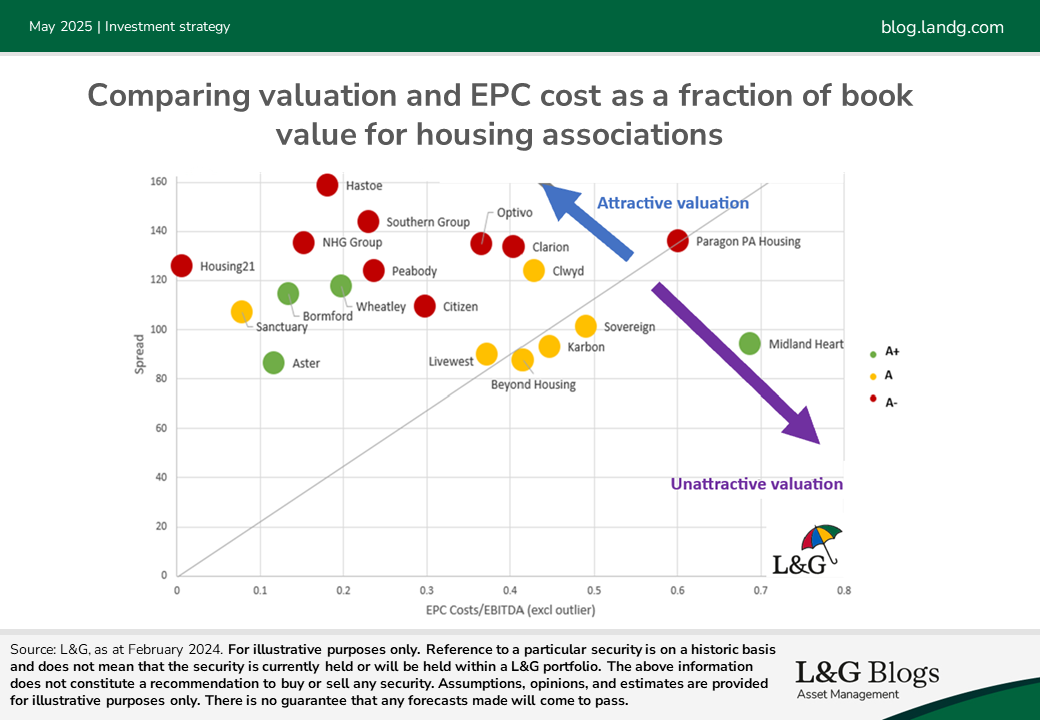

Case study: Our energy performance contract (EPC) engagement in 2024

Background

- Current EPC requirements are set out in the Energy Performance of Buildings (England and Wales) Regulations 2012

- Designed to provide information on the energy performance of houses for comparison and improvement recommendation

- Compliance and positive performance is imperative for housing associations as failure to meet minimum standards could present significant future expenditure

Our engagement

- Our goal was to identify potential threats to balance sheet and cashflow quality

- We wrote to every Housing Association under our coverage, this includes almost all HAs which issues bonds

Results

- Our analysis suggested strong correlation between EPC spending and stock age

- We assessed the attitude of individual management teams based on their quality of response and willingness to engage

- We have uncovered that some of the risk is not being priced in by the market

- We found that not all risk is being accounted for appropriately by rating agencies

Case study shown for illustrative purposes only. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.