Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Are growth strategies anti-value?

The answer is nuanced – but designing growth strategies in a way that is agnostic to value could allow investors to capture the market returns unique to each factor.

Growth stocks tend to be characterised by high price multiples. In the academic literature, the terms ‘expensive’ or ‘glamour’ have been used interchangeably to describe such stocks.[1] By contrast, value stocks are defined as undervalued stocks relative to their intrinsic measures of worth.

In today’s growth market landscape, we observe index providers placing growth and value stocks at opposite ends of the investment spectrum. Arguably, this may lead to growth strategies featuring only expensive, growing companies and value strategies featuring only undervalued, shrinking companies.

This leads to a well-worn question: ‘is growth anti-value?’

The definition matters

The definition of growth matters when designing the investment style. We define growth investing as a focus on companies with high realised growth in fundamentals for future capital appreciation.

Independent of valuations, the objective is to select companies that are expected to have consistent long-term growth in the future.

Our definitions of growth and value aim to enhance potential for investors to capture market returns unique to each investment strategy.

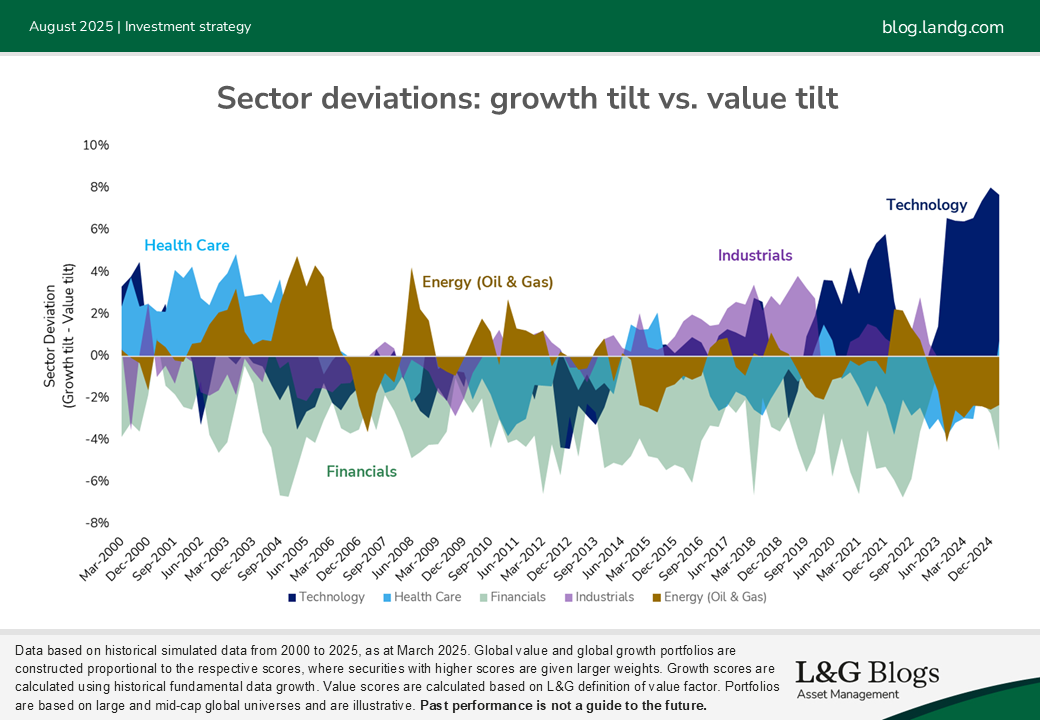

Historical sector allocations

Sector allocations differ between growth and value strategies, based on how we’ve defined growth. Below we observe that technology is frequently overweighted and financials often underweighted when comparing growth to value tilt portfolios. For cyclical sectors, energy (oil and gas) allocations appear dynamic, while industrials exhibit more frequent overweights in growth portfolios.

It follows the evolution of sector allocations within growth and value strategies is likely influenced by market cycles and long-term structural trends within industries.

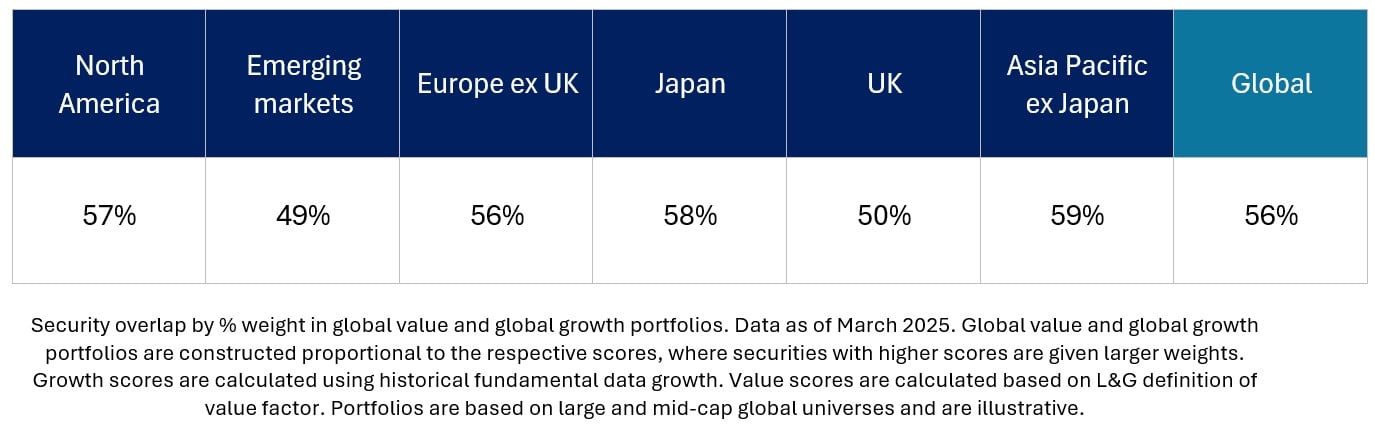

Point-in-time security overlaps

A snapshot of the percentage of security weight overlaps between the two strategies on a regional and global basis indicates the presence of undervalued stocks in the growth portfolio and high-growth stocks in the value portfolio. The weight of the overlaps suggests that growth and value are not mutually exclusive.

Why would growth not look anti-value?

1. The valuations argument

Growth stocks don’t always appear expensive. There is evidence that investors may be slow to price in company fundamentals.[2] Growth stocks may be more expensive than value stocks due to the market pricing in future fundamentals growth, as we see with US tech stocks. However, we find examples of undervalued stocks within the US tech sector as of December 2024, with both value and growth scores greater than 50.[3]

Equally, expensive stocks are not necessarily growth stocks. Investor behaviors such as over-confidence, anchoring and confirmation bias may lead to the overvaluation of stocks, irrespective of the firm’s fundamental qualities.

Overvaluation may also be due to the overextrapolation of growth too far into the future. For example, some stocks that soared during the COVID-19 pandemic experienced slower growth in the years that followed.

2. The fundamentals argument

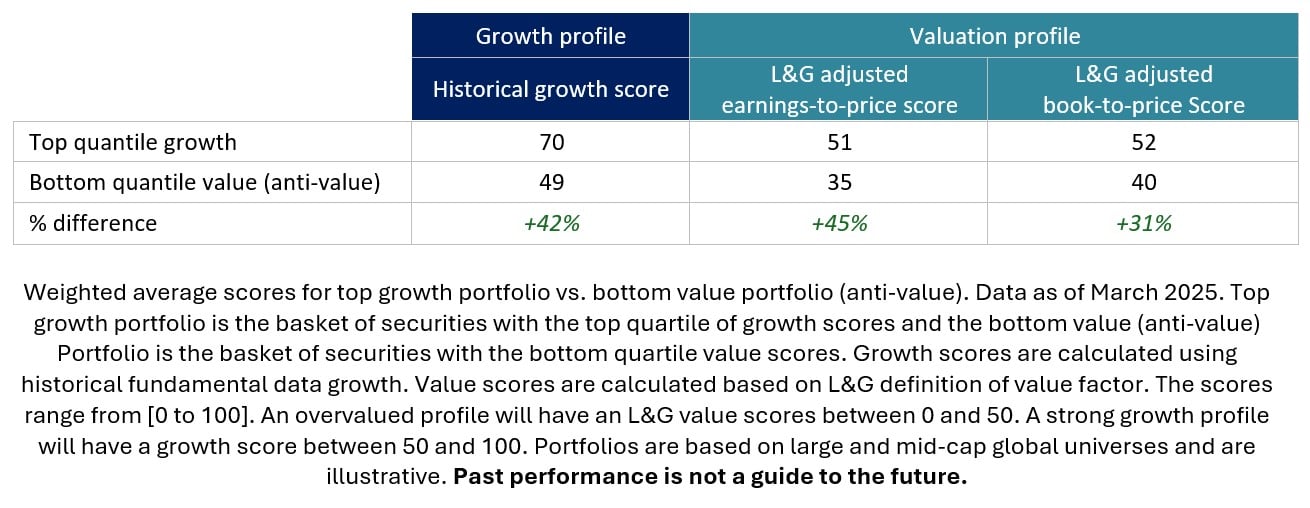

In addition to valuation metrics, company fundamentals also support a distinction between growth and anti-value.

The top growth portfolio, which represents the set of securities with the strongest growth characteristics, exhibits a different fundamental profile to the bottom value portfolio, or the overvalued (anti-value) stocks.

The table below shows stronger fundamentals growth and attractive valuations for the top growth portfolio vs. the anti-value portfolio. It follows that anti-value stocks do not always reflect growth in company fundamentals, using our definitions.

When does growth look anti-value?

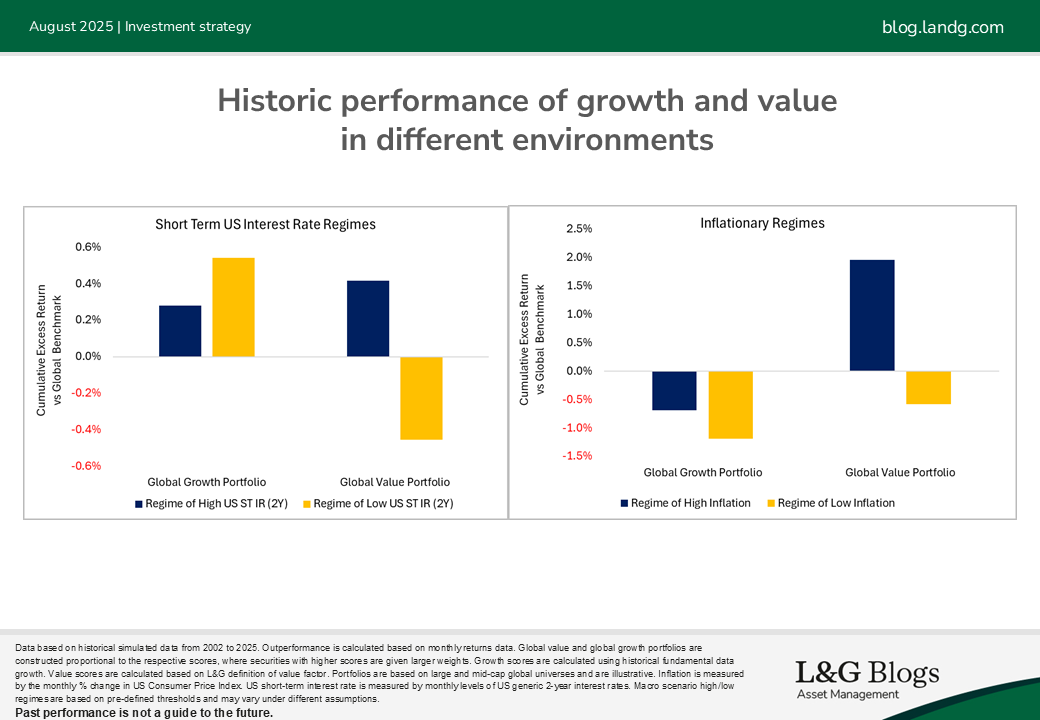

1. The macroeconomic argument

In low short-term interest rate regimes, an example of a risk-on environment, global growth stocks have historically tended to outperform their value counterparts, as presented in below (left chart, yellow bars). Under high inflationary regimes, we see that global value has historically tended to outperform global growth, (right chart, blue bars).

An integrated approach

While valuations and company fundamentals may frame growth as not anti-value, growth and value strategies have unique risk and return profiles across different macroeconomic scenarios.

Framing the answer to the question ‘is growth anti-value?’ as a binary choice between ‘yes’ or ‘no’ obscures the complex reality of market dynamics.

Instead, we believe adopting a style-agnostic approach when designing each investment strategy increases potential for investors to capture distinct return drivers and to benefit from diversification[4] by marrying the two in a multi-factor growth and value strategy.

[1] Fama and French (2019) ‘The Anatomy of Value and Growth Stock Returns’ and Capul, Rowley and Sharpe (1993) ‘International Value and Growth Stock Returns’, where Growth stocks are defined as stocks with high price-to-book ratios.

[2] Piotroski, J.D., 2000, Value investing: the use of historical financial statement information to separate winners from losers. Hou, K. and Moskowitz, T.J., 2005. Market frictions, price delay, and the cross-section of expected returns. Piotroski, J. D. and So, E.C., 2012, Identifying expectation errors in value/glamour strategies: a fundamental analysis approach.

[3] Growth scores are calculated using historical fundamental data growth. Value scores are calculated based on L&G definition of value factor. The scores range from 0 to 100, where 0 is low, 50 is neutral and 100 is high.

[4] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.