Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Amid global uncertainty, what role can EMD play in insurance portfolios?

What potential benefits could it offer insurers – and what considerations do they need to take into account?

The high degree of recent policy volatility emerging from the US has led to huge uncertainty for market participants. Given their significant exposures to tariff risk, certain emerging markets could face meaningful economic impacts in various possible scenarios.

In recent years, emerging market debt (EMD) has become a fixture in insurance general account portfolios, with investors drawn in by the possibility of a capital-adjusted return pickup and potential diversification benefits. It can also fit well into insurers’ asset liability management (ALM) providing contractual cashflows to match liabilities and manage accounting volatility.

However, as ever with insurers, it is not a case of one-size-fits-all. Below we’ll explore three parts of the insurance general account where EMD features and share our thoughts on three actions we think could benefit insurers under present conditions.

1. Life insurer matching portfolio

Historically, EMD was not a mainstream choice for life insurers' matching portfolios due to its generally sub-investment grade credit quality and short duration. However, as EMD markets have developed and credit quality has improved, insurers are increasingly investing in sleeves of long-duration investment grade EMD alongside investment grade developed market (IG DM) credit. Life insurers have been attracted by the return pickup (we have built portfolios at 50-100bps over broadly rating- and duration-equivalent DM credit), potential diversification benefits, and the ability to construct long-duration portfolios – we have helped our insurance clients to build diversified EM sleeves with durations of 10 or more years.

A low-turnover approach is often adopted to minimise accounting volatility, especially for insurers that treat EMD portfolios as Fair Value through Other Comprehensive Income (FVOCI) under IFRS9. Like any credit portfolio, bottom-up credit research is critical for both day-one selection and ongoing credit monitoring.

Portfolios are almost always in hard currencies (usually US dollars) and hedged via currency derivatives such as cross-currency swaps to the currency of the insurer’s liabilities.

Where cross-currency swaps are used for hedging, the EM bonds are typically not accepted as eligible collateral so a buffer of other assets (e.g. sovereign bonds or DM credit) is needed as a derivative collateral buffer. Other structures, such as SPIRE notes[1], can be used where insurers need EMD to be ‘self-collateralised’.

2. Non-life insurer matching portfolio

In the cases of non-life insurers, liabilities are generally shorter duration (around 2-3 years or less) and less certain. In our view, EMD markets are fertile ground for building short-duration portfolios, with approximately 45% of the hard currency universe with a maturity of less than five years. This can skew towards corporates, and the natural turnovers (as short-duration portfolios run-off) are supportive of an active approach and rotation.

3. Return-seeking / surplus portfolios

These include the return-seeking/growth part of a participating fund (where the insurer and policyholder share the risk) and insurers’ surplus portfolio (i.e. assets are greater than liabilities).

More risk is typically taken here, with insurers both investing across the credit spectrum, including sub-IG, and sometimes allocating to unhedged local currency EMD exposures – although historically local currencies have displayed added volatility but little or no additional returns. Additionally, high currency risk capital charges under different global insurance regulatory regimes can discourage insurers from taking EM local currency risk.

What actions should insurers consider?

We see three key actions:

1) Focus on avoiding the losers

We believe there is an information asymmetry within emerging markets that we believe favours the active style L&G specialises in.

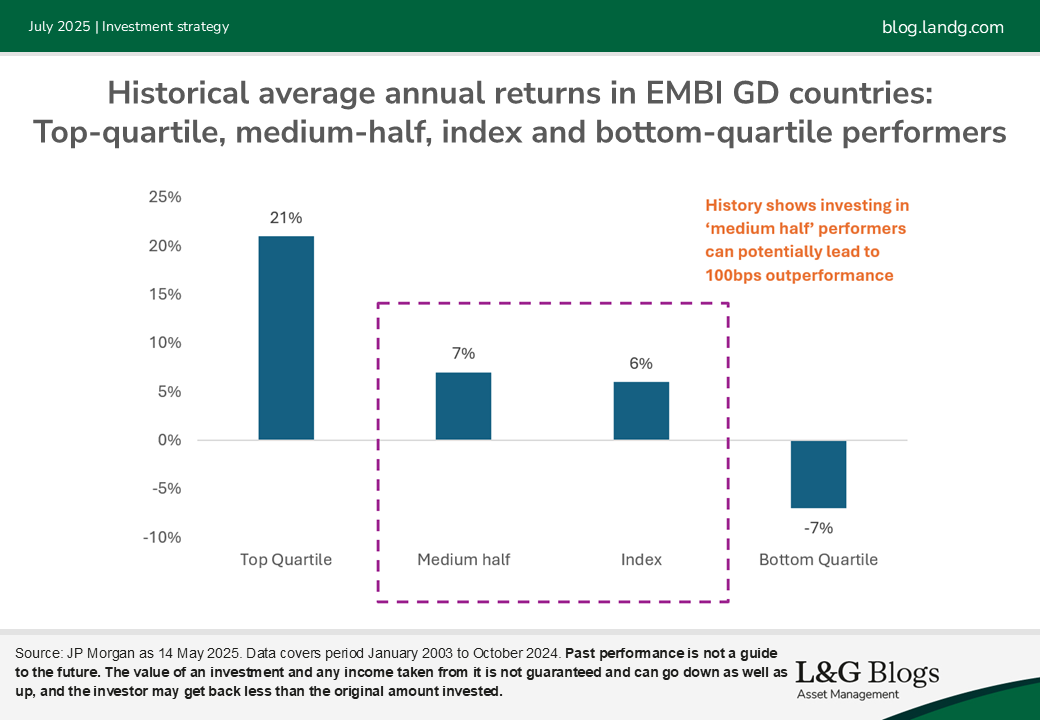

Historical analysis shows that active managers can outperform the index by just investing in median countries and avoiding the tails, as we can see on the chart below. Of course, identifying winners enhances the returns; however, we believe it is more important to avoid losers than identifying winners.

2) Consider an EM private debt allocation

Historically, few insurers have ventured into EM private debt markets due to their specific risk appetites and prudent person considerations. This is starting to change as insurance balance sheet-friendly investment opportunities emerge.

For example, at L&G we have invested in our Nature and Social Outcomes private debt strategy for our own insurance balance sheet. This strategy funds conservation in emerging market countries, guaranteed by international organisations. In addition to offering potentially attractive rating-adjusted return pick-up versus public markets and long maturities to back long liabilities, these assets can support insurers’ ESG objectives, making an impact where it matters most.

3) View your portfolio through a new diversification lens

EMD is often harnessed for the diversification benefits it can offer portfolios. It’s still too early to know for certain what the new contours of international trade will be in the wake of the Trump administration’s tariff policies, but it is conceivable that the world economy will segregate into distinct trading blocs. This could then become another diversification lens in which to manage your portfolio – but only time will tell..

It should be noted that diversification is no guarantee against a loss in a declining market.

[1] Single Platform Investment Repackaging Entity

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.