Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Active Fixed Income Outlook: Politics vs. economics

Could markets soon be wrestling with the consequences of fiscal dominance on the streets and debt mountains on the spreadsheets?

This article is an extract from our Q3 2025 Active Fixed Income outlook.

Fiscal sustainability is a live conversation in financial markets.

Many of the significant themes we have been focused on since the pandemic not only remain powerful forces, but have actually been amplified by the current geopolitical backdrop.

Most now acknowledge that the pandemic was the catalyst for a seismic shift to fiscal dominance. It created both a moral and economic case for fiscal policy; developed countries in particular deployed it aggressively. Since then, we have witnessed further fiscal largesse as governments have had to respond to a number of challenges to growth and they have repeatedly turned on the fiscal taps.

For example, when gas prices spiked after Russia invaded Ukraine, governments rolled out a variety of support packages to shield consumers and industry from the full force of the impact (>+120%). We also saw expansionary fiscal policy in the US in 2023 to support infrastructure construction, emergency assistance for Ukraine, and healthcare. Meanwhile, the UK implemented a mortgage interest payments scheme to help homeowners when interest rates rose significantly in 2022

Fragility exposed

The pandemic was part of a trifecta of shocks that highlighted the fragility of the global economic system.

In 2008, the GFC exposed the fragility of the banking system, Covid exposed fragilities in company supply chains, and the complex network of conflict and competition in Russia/Ukraine, US/China and the Middle East has highlighted geopolitical fragilities.

Having ruthlessly prioritised efficiency in previous cycles, we now see a rebalancing away from efficiency towards resiliency. ‘Liberation Day’ told us that the fundamentally transactional President Trump believes in tariffs as the means of returning a manufacturing base to the US. This means that America now has to reengineer global supply chains at the same time as the rest of the world is forced to do the same, while considering whether the US can be a trusted long-term partner.

In short, systemic resilience is now receiving priority over economic efficiency and profit maximisation. A transition of this significance will be costly and could lower productivity. It could continue the trend towards a home-first approach which could further increase international tensions.

A debt spiral?

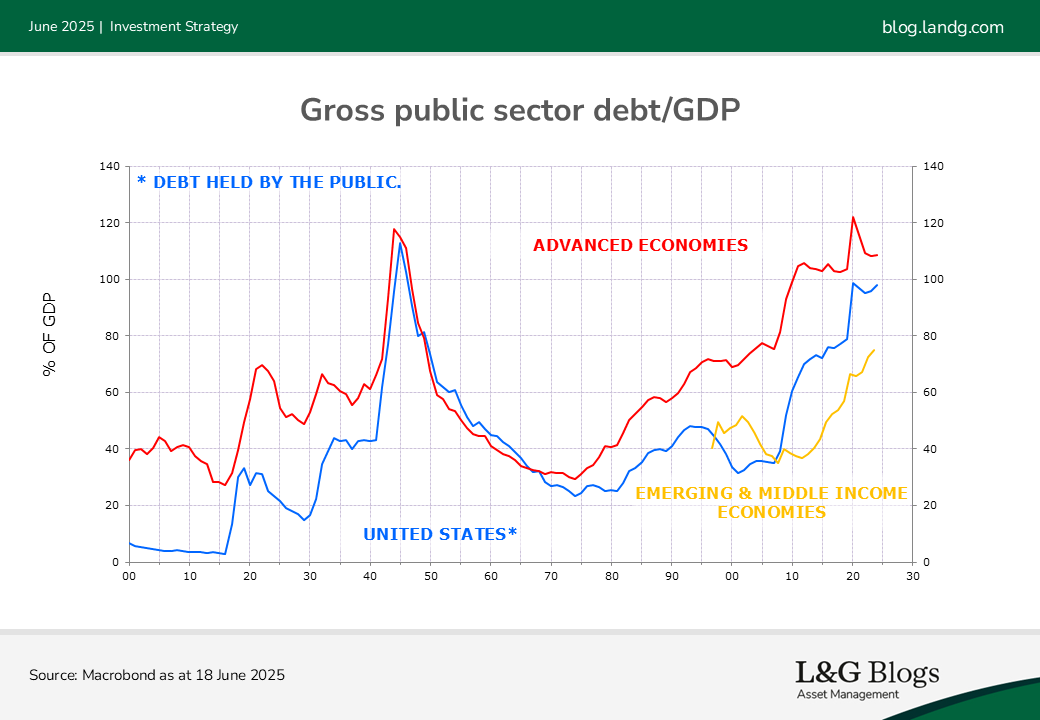

As we can see in the chart below, current projections of rising debt levels are unsustainable. Trump’s tax-slashing ‘One Big Beautiful Bill Act’, the release of Germany's constitutional 'debt brake', and recent corporate tax breaks all raise the question – have those developed economies that deployed their fiscal weapons so aggressively now realised that the only way out of this debt fiasco is to focus on boosting growth?

As investors keep a watchful eye on debt/GDP ratios, the point to realise is that what are feasible now is lower than they have been only recently. If you believe rates/yields could be structurally higher, then the forward-looking point is that funding large public deficits will be more difficult with structurally higher levels of investment required to re-shore, on-shore and friend-shore production in today’s world. In addition, defence spending, climate risk mitigation and a global spending spree on the infrastructure powering artificial intelligence are all other areas of investment driving this trend.

We have repeatedly highlighted how powerful these forces are and the potential impact they could have on markets – not least fixed income ones. That view has not changed.

This article is an extract from our Q3 2025 Active Fixed Income outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.