Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

A bird in the hand: why dividends matter

Dividends can potentially provide a valuable source of stability in periods of volatility, and may also be indicative of superior profitability. But the investment strategy matters – not all dividends are sustainable.

Key takeaways

- Dividends have historically fluctuated less than share prices, offering a steady source of potential returns

- Incorporating return on equity (ROE), long-term dividend growth and quality screening into a dividend investment strategy can help investors to avoid unsustainable dividend payers

- A liquidity-aware, equal-weight approach can avoid concentration risk in dividend income strategies, helping to maintain diversification[1]

The logic behind the expression ‘a bird in the hand is worth two in the bush’ is straightforward: yes, it’s nice to have two birds, but there’s definite value in the one you’ve actually caught.

In 1963 Myron Gordon and John Lintner latched onto the phrase to explain the enduring appeal of dividend-paying stocks.

In a neat counterpoint to theories arguing investors are indifferent about whether their returns come from dividends or capital gains, their theory suggests stocks with high dividend payouts are sought out by investors who prefer the dividend ‘in the hand’ to capital growth ‘in the bush’.

A steady source of returns?

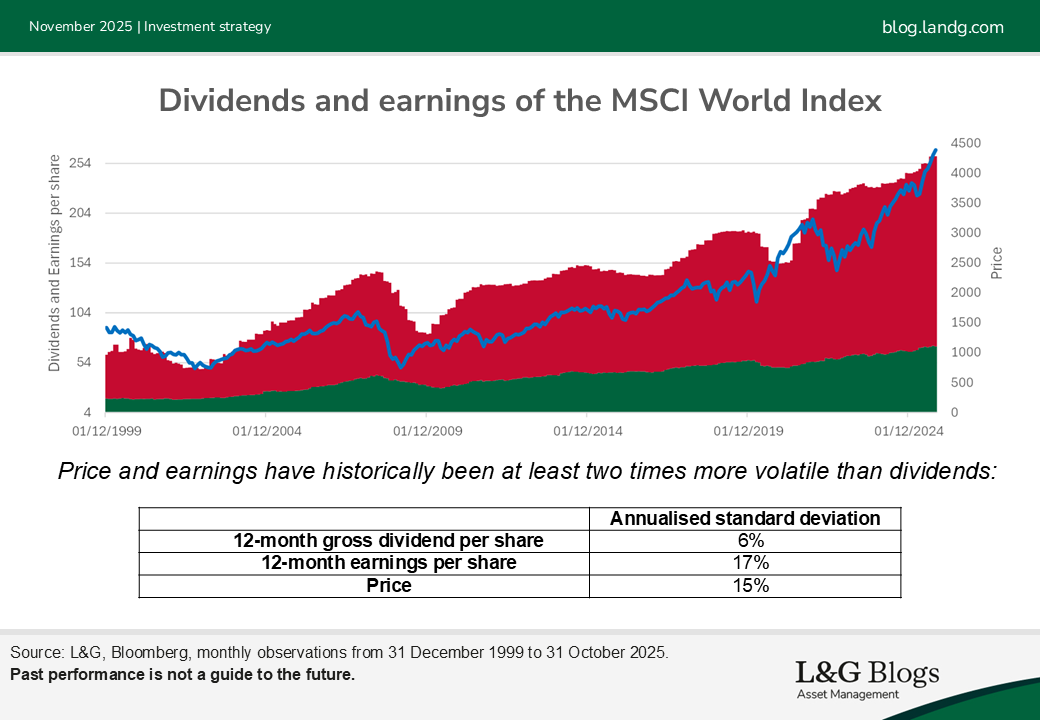

For investors, one of the key appeals of sustainable dividend payers is that those companies will typically aim to maintain those payments and keep returning capital to shareholders through times of high and low earnings.

This mean dividends have historically fluctuated less than share prices, as shown below.

As well as providing greater visibility for investors, dividends have historically been a potential indication of companies with improved profitability.

By examining a global all-cap universe of 5,418 companies, we can see that the 1,936 companies that have paid dividends in the past 12 months can compare favourably on a range of metrics, on average, as shown in the chart below.

Mind the dividend trap

Despite these clear arguments in favour of dividend-paying companies, it’s important to distinguish between steady, sustainable payers and potential dividend traps.

Companies that use retained earnings to pay unsustainable dividends may soon find their cash piles dwindling. This can lead to dividend suspension and negative share price surprises.

Sustainability of dividends is particularly crucial as research[2] indicates that a surprise dividend cut has historically typically resulted in a share price reaction of around double the magnitude of that in response to a similar dividend rise.

Three ways to target sustainable dividend payers

We believe there are three practical ways that investors can aim to identify sustainable dividend payers and dodge the dividend trap:

1. Look at ROE to measure profitability relative to equity value invested in by shareholders

2. A long (10-year) positive trend in dividend growth provides evidence of consistency of past dividends

3. Quality screening that assesses profitability and leverage

- Return on assets (ROA): is the company generating profits efficiently in relation to its assets?

- Change in asset turnover: are companies improving their asset turnover over time? Is this being done organically or in sudden steps?

- Accruals (in the negative): is the firm able to collect its profitability? Is income truly reflecting the financial position of the firm?

- Leverage: Is the company’s cash sufficient to pay out its debt? Sometimes it can be ok to have debt, as long as it is manageable and healthy.

Dividends and diversification

Putting the potential benefits of dividend-paying companies into a wider portfolio context, it’s important to recognise that it is possible to target this source of income without sacrificing diversification[3] – but it requires a thoughtful approach to investment strategy.

If a dividend-seeking strategy weights stocks by dividend yield this may result in a relatively concentrated portfolio, with high allocations to the companies that have the highest yields.

But there’s another way: an equal-weighting approach can capture the potential benefits of dividends while preserving diversification.

In our view, dividends are a crucial part of the potential returns on offer from equity markets. The key, we believe, is to be selective and focus on companies that have a history of making sustainable

[1] It should be noted that diversification is no guarantee against a loss in a declining market.

[2] Source: Dividends as Reference Points by Malcolm Baker and Jeffrey Wurgler, 2011.

[3] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.