Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Probing the market impact of productivity gains

We survey what AI might mean for GDP growth, corporate margins, equities and fixed income.

The following is an extract from our latest CIO Outlook.

How excited should we be about the AI revolution? Some analysts suggest it could boost global growth by around 1% per year through to 2030. This sounds great, with two caveats.

One, we’re running to stand still with ageing demographics hurting trend growth.

Two, are we double counting? We had mainframes, then PCs, then the internet then mobile internet. AI refutes Robert Gordon’s dire warnings of the peak of technology, but it’s hard to pinpoint how much better it will be than everyone’s implicit extrapolation of previous innovations.

In other words, technologies like AI have always been needed to fulfil analysts’ long-term growth projections.

Getting with the program

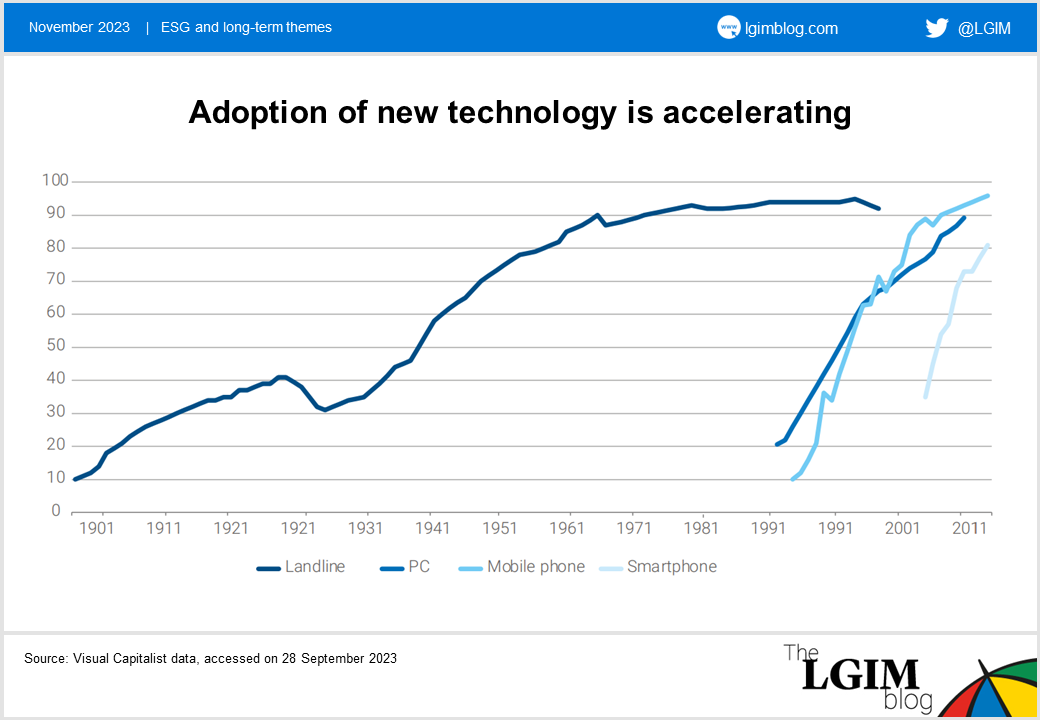

Of course, it’s not just technological development that matters, but the rate of adoption. There’s good news here in that recent technologies have become mainstream faster than previous innovations did, as illustrated in the chart. That augurs well for the future.

We believe the benefits of AI are most likely to show up in corporate earnings before they appear in GDP data.

First, statisticians notoriously struggle with new technologies, particularly new products with no comparison. For example, the introduction of Netflix* was not counted as a lower cost/higher volume for movie rentals (Source).

Second, AI is likely to reduce the cost of existing services such as solicitor enquiries, medical consultations or drive-thru orders. Prior research on the corporate response to pandemic-era shortages suggests we have oligopolies rather than perfect competition. We would initially expect higher margins, and then, eventually, lower prices as new entrants compete those margins away.

Could AI delay the recession?

Perhaps, but it’s possible a ‘creative destruction’ recession and job losses are needed to harness its benefits.

Reluctant technology adopters might only make the switch when it’s forced upon them by legacy suppliers going bust, moving us to the steep part of the S-curve of innovation.

The boost to growth might come from displacing knowledge-based workers into other industries, just as the tractor helped displace workers from fields to factories.

Markets could look through any such pain as ‘proof of concept’ productivity enhancements become apparent. It all depends on how many winners and losers we have: will every company adopt AI equally, or will some lag behind and be forced to close? (For more on this theme, see Madeleine and James’s piece.)

What might AI mean for real rates?

In general, stronger productivity growth should boost equity markets and real interest rates. In a classic production function, stronger productivity implies higher returns accruing to both labour and capital. The latter is good news for equity returns, where the ability to produce ‘more with less’ implies consistently higher margins.

However, that impact is likely to be highly asymmetric across the corporate sector. Just as we worry about ‘stranded assets’ from the climate transition, it’s sensible to also worry about large debt-issuing losers from the AI revolution. We believe equity indices, with their constantly evolving constituents, are more likely beneficiaries than credit markets.

The impact on the rates market is less clear. Productivity improvements could bear down on inflation over time, putting downward pressure on yields. Or higher growth could push up the market’s estimate of neutral real interest rates, having the opposite effect.

What we can say is that the benefits are most likely to accrue to those parts of the world whose regulatory environment is most amenable to AI. That implies yet another reason why King Dollar is unlikely to be knocked off its throne anytime soon.

The above is an extract from our latest CIO Outlook.

*For illustrative purposes only. Reference to this and any other security is on a historical basis and does not mean that the security is currently held or will be held within an LGIM portfolio. Such references do not constitute a recommendation to buy or sell any security

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.