Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Limiting global warming to 1.5C is becoming harder, but clean energy growth is keeping hope alive

The IEA has updated its flagship scenario, demonstrating how the world can reach net zero - all parts of society must play their part to achieve this goal.

To limit the average temperature rise to 1.5C, the world should pursue the goal of net zero carbon emissions by 2050.1 Substantial changes to energy supply and demand are needed now and over the coming years. But what changes?

The International Energy Agency (IEA)’s Net Zero Emissions (NZE) scenario is an important tool for identifying potential energy transition goals and assessing progress. IEA scenarios are often referenced by governments, companies, and investors. The recently revised NZE scenario merits attention.

Scenarios are not predictions. There is no way we can predict with a useful degree of certainty what the world will look like in 2030 or 2050. In a dynamic market economy with recurrent crises and complex global political interactions, relying on long-range forecasts is of limited utility. However, we believe scenarios, if used wisely as illustrations, can help us focus on choices we need to make.

Bad and good news

Compared with its original scenario published in 2021, “the path to achieving net zero emissions by 2050… is a steeper one… and requires more to be done after 2030”.2 This is because the economy rebounded more strongly than expected post pandemic, with higher emissions, and because insufficient action has been taken to mitigate climate change.

The deployment of wind, hydrogen, and carbon capture, utilisation and storage (CCUS) has been downgraded, reflecting supply chain constraints, delays in scaling up pipelines and related infrastructure, and slow progress in developing market frameworks. More government, regulatory and industry action is required.

Yet in some sectors, the transition has exceeded expectations. The IEA notes that “currently announced manufacturing capacity expansions for solar photovoltaic (PV) and batteries would be sufficient to meet demand by 2030”.3 Record growth in electric car sales is also in line with its pathway to meet net-zero emissions by 2050.4

These developments reflect market economics. The energy crisis increased fossil fuel prices, making clean energy relatively cheaper even as new fossil fuel supplies were sought. Supply, and innovation, has been responding to demand. Government subsidies for electric vehicles (EVs) and prescribed phase-outs of petrol and diesel car production have helped too. Solar PV generation and EVs therefore have a more prominent role in the new NZE scenario.

The IEA is also positive about further roll-out of clean energy technology, for example as innovation finds ways to offset supply bottlenecks in critical minerals.

A route to net zero

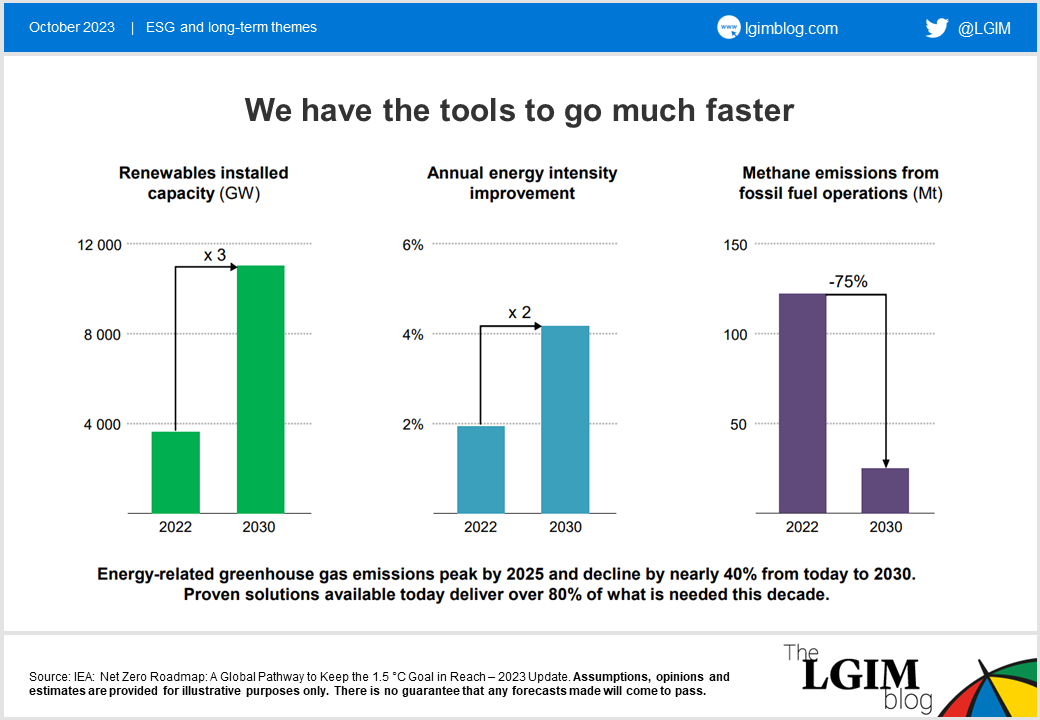

The IEA’s revised scenario requires fossil-fuel demand to fall by over 25% to 2030, driven by substantial increases in renewable energy and significant improvements in energy intensity. At the same time, there should be sharp cuts in methane emissions.

In addition, electricity transmission and distribution grids need to expand by around 2 million kilometres each year to 2030, with further energy infrastructure investment elsewhere. Clean energy investment in developing countries needs to rise rapidly.

The IEA also suggests that countries – governments – should bring forward their net zero target dates. Developed countries should move faster, achieving net zero by 2045, China by 2050, and other emerging market and developing countries afterwards. This reflects in large part degrees of coal dependency.

Implications for companies

The IEA is clear that “there is no need for investment in new coal, oil and natural gas… No new long-lead time upstream oil and gas projects are needed in the NZE Scenario, neither are new coal mines, mine extensions or new unabated coal plants,” anywhere in the world.5

However, continued investment in existing oil and gas assets and projects already approved is incorporated. This is because “the decline of fossil fuel supply investment and the increase in clean energy investment is vital if damaging price spikes or supply gluts are to be avoided”.6

To align with this scenario, we believe oil and gas companies need to maintain strategies consistent with a decline in fossil fuel demand to 2050. Doing otherwise risks financial cost in a world approaching net zero. The very business model of an unaligned oil and gas company is therefore challenged.

The role of investors

We believe investors should continue to test companies’ resilience to this and other similar scenarios. LGIM does this through its Climate Impact Pledge. Companies need to show how they are aligning with a global net zero outcome. If they are not aligned, we may vote against them. In cases where it’s consistent with the fund objectives, we may also divest.

The IEA has published a detailed and credible scenario of how the world can attain net zero and limit global warming to 1.5oC. It shows how attaining net zero is within our grasp.

All parts of society – governments, companies, investors, and others – need to play their part.

Key risks

Any views expressed are those of LGIM as at October 2023. The value of investments and the income from them can go down as well as up and you may not get back the amount invested. Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

1. Source: IPCC Special Report Global Warming of 1.5C (2018) and IPCC AR6 Synthesis Report Climate Change 2023. To limit temperature rise to 1.5C with little or no overshoot.

2. Source: Net Zero Roadmap: A Global Pathway to Keep the 1.5 °C Goal in Reach - 2023 Update (windows.net)

3. Source: ibid.

4. Source: https://www.iea.org/reports/global-ev-outlook-2023/trends-in-electric-light-duty-vehicles

5. Source: ibid.

6. Source: ibid.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.