Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Israel-Hamas conflict: implications for investors

What the hostilities in the Middle East mean for markets and the global economy.

The unprecedented attack on Israel by Hamas, and ensuing hostilities, are first and foremost a human tragedy. Our thoughts are with everyone impacted.

At LGIM, our clients’ exposure to Israeli assets is minimal, largely via index equity holdings. As such, we anticipate a limited impact on client portfolios, while remaining mindful of potential ramifications as the situation evolves.

In this post, we discuss the immediate market impact and potential longer-term geopolitical implications of this developing situation, which we continue to monitor on behalf of our clients.

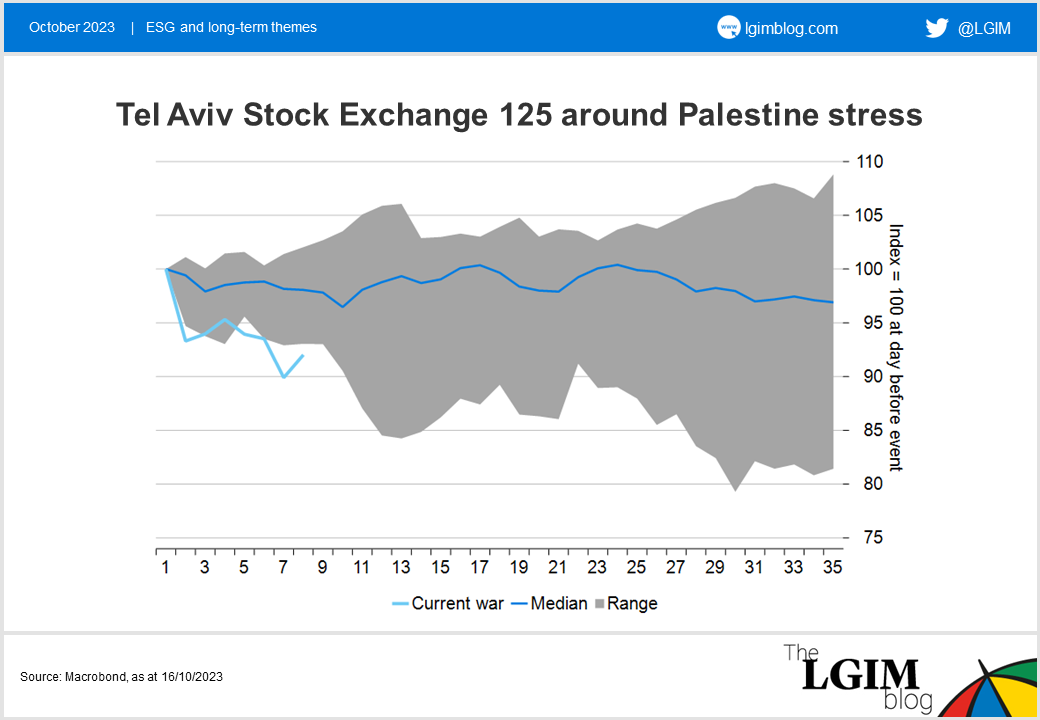

Impact on Israeli assets

The chart below shows the immediate impact of hostilities on the Tel Aviv stock exchange relative to the reaction after previous escalations in hostilities. Historic data points indicate that equities performed in line with the worst of previous episodes (Operation Defensive Shield in 2002).

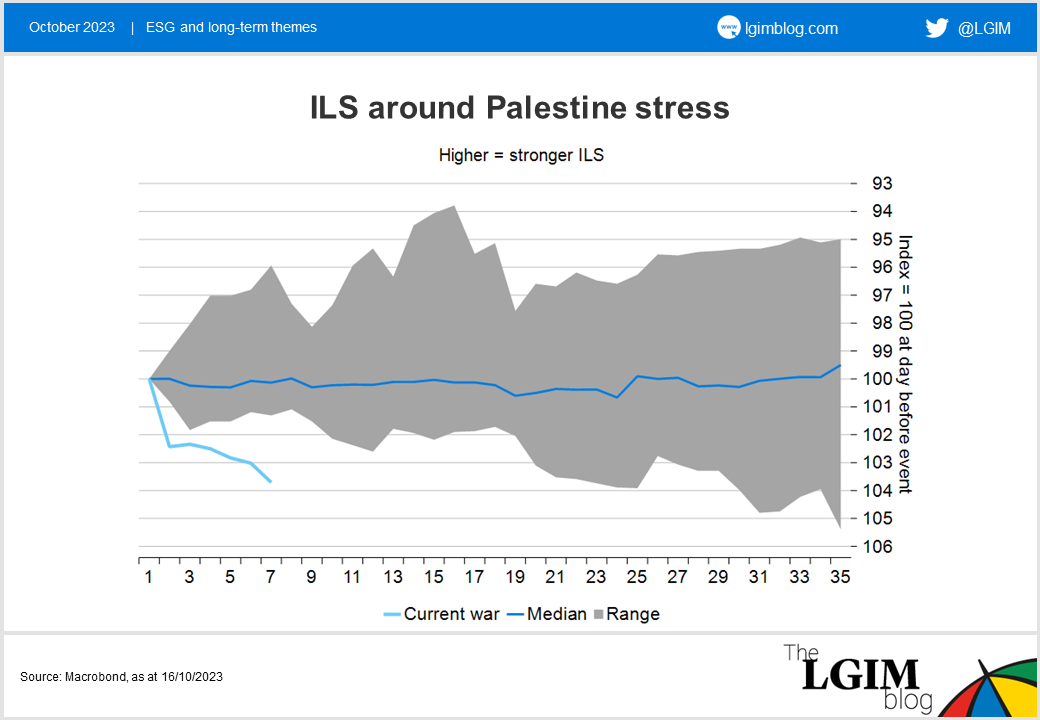

The Israeli currency, meanwhile, fell more than it has during previous periods of stress:

We think the shekel embeds a significant risk premium given the political backdrop at current levels. The premium also in part reflects institutional uncertainty associated with Israel’s planned judicial reform, which if successfully enacted would limit the Supreme Court’s ability to challenge government decisions. In our view, the current crisis makes the passing of the judicial reform less probable.

We believe Israel’s very sound fundamentals provide a firm foundation for the currency.

The country runs a current account surplus and reserves that amount to close to 40% of GDP.1 Indeed, in response to the hostilities, Israel’s central bank announced that it would spend $45 billion to support the shekel.2

Global market reaction

The immediate impact on global markets has been relatively limited thus far. Oil prices have edged higher, while developed-market government bond yields have declined, partly reflecting their status as safe-haven assets in periods of heightened uncertainty.

The situation in Israel and Gaza is evolving with great speed, and as always our mantra is “prepare, don’t predict”. However, we do see value in assessing potential scenarios, and how these might intersect with long-term geopolitical themes.

The key near-term risk is that the hostilities escalate into a wider conflict, involving Hezbollah and Iran. We would expect a larger market reaction if this happens.

In this scenario, oil prices could rise significantly, potentially weighing on asset prices worldwide and raising the possibility of renewed inflationary pressure. Should the hostilities intensify, pushing oil prices higher, we would expect the European economy to be more affected than the US, given the latter has a larger domestic production base and Europe is already constrained by reduced imports from Russia.

The multi-polar world

We also emphasise how the conflict fits into the broader context of the shift towards a multi-polar world, characterised by Russia’s rising isolation, the intensification of tensions between China and the West, and the polarisation of US politics.

We believe this increases overall geopolitical risk, which could result in rising defence spending, isolationism and inflation.

Important upcoming elections, including in the US, will be shaped in part by how candidates respond to this global geopolitical narrative, as well as the localised conflict in the Middle East.

We will continue to monitor the Israel-Hamas conflict closely and will share our thinking as the situation evolves. Our thoughts will remain with all those affected by this tragedy.

Views expressed as at 16 October 2023. Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.