Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

From post-AGM to pre-AGM: Japan’s efforts to reform annual disclosure practices

As Japan’s AGM season wraps up, it’s a timely moment to revisit the expectations we’ve communicated on long-standing issues like AGM clustering, disclosure timelines, and audit-related reforms — and to see what progress has been made.

Back in 2020, we wrote about two key challenges in Japan’s AGM season: the heavy concentration of AGMs in June and persistent delays in publishing the Yuho (annual securities report). We also published suggestions for companies and policymakers to help address these issues, which have, in our view, long limited meaningful shareholder dialogue and undermined the effectiveness of proxy voting.

A breakthrough in Yuho timing

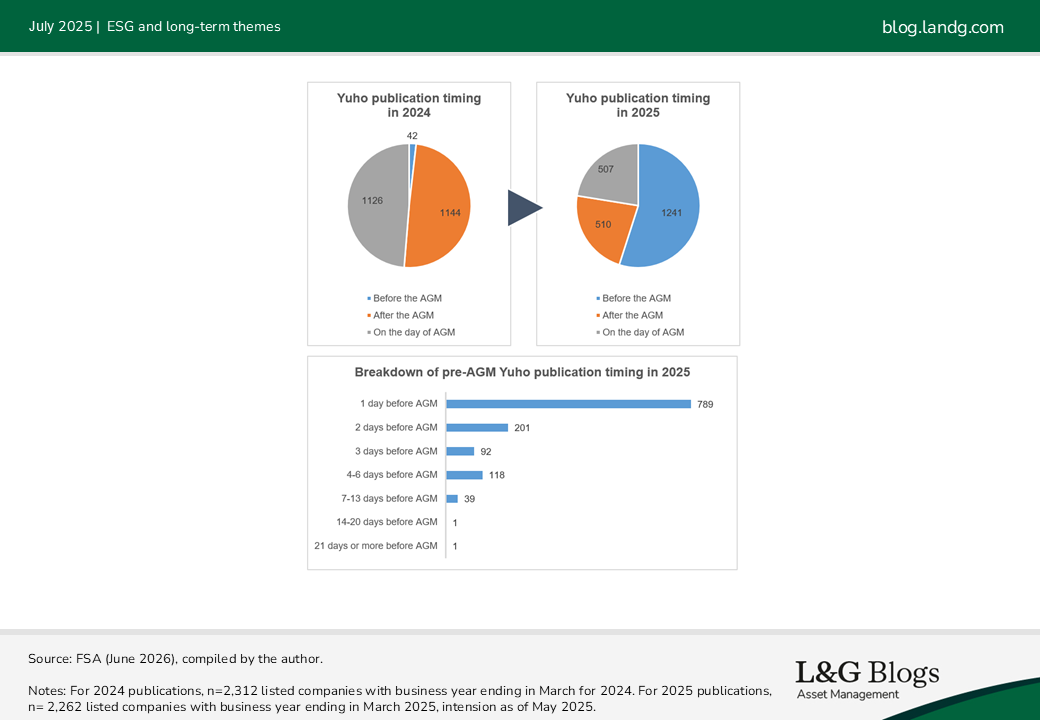

In a significant development, Japan’s Financial Services Agency (FSA) recently revealed that 54.9% of companies with March fiscal year (FY) ends had immediate plans (as at end May) to publish their Yuho before the AGM, up from just 1.8% last year. This surge follows a March 2025 call by the Finance Minister for earlier Yuho publication. The TSE Prime Market is leading the way, with two-thirds of companies aiming to disclose in advance of the AGM.

This represents a sea change in disclosure practice. Previously, over 80% of companies released their Yuho on the day of the AGM or the day after, giving investors no time to absorb critical information on corporate governance, capital allocation, and risk factors before voting.

The drivers? A coordinated push from regulators, likely recognising the continued pressure from global institutional investors, and a growing understanding among issuers that meaningful dialogue requires meaningful transparency.

A strong start, but work remains

Crucially, however, only a handful of companies currently meet the gold standard of disclosing at least three weeks before the AGM, according to the FSA. Among 2,262 March-year companies, 41 (1.8%) said they would publish at least one week prior to the AGM. While this marks an increase from just 11 (0.4%) last year, we believe real investor dialogue requires time. Roughly a third (789 companies) indicated plans to release their Yuho the day before the AGM, but, in our view, publication on the eve of an AGM doesn’t serve much purpose.

SSBJ mandates will raise the stakes

The case for earlier Yuho publication will only strengthen as sustainability disclosure requirements come into play. From FY ending March 2025, companies may voluntarily adopt the Sustainability Standards Board of Japan (SSBJ) standards, aligned with the ISSB’s global standards. These disclosures will be integrated into the Yuho.

Phased mandatory adoption is expected to begin from FY2027 for large Prime Market companies, expanding to all Prime-listed firms in the 2030s. This raises the bar for timing, coordination, and assurance across reporting processes.

If companies wait until just before the AGM to publish, we don’t believe investors will have sufficient time to evaluate and engage on climate-related risks and plans. For Prime Market firms, especially those with global shareholders, early and robust disclosure will become essential, not just for good governance, but for credibility on sustainability.

Looking back and ahead: From momentum to lasting reform

While legal or regulatory support can help solidify recent progress, it's important to reiterate that companies are not legally required to hold their AGMs in June, despite common practice. While concerns remain around audit capacity, dividend timing, and shareholder expectations, there are positive signs of openness to change. We applaud the FSA’s initiatives and collaborative efforts to address these challenges.

For many years, we have called on companies to hold their AGMs after the Yuho publication. In our 2020 blog, we suggested one way to do this with more breathing room was to decouple the fiscal year-end and the record date (the cutoff for determining shareholder eligibility). A small number of companies have already taken this step, and we continue to support companies seeking to make such changes at their AGMs.

For policymakers, we suggested streamlining audits and quarterly reporting requirements. This has partly been addressed, with updates made to the quarterly reporting requirements under the Financial Exchange and Instruments Act.

We are pleased to have contributed to the conversation with companies, policymakers, and media, both directly and alongside peers such as ICGN and ACGA. Yet, this is just the starting point. The next few years must convert this momentum into lasting reform to ensure early, meaningful disclosure becomes standard practice rather than a notable exception.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.