Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

From cloud to cash: How hyperscalers are funding AI expansion

Big Tech’s funding of AI infrastructure is well known. In this blog, we address how hyperscalers are financing their efforts in the technology and answer questions around whether these initiatives are sustainable.

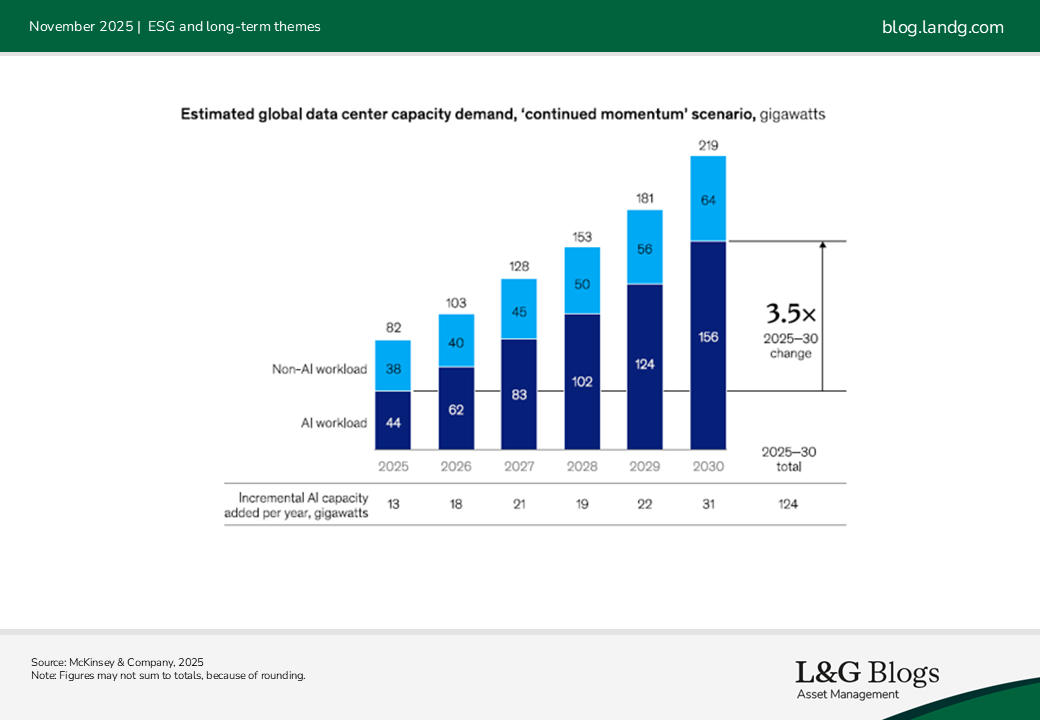

The race to build AI-ready data centres is accelerating and it appears increasingly expensive. Estimates of global capital expenditure on AI infrastructure range from $2.5 trillion to $6.7 trillion by 2030[1]. At the heart of this buildout are the hyperscalers: Amazon AWS*, Microsoft Azure*, Google Cloud*, Meta, and Oracle are collectively responsible for over 75% of global cloud infrastructure capacity. Removing our head from the clouds requires determining how they plan to fund this scale of investment, and what risks lie ahead?

The capacity crunch

Demand for generative AI and other advanced models is driving a wave of construction across the globe. These ‘AI factories’ – i.e., massive, GPU-packed data centres require unprecedented computing power and energy density. With limited visibility of future demand and lagging investment, hyperscalers remain short of capacity, limiting their ability to monetise customer commitments. This supply-demand imbalance is expected to persist in the near term.

What’s being invested near term?

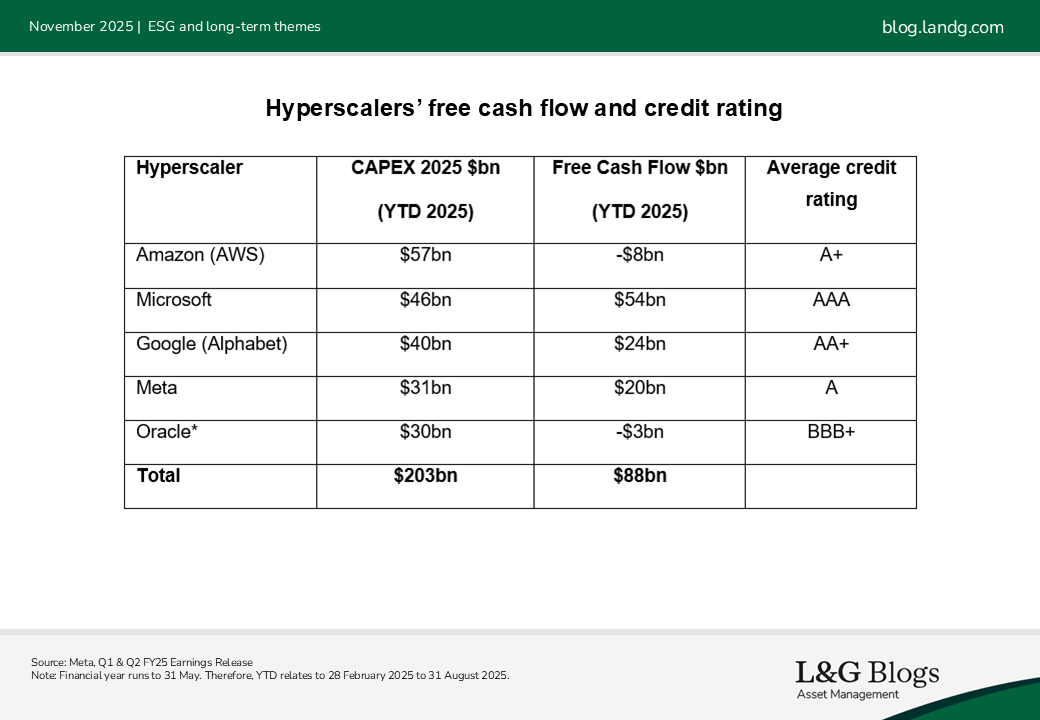

Hyperscaler capital expenditure is surging, financing their AI data centre expansion through a blend of internal and external sources. The primary source is free cash flow, with these firms reinvesting billions of their operating profits into infrastructure buildouts. For example, Microsoft and Amazon have committed tens of billions annually to AI-related capex, largely funded from retained earnings. Despite their sizeable current commitments, forecasts suggest that, to meet demand, over half of the required investment will need to be sourced from alternative funding methods – debt, for example. Barclays has projected capital expenditure for the hyperscalers to reach $500bn by 2027[2], a sizeable increase relative to today’s investments, but nowhere near the magnitude of investment being floated by researchers.

Hyperscalers are able to tap public credit markets (although they are yet to in the magnitude expected), issuing corporate bonds at attractive rates thanks to their strong credit ratings. In October 2025, coupled with their Q3 results, we’ve seen the beginnings of the public credit issuance from the hyperscalers in sizeable blocks, with Oracle, Meta and Google all announcing deals. Increasingly, we’ve seen hyperscalers accessing private credit markets, particularly for bespoke or off-balance-sheet projects; Meta’s recent $29 billion public/private credit deal is a notable example[3]. Some operators are exploring securitisation, packaging long-term lease income from data centres into asset-backed securities (ABS) to raise capital while keeping debt off the parent company’s balance sheet. Given the size of the private credit and securitised markets they are likely unable to absorb all of the proposed issuance. We expect that hyperscalers may increasingly need to use hybrid deals to source funding. This diversified capital stack may enable hyperscalers to maintain flexibility, manage risk, and scale rapidly in response to surging AI compute demand.

Head in the clouds - incentivising investment

The One Big Beautiful Bill Act (OBBBA), enacted on 4 July 2025, marks a pivotal shift for hyperscalers investing in AI infrastructure. Under the legislation, businesses can now immediately deduct 100% of the cost of qualified property – such as servers, GPUs, and data centre equipment – in the year it is placed in service, rather than depreciating it over time. This change delivers a substantial liquidity boost through tax savings, freeing up capital for reinvestment. The time value of money further amplifies the benefit, as early deductions carry greater financial impact due to inflation and opportunity cost. For hyperscalers, this accelerated depreciation aligns with their aggressive expansion strategies, enabling them to maximise near-term returns and scale infrastructure rapidly.

Meanwhile in Europe, the pursuit of AI sovereignty has resulted in many partnerships across countries and hyperscalers to provide digital autonomy. These public-private partnerships are supported by the grants offered by the Strategic Technologies for Europe Platform (STEP) Programme, which encompasses the Digital Europe Programme (worth €8.1bn[4]). As a result, Microsoft, Amazon and Google have all launched EU initiatives to capture the opportunity, diversifying their investments geographically.

Feet on the ground - recognising the risks

Commentators have mused that AI offers efficiency gains and the prospect of sky-high profits for years, yet we have not seen necessarily seen these gains come to fruition. Many hyperscalers do face a shortage of capacity, limiting their ability to convert customer commitments into revenue. While this supply-demand imbalance creates urgency, the rush to capture near-term gains comes with significant risks. This revenue uncertainty is compounded by the possible obsolescence of data centres as the demands of AI increase. As long-lived assets, often with useful lives exceeding 15 years, data centres may require additional capital and retrofitting to keep up with shifts in technology.

Model advances may continue to require additional compute from data centres or suggest migration towards decentralised architectures. Graphics processing units (essential chips for AI) appear to have a short shelf life before they are reassigned to more basic tasks, requiring consistent spending to keep data centres abreast. Could the ongoing upkeep render today’s hyperscaler investments less relevant or even obsolete before their full value is realised?

Should revenues linked to AI fail to materialise in the scale expected, this might prove catastrophic for the industry. The circularity with chipmakers investing in operators (i.e., the hyperscalers) has raised concerns from some investors. A complicated web of transactions has created its own self-fulfilling financial ecosystem that faces a sizeable challenge. Hyperscalers must deliver a plausible method of generating revenue through their platforms to ensure this city in the clouds doesn’t come crashing down.

Summary

Despite the staggering scale of investment required to support AI infrastructure, the largest hyperscalers appear well-positioned to manage the financial burden in the short term. Strong free cash flow, benefitted by tax incentives, strong credit ratings, and diversified financing strategies (including private credit and securitisation) give these firms the flexibility to scale rapidly, in our view. While risks like overcapacity and tech obsolescence remain, the current financial and policy environment suggests that it is possible that the aggressive hyperscaler expansion may also be financially sustainable, at least for the Big Tech players.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1] L&G, McKinsey & Company, 2025

[2] Barclays Q3 Global Macro Outlook, 25 September 2025.

[3] ‘Meta seeks $29bn from private credit giants to fund AI data centres’, Financial Times, June 2025

[4] Digital Europe Programme (DIGITAL) | EU Funding & Tenders Portal, 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.