Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

European gas shock: the need for green

Just as the 1970s oil shock reshaped the global automotive industry, so the latest energy shock may lead to a rethink on the built environment.

Russia’s invasion of Ukraine is causing a rethink on European energy policy. European natural gas prices have jumped by 300% over the past year.[1] Natural gas makes up just over 20% of Europe’s total energy needs, and 90% of that is imported – with 45% of this coming from Russia.[2] Politicians have had to rethink security of energy.

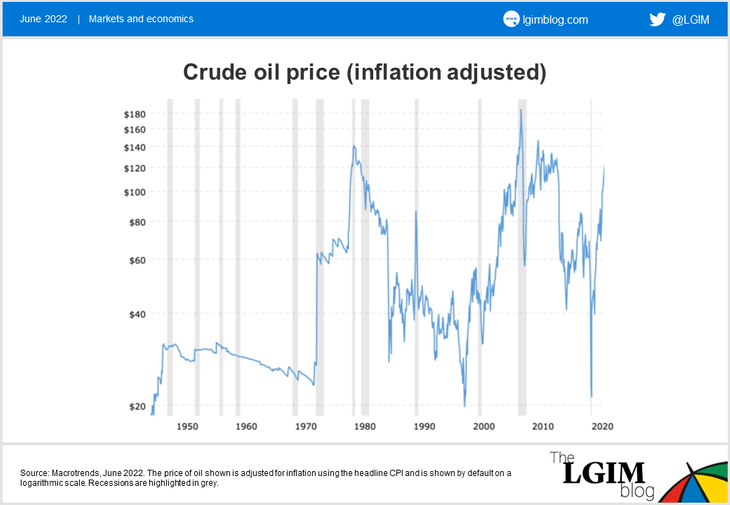

Today’s gas price volatility has historic parallels with the 1970s oil price shock.

A lesson from history

In October 1973 Egypt and Syria attacked Israel, beginning the Yom Kippur war. Russia began sending weapons to Egypt and Syria, while the US supplied Israel. In response, members of the Organisation of Arab Petroleum Exporting Countries embargoed oil shipments to the US, causing a major shock to oil prices and the global economy.

The embargo was short-lived, ending in March 1974, but it left scars. There was petrol rationing in the US and a national highway speed limit of 55 mph was put in place to conserve fuel.

This changed the automotive industry. Prior to the crisis, American giants Ford, General Motors (GM) and Chrysler were building large cars with large, inefficient engines. High pump prices meant American brands struggled, to the benefit of more efficient Japanese imports. Gas guzzlers were hard to shift. In 1974, car sales of GM fell by 36%[3] and it closed 15 of its 22 assembly plants in an effort to reduce the glut of unsold cars.

The crisis led to a recession, the formation of the International Energy Agency (IEA) in 1974, the beginning of the US strategic petroleum reserves in 1975 and the creation of the US Department of Energy in 1977.

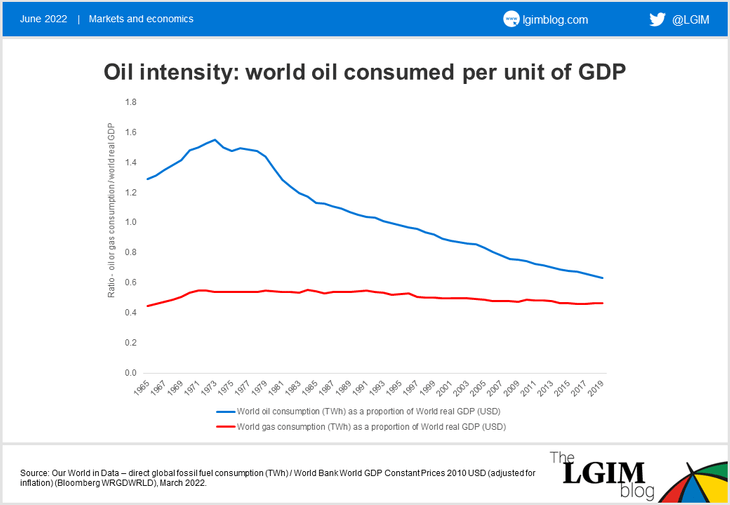

The ripples of the 1973-74 oil price shock can still be felt today. World oil intensity, defined as global oil consumption as a proportion of global gross domestic product, fell year-on-year following the price shock. The world began to use oil more efficiently and diversified its energy sources to drive growth.

If we consider that Europe’s gas price shock is of a similar magnitude to the 1973-74 oil price shock, then there may be similar long-term ramifications for natural gas usage.

The need for green

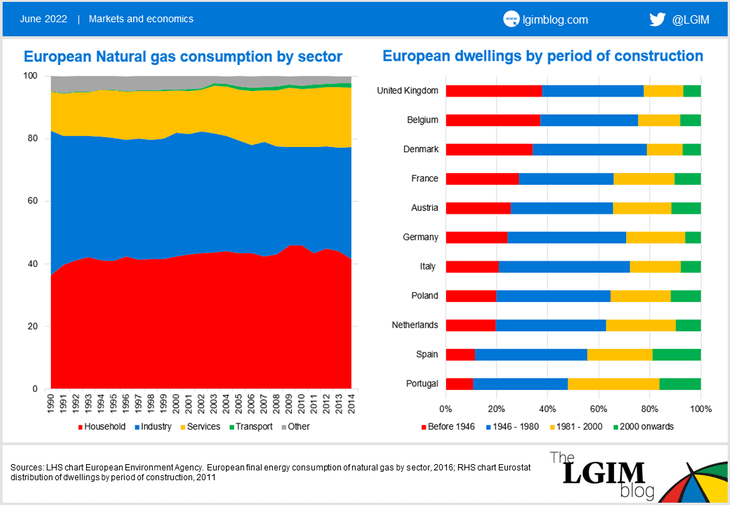

Just as consumers shifted to more fuel-efficient cars in the 1970s, consumers are also likely to seek to use natural gas more efficiently in the years ahead, in my view. Today, buildings comprise around 40% of the EU’s total energy consumption. And the housing stock is energy inefficient, given around 35% of the EU’s buildings are over 50 years old. It’s a similar picture in the UK.

The EU’s long-term aim is for all buildings to have net-zero emissions by 2050. In December 2021, an EU directive proposed that all buildings in the EU with the worst energy rating (G-grade) must be renovated to a higher standard by 2030 and F-grade buildings by 2033. Sustained high gas prices make this legislation less politically sensitive and make it more likely that there will be voluntary self-adoption.

For some buildings, it will be economically unviable to renovate them. In the UK, the housing stock age for many housing associations is old. This complicates the problem of meeting a social housing shortfall with the government’s 2050 carbon neutral commitment, a point made by my colleagues in a previous blog.

Just as the 1973-74 oil price shock changed the automotive industry, the 2022 European gas price shock is likely to reverberate for decades, changing the European architectural cityscape forever.

[1] Source: Bloomberg, World Bank commodity prices Natural Gas Europe

[2] Source: Eurostat, 2020

[3] New York Times article The Energy Trauma at General Motors, March 1974

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.