Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Does decarbonisation alter investment objectives?

In a follow-up to our 2022 research, we have modelled portfolios using the latest data to explore whether conventional investment objectives are compatible with decarbonisation.

Decarbonisation represents a major change in the prevailing wind for investors. No longer a niche consideration, it’s increasingly central to portfolio construction. Under frameworks like the EU Climate Benchmarks[1], investors are being asked to align with pathways that target a 50% immediate carbon reduction and a 7% annual decline thereafter, consistent with IPCC’s 1.5°C scenario.

Does this change in the winds necessitate a change in destination?

In this article, we argue it does not. The core objectives – risk-adjusted returns, diversification and capital preservation – remain unchanged. But decarbonisation does reframe the constraints and tools used to achieve them.

With some skilful adjusting of the sails, we believe investors can adapt and chart a course to their desired destination. But there are some important nuances to consider.

Decarbonisation without derailing objectives

Our modelling of developed equity markets suggests significant decarbonisation is technically feasible with generally small deviations from market-capitalisation-weighted benchmark performance.

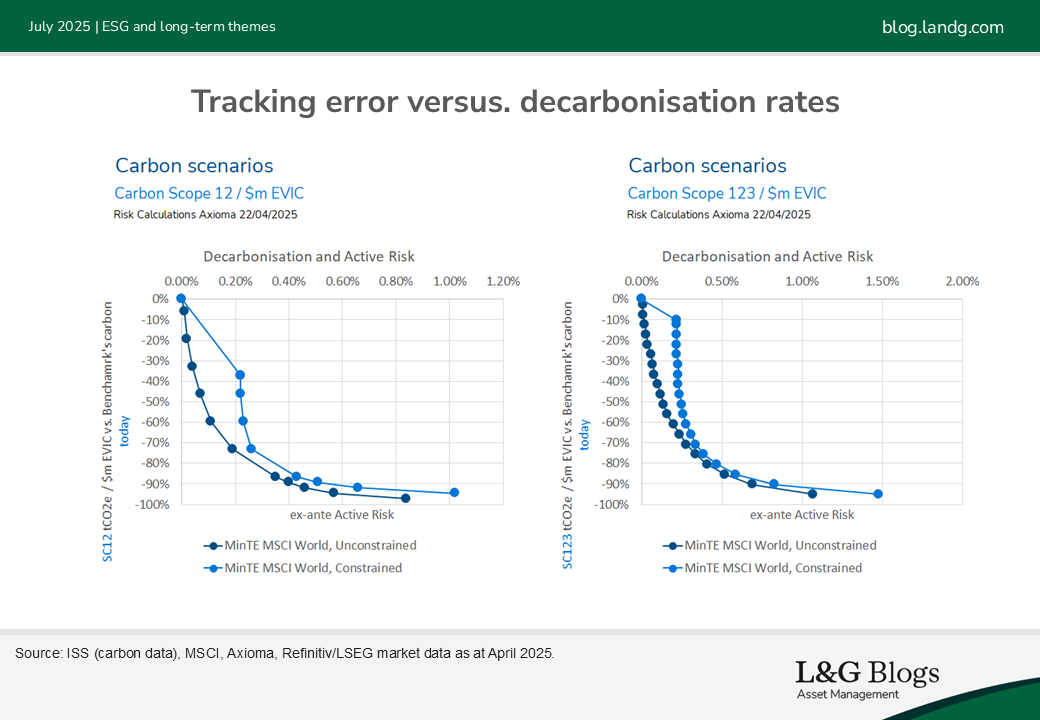

In unconstrained scenarios, where the focus is solely on decarbonisation, portfolios can achieve substantial carbon reductions with an active risk (tracking error, TE) under 100 basis points (bps). Even when Scope 3 emissions are included – often the most complex and opaque – the TE remains below 150bps.

We have studied illustrative market portfolios using today’s market and carbon data, continuing our work from 2022. The findings remain consistent.[2]

We analysed carbon scenarios based on two variations of modelled portfolios:

- Scenarios with minimum TE portfolio, unconstrained: these strategies aim to minimise ex-ante TE while targeting a level of portfolio carbon footprint (WACF[3]) without any exclusions or limits to characteristics such as regions, sectors or securities.

- Scenarios with minimum TE portfolio, constrained by exclusions, limits on regions, sectors and securities, as well an ESG improvement. These strategies include further constraints to explore additional sensitivities.

The same analysis has been run with both Scope 1 and 2, and Scope 1, 2 and 3.[4]

Below we show active risk (TE) for different rates of decarbonisation against the starting universe as at April 2025.[5] In the chart, 'carbon scope 12 / $m EVIC' indicates how many tonnes of CO₂e are emitted per million dollars of Enterprise Value Including Cash (EVIC) over a given period. It is a measure of carbon intensity relative to the issuer’s economic size.

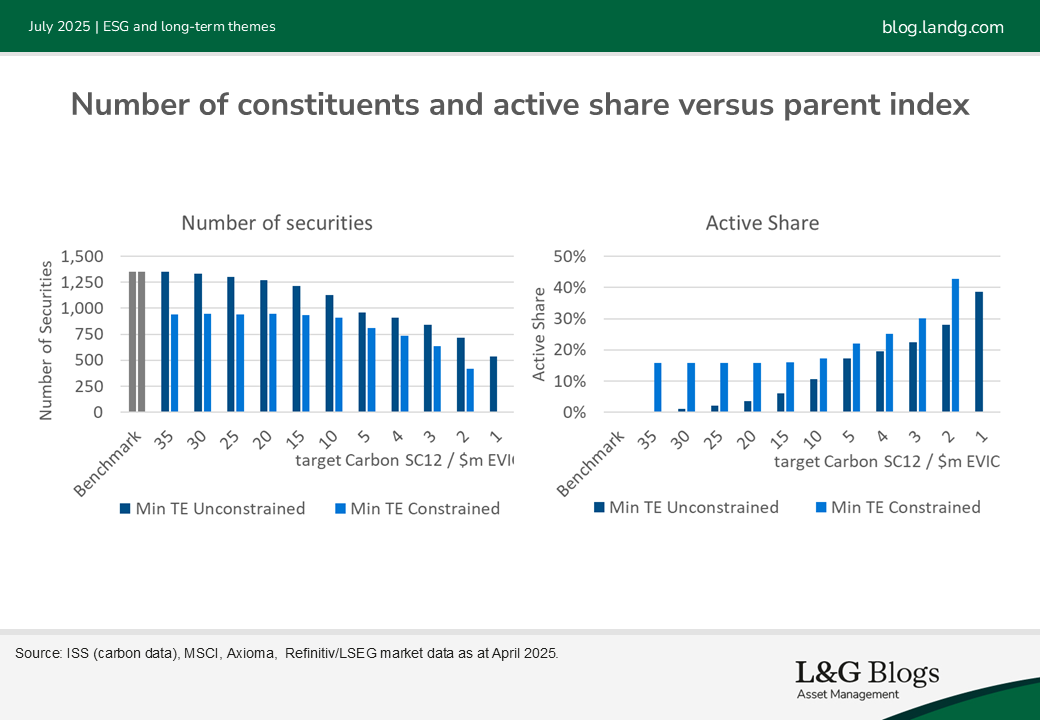

However, the journey is not linear. The final 10% of decarbonisation is challenging, requiring more aggressive exclusions, resulting in higher turnover, fewer securities and increased concentration risk. This trade-off underscores the importance of balancing climate ambition with investment practicality.

Constraints, customisation and ESG integration

When additional constraints are layered – such as regional or sectoral exclusions, or ESG improvements – the investment landscape becomes more complex. When the progressive decarbonisation needs to be met, these constraints can increase TE and limit diversification, potentially impacting performance.

This complexity can open the door to customised solutions.

Strategies may incorporate ESG tilts or other forward-looking metrics like Temperature Alignment (TA) and can offer an alternative way to align with decarbonisation goals, while preserving broad market exposure. However, when additional elements, such as bespoke exclusions, ESG integration, or stewardship requirements, are introduced, maintaining a low active risk profile becomes more challenging.

For instance, many L&G ESG strategies apply a tilt-based approach that enables proportional ESG integration and supports existing stewardship efforts. While these strategies remain close to the underlying universe, they do require a modest active risk budget beyond what a purely carbon-focused strategy would demand.

Sector and regional implications

Decarbonisation naturally shifts portfolio composition. Sectors like financials and technology, typically lower in carbon intensity, are likely to see their weights increase, while energy, materials and utilities see reduced allocations. Within each sector, companies with lower carbon intensities also gain more prominence. Regionally, unconstrained strategies tend to favour Europe and Asia over North America and the UK[6], reflecting differences in carbon intensity.

These shifts are not just tactical – they reflect a strategic reallocation of capital towards business models and regions that are better aligned with policy designed to limit climate change. For long-term investors with a strong preference for decarbonisation, we believe this is not a compromise, but a recalibration aligned with future economic realities.

Other considerations for decarbonisation

Questions often arise from investors on whether decarbonisation strategies remain appropriate and feasible in the near term. One area that warrants close attention is Scope 3 carbon emissions. As reporting becomes more comprehensive, some sectors such as financials and consumer goods may show increased carbon. While some may choose not to directly integrate Scope 3 emissions into their decarbonisation pathways, these emissions can still be considered through alternative means. For example, Scope 3 data is incorporated into our broader L&G ESG score as one of several contributing indicators.

Furthermore, strategies aligned with regulatory frameworks such as the PAB and CTB are required to integrate Scope 3 emissions directly.

Looking ahead, next-generation decarbonisation strategies may attract greater research, potentially becoming more mainstream. These strategies may go beyond portfolio-level decarbonisation to include asset-level considerations, such as the integration of green capital expenditure and taxonomy-aligned activities. There is also growing interest in evaluating the rate of change in emissions in addition to focusing on absolute levels (i.e. TA). As the landscape continues to evolve, sector-specific decarbonisation pathways may also be considered.

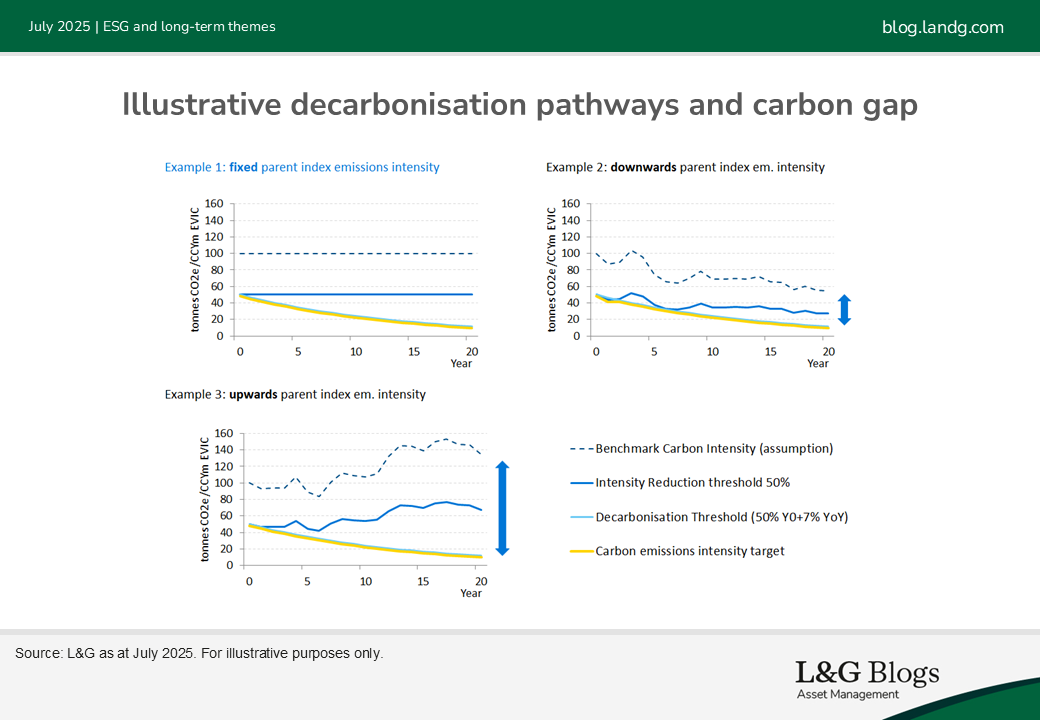

While we have assessed risk profiles based on the current investment universe and carbon data, future developments could lead to different conclusions. For instance, if the carbon intensity of the universe were to increase significantly, maintaining the same decarbonisation pathway would result in a widening carbon gap between the strategy and its benchmark, and vice versa. This would, in turn, increase active risk. Below we show increasing and decreasing carbon for the universe relative to a defined decarbonisation pathway.

Tacking into the wind

Decarbonisation need not negate traditional investment objectives – it redefines the parameters within which they are pursued. For many investors, carbon intensity, regulatory alignment and ESG integration have become prominent components of portfolio design, alongside the traditional dimensions of risk and return.

Through L&G, our clients have exposure to a slice of the global market, and therefore to risks and opportunities that can be financially material to our clients’ investments. Our ‘universal ownership’ approach to investment stewardship means that we believe in using corporate engagement and policy dialogue to drive long-term value creation and shape the future by encouraging more sustainable, long-term practices from companies.

Decarbonisation does not mean investors need to change their goals. With the right tools, data and strategy, we believe investors can pursue net zero while still targeting performance objectives. Sustainability and profitability need not be mutually exclusive.

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. Past performance is not a guide to the future. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. It should be noted that diversification is no guarantee against a loss in a declining market. Whilst L&G has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

[1] EU Paris-Aligned Benchmark (PAB) and Climate Transition Benchmark (CTB)

[2] L&G - Fadi Zaher - Decarbonising index strategies – an overview (2022).

[3] Weighted Average Carbon Footprint – tCO2e /$m EVIC

[4] We note that company-reported Scope 3 data availability continues to be significantly estimated, albeit we have observed some gradual improvement in recent years. The exercise of measuring and reporting on Scope 3 on all indirect emissions upstream and downstream is not free from complexities and varies in coverage and methodology across sectors.

[5] Decarbonisation portfolios are constructed based on a broad market cap universe representative of developed equity markets (MSCI World) with minimisation of active risk optimisation, controlling for regional neutrality, sector deviations within +/-3%, security deviations from universe +/-3% and max 20x. ESG impact at least +5%. Light exclusions of thermal coal (20% revenues and no new coal), controversial weapons manufacturers and perennial UNGC violators with impact approximately 0.50% exposure and 10bps ex-ante TE. Risk Calculations: Axioma.

[6] Based on L&G analysis illustrated above.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.