Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Digital infrastructure: Charting the course in 2025

After proving fairly resilient in 2024, we look at what the remainder of 2025 may have in store for digital infrastructure – including the potential impact of DeepSeek’s* R1 model release.

Generative AI and DeepSeek

Let’s start with January’s most prominent headline: The release of DeepSeek’s R1 model increasing uncertainty around the value of capital expenditure on AI undertaken by Silicon Valley’s tech giants.

DeepSeek’s AI model performed like world-leading US models while using a fraction of the computational resources to build and use it[1]. It was also made freely available to download.

What are the potential implications for digital infrastructure? Well, demand for data centre power and leasing activity comes from a few sources. Cloud services from companies like Microsoft’s Azure, Google Cloud and Amazon’s AWS, the “hyperscalers”, is one – and one where growth alone is expected to bring robust demand[2]. Enterprises needing to house their servers is another. We’ve also seen increasing demand for data centre power driven by the increasing prominence of AI providers.

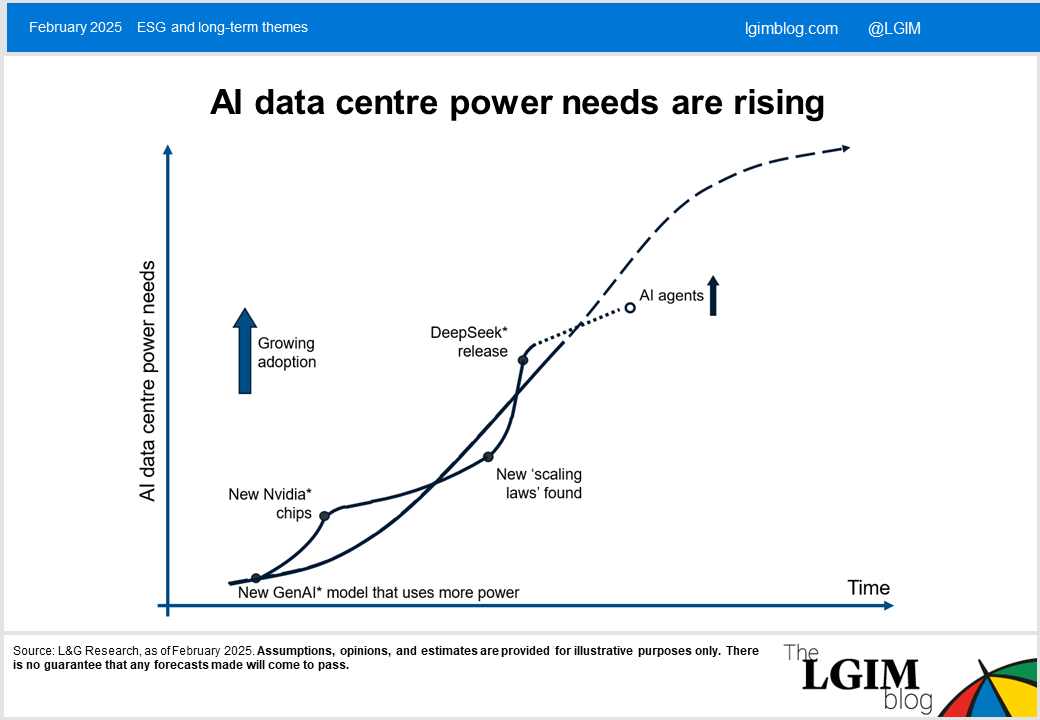

The exponential increases and decreases of AI power needs have been characteristic of its development prior to DeepSeek’s R1 release, both in AI models developed and improvements in AI chips. For example, OpenAI* showed its new o3 model in December 2024 costing exponentially more to improve performance[3]. Nvidia*, meanwhile, previously claimed its new AI chips would reduce cost and energy consumption by ~25×[4]. The cost of using AI models of a given performance has been decreasing exponentially over the last two years of development, with DeepSeek’s advancement being the latest iteration[5].

Hyperscalers and technology companies have known of these exponential swings over the last 2 years, yet have continued to spend significantly on AI. Such sentiment continues: with acknowledging DeepSeek’s innovations on increasing GenAI efficiencies and the surrounding unpredictability, hyperscalers have signalled even greater capex spend through 2025. Such rhetoric has supported a backstop and mild recovery in data centre REIT pricing after its fall following DeepSeek’s release, though uncertainty remains.

AI power needs can potentially be considered as an ‘s-curve’[6], overlayed with frequent demonstrations of exponential increase or decrease. We anticipate future exponentials in the adoption of AI agents (AI models that take decisions and perform tasks), which could need lower-cost reasoning models as enabled by DeepSeek to lower economic barriers while providing reliability3, and the development of next-generation AI chips with greater AI efficiencies, like Nvidia’s Rubin. The overall contribution to data centre demand is uncertain, but its underlying growth, supported by rising adoption, is expected to have meaningful impact.

DeepSeek’s advances may enable technology companies to optimise their AI chips and models beyond what was previously thought. In a bear case, this may reduce short-term leasing activity as tech companies re-evaluate their chip capabilities. However, the open-source nature of DeepSeek, alongside its lower entry barrier, could enable enterprises to use their own servers for AI/DeepSeek workloads, potentially increasing their data centre leasing, albeit with less power per lease.

Even without AI, robust data centre demand growth is expected2. The pace of innovation can bring uncertainties, and markets will determine if this translates to higher or lower risk premia.

Resilience in digital infrastructure through 2025

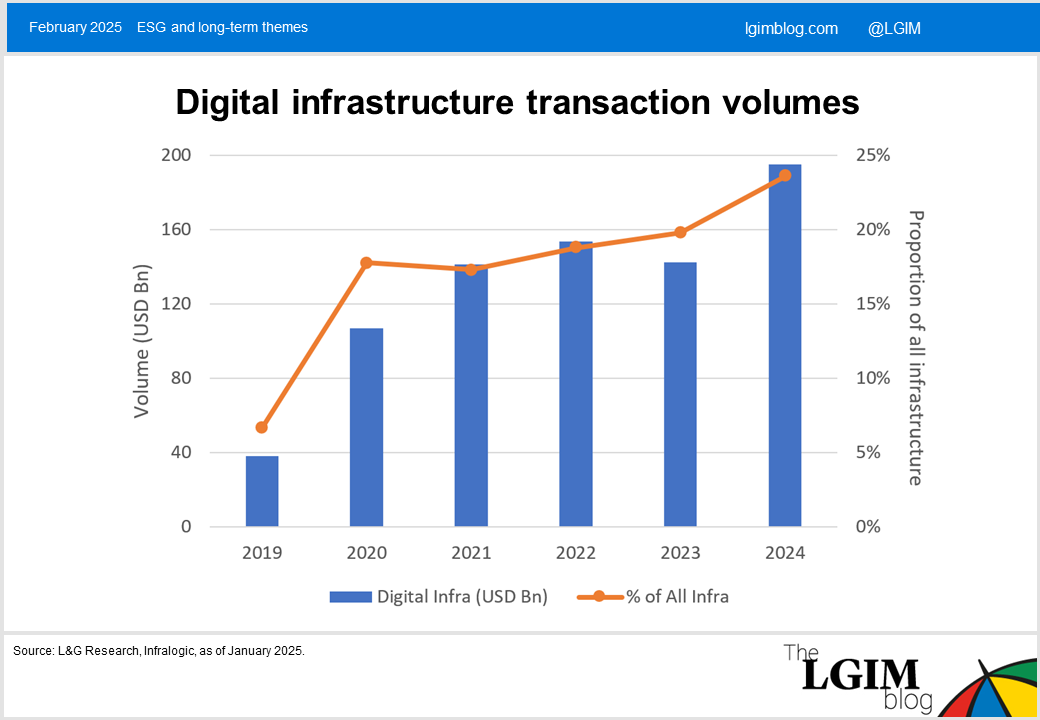

In 2024, digital infrastructure showed resilience through an overall challenging environment[7]. With the forecasted rise in data demands, we anticipate ongoing strength in transaction volumes for 2025, driven primarily by data centre activity.

Mild caution on AI may drive transactions towards markets that align closer with the needs of cloud services or enterprise tenants housing servers. With new developments now reaching multi-billion-dollar capital requirements, we believe private markets are positioned to continue capitalising the buildout.

Deployment for data centres is expected to compensate smaller transaction activity in towers and fibre and maintain resilience for digital infrastructure overall.

A decline in rates could increase European M&A activity in towers, in our view, though deployments might remain limited. We see fibre buildouts continuing, with some regional variation, likely led by incumbents with support of public market financing.

Private markets could see further consolidation or refinancing transactions of smaller fibre companies after the higher-rate environment. We believe there will likely be opportunities for deployment in towers and fibre, though we also estimate the capital requirements to develop these assets will be lower than for data centres.

Data centres see robust leasing activity

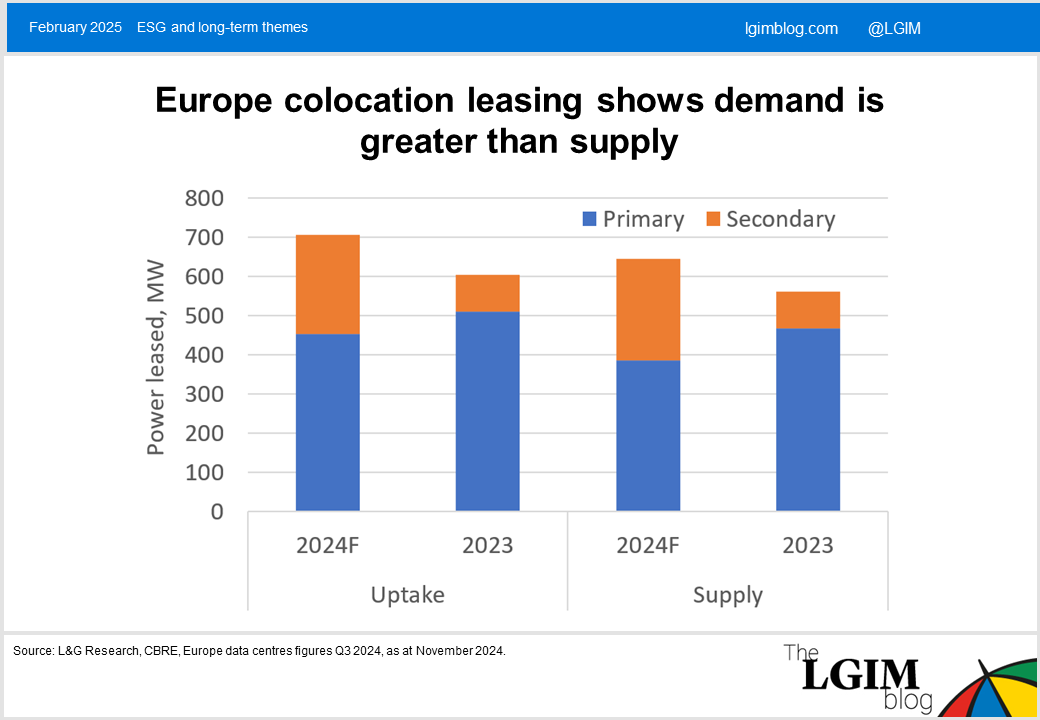

In 2025, we believe data centres will see demand growth, with data and AI sovereignty serving as rising drivers of European demand. Further long-term drivers include the increasing operational power needs for non-AI servers[8] and difficulties in enhancing data centre power efficiency.

We believe demand will remain robust in primary markets. Limited supply, multi-year construction times, and rising construction costs could keep vacancy rates subdued, dampen leasing activity, and drive rental growth. Supply is expected to grow in secondary markets, where its absorption helps to maintain overall leasing levels.

In the US, Trump's policies could see developments start earlier through deregulation, but his approach to immigration may reduce the number of construction workers[9], increasing costs and delaying completion times.

Geopolitical tensions simmer while AI sovereignty gains traction

Chip-related US trade restrictions on China increased through 2024, and Biden announced further regulation before his departure, effectively splitting the world into three tiers[10]. We expect geopolitical tensions to continue simmering in 2025 as the US seeks to streamline data centre construction for national security, further restrict the supply and usage of AI chips and models, and reshore semiconductor manufacturing. A restricted global chip supply due to a geopolitical escalation would have profound implications – and data centre economics would be no exception.

High-quality data suitable for building ever larger GenAI models is becoming constrained: the rate of high-quality global data creation is slower than the rate at which the models are consuming it[11]. In 2025, we expect clearer regulations on European data usage[12] and a rise in AI sovereignty, where nations develop their own models. This could boost investments in European data centres from US companies as they seek to align with regulations. Furthermore, ensuring data privacy and protection alongside enabling data and AI sovereignty could motivate companies to increase repatriating data from hyperscalers to local servers in colocation data centres, driving leasing activity.

Balancing data centres’ power needs with meeting net-zero

Meeting data centre demands while achieving net-zero targets will be a challenge faced by many through 2025. Centralising processing and storage through providing data centre capacity can improve the overall power efficiency of rising demands, but efficient use of resources remains crucial, in our view.

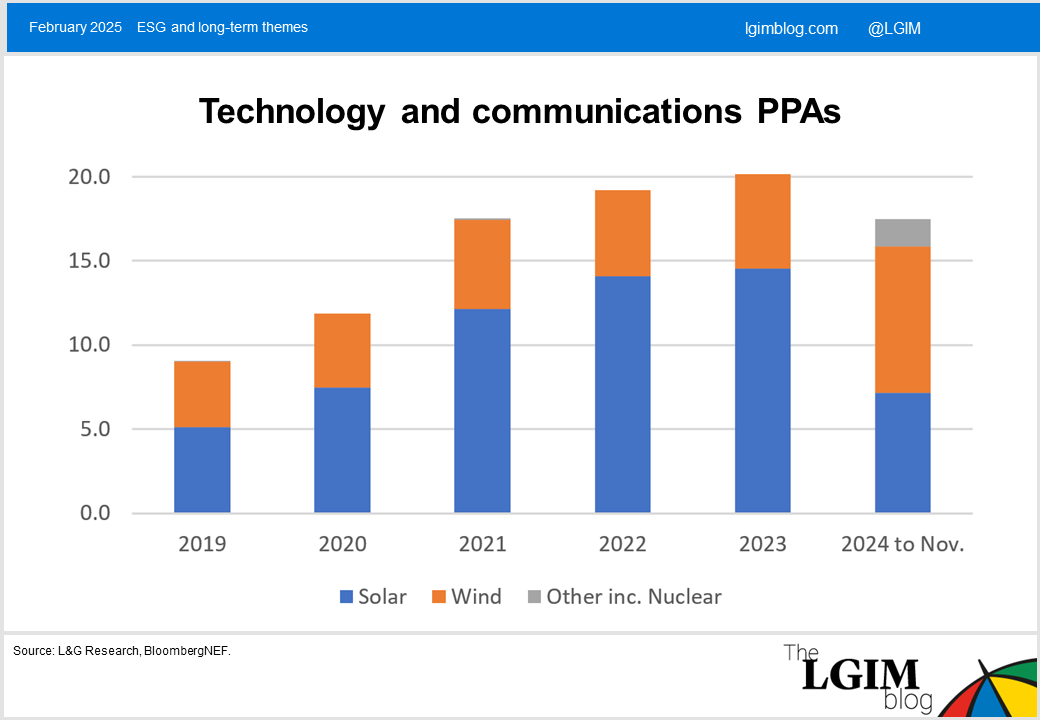

We anticipate growing power purchase agreement (PPA) volumes for renewables through 2025 as hyperscalers aim to meet net-zero commitments. Longer-term, we see nuclear power potentially playing a larger role as data centre operators seek access to a steady source of low-carbon electricity. Small modular reactors could address power challenges and shift investment focus back to primary markets for greater alignment with established drivers.

Charting the course in 2025

The interplay between AI advancements and digital infrastructure will continue to evolve with potential shifts in leasing activity and power needs, though supported by growing AI adoption. Despite these uncertainties, the growth in cloud services, enterprises housing their servers, and the push for digital sovereignty are anticipated to drive sustained demand for data centres. Geopolitical dynamics are likely to influence AI development and data centre investments as nations strive to secure their technological and economic interests.

In the wider context of real assets, data centres benefit from a multiyear asset creation cycle amid an increasingly stretched supply backdrop that creates growing value for asset owners. Their compelling long-term characteristics, alongside their exposure to AI innovation, will likely continue to attract private capital through 2025.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an LGIM portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] DeepSeek-R1: Incentivizing Reasoning Capability in LLMs via Reinforcement Learning, DeepSeek, January 2025

[2] Breaking barriers to Data Center Growth, BCG, January 2025

[3] R1-Zero and R1 Results and Analysis, Mike Knoop, ARC Prize, January 2025

[4] NVIDIA Blackwell Platform Arrives to Power a New Era of Computing, NVIDIA, January 2025

[5] DeepSeek Debates, SemiAnalysis, January 2025

[6] RAND, AI’s Power Requirements Under Exponential Growth, January 2025

[7] Infralogic data as of January 2025.

[8] 2024 United States Data Center Energy Usage Report, Berkeley Lab, December 2024

[9] Trump immigration proposals could make construction shortage worse, Axios, January 2025

[10] Biden unveils last round of AI chip curbs aimed at China, Russia, CNN Business, January 2025

[11] Will we run out of data? Limits of LLM scaling based on human-generated data, EpochAI, June 2024

[12] Europe needs regulatory certainty on AI, euneedsai.com, September 2024

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.