Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Deglobalisation 2.0: Real estate

Real estate has shown it can perform even amid higher inflation and rising rates, providing growth is strong. How does a ‘deglobalising’ world change the picture?

Generally speaking, we believe real estate can still perform in an environment of higher inflation and rising interest rates if economic growth is sufficient to boost returns via eroding voids and growing rental income. Tariffs may introduce significant macro challenges, but strategic investments can still yield positive outcomes. Real estate opportunity is likely to be highly localised, but not necessarily absent.

Firstly, some context. In the US, backward looking economic data at the end of 2024 was generally positive and supported the PREA Consensus[1] forecast for a 6.6% total return for 2025 with positive 1.7% capital appreciation. Prospects for 2025 were based on assumptions for ongoing positive US macroeconomic and financial markets paths.

In the UK, consensus forecasts[2] suggested all property returns of 8.0% p.a. over the 2025-2029 horizon, with capital appreciation of 3.0% p.a.. With rents expected to grow 2.6% p.a., this implies, assuming depreciation in excess of -1% p.a., a reasonably positive effect from yield compression.

Recovery cycles are usually dominated by more aggressive yield tightening than this, so being cautious on this yield driver makes sense at a time of geopolitical uncertainty. However, the potential for stubborn or even higher market interest rates reduces further the certainty around this performance lever being pulled.

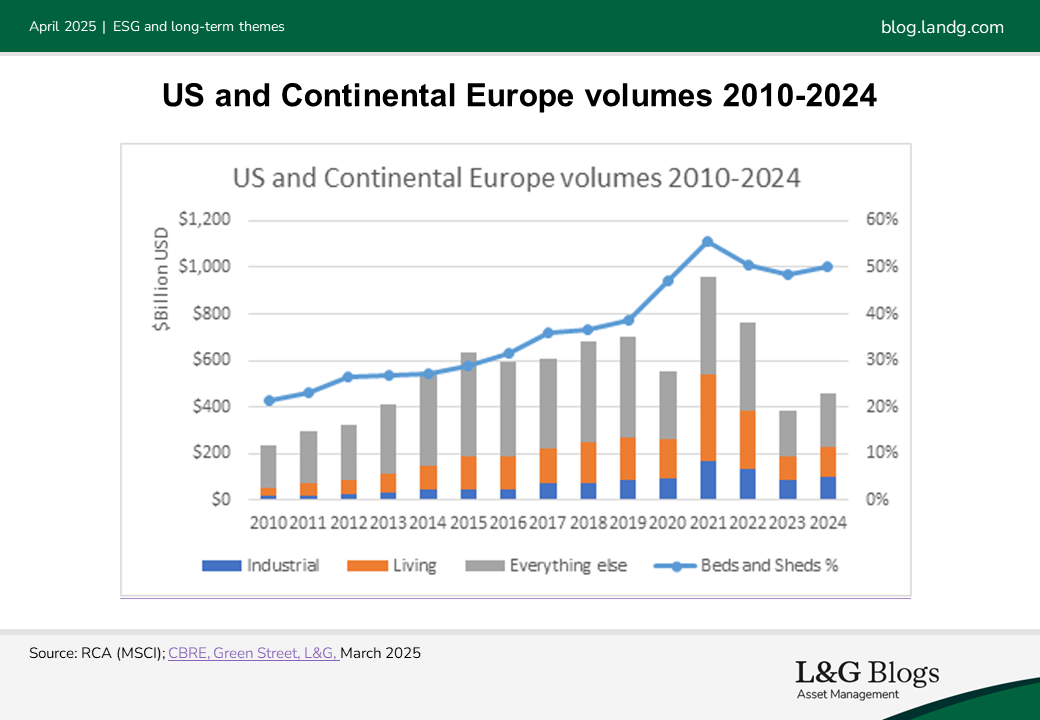

The global real estate market has been dominated by a strong narrative around ‘beds and sheds.’ This means living-related real estate across various strategies, and buildings supporting distribution and manufacturing activity.

There’s a good reason this has been front and centre, with global megatrends supportive for long-term performance in these parts of the market above all others. Strong expectations, however, naturally result in lower yields. Although we are comfortable with current yield levels, rate uncertainty increases the reliance on growth to deliver performance.

We have observed a narrowing gap between expected returns for living and industrial sectors, which we might term ‘growth sectors,’ and other parts of the market such as within retail, leisure, hospitality, and certain office markets. These sectors have experienced significant capital value correction, and their higher yields require less growth to perform. We can call these ‘income sectors.’

'Beds and sheds' have dominated investment volumes

At a macro level, our view is that a lower growth/stubborn rates scenario might make some income sectors appear more attractive, given there may be perceived insulation from higher yields. But this is more likely to be part of a nuanced response, in our view, which would still support parts of the living and industrial world – as well as caution elsewhere.

For instance, we believe higher rates are likely to delay the owner-occupier housing recovery and prolong mortgage affordability challenges. This should be good for residential rental demand. Within industrial, although port traffic is likely to be affected adversely, tariffs may result in more onshoring of production alongside a push for more resilient domestic supply chains, and therefore net new industrial demand.

Performance expectations for higher-yielding assets can also quickly unwind when growing void or depreciation risks are factored in. Asset and locational underwriting will be even more critical, in our view.

More generally, we believe sectors and locations that are now enjoying supply-demand balance with vacancy rates in line with historical averages can endure slower national economic growth and higher inflation with minor impact. On the other hand, markets now digesting excess supply of new space will require more time to achieve equilibrium should growth slow. This encourages continued caution on many office markets. Longer-term, construction cost inflation and macro uncertainty can restrict new development activity, further constricting supply and supporting rental growth prospects in markets without excess space.

Consequently, we see the pace of investment transactions potentially slowing (relative to what they would otherwise have been) as some investors take a more cautious view of US policies; or at least wait to see how they settle. Such caution could spell a prolonged acquisition opportunity for tactical investors.

We expect the main impact will be making investment more selective and forensically underwritten within both main styles: whether ensuring growth projections are justifiable or that yields offer sufficient compensation for changing risks amid another phase of geopolitical uncertainty.

Past performance is not a guide to the future.

[1] Pension Real Estate Association, November 2024

[2] PMA, 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.