Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Deglobalisation 2.0: Private equity and private credit

In the next instalment of our series on deglobalisation, we look at whether 2025’s macro environment is still conducive to a recovery in the private equity space and still supportive of potential outperformance in private credit. If you missed our first article on how deglobalisation is impacting today’s macro environment, you can find it here.

Are we still on course for a recovery?

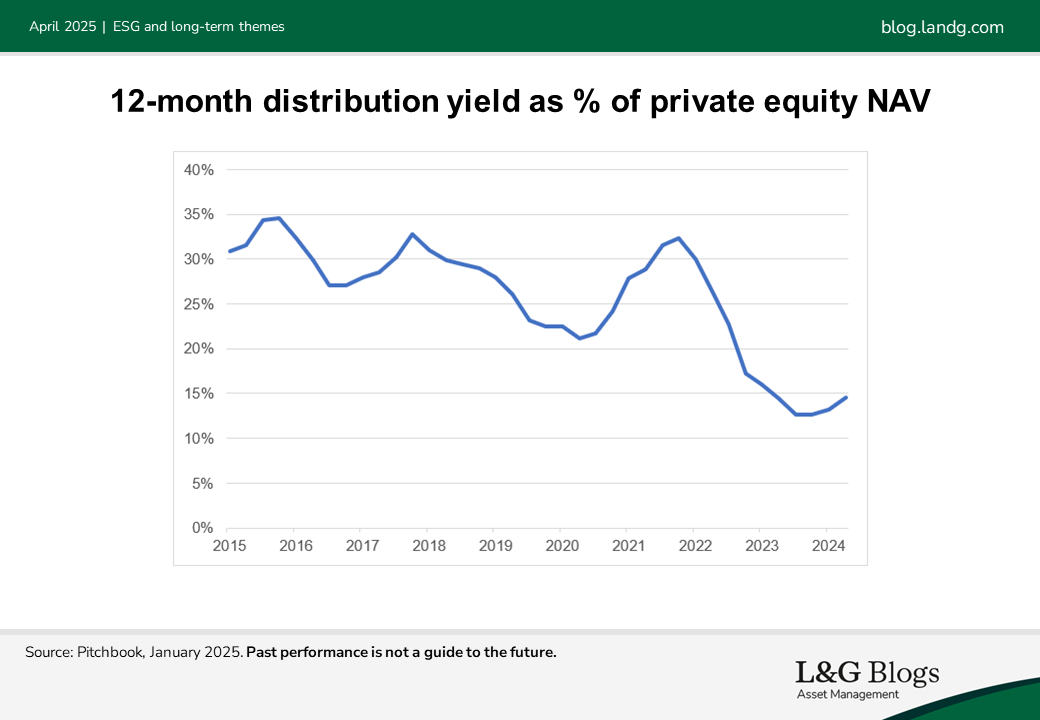

Last year, the private equity industry began recovering from the tough market conditions in 2022/23 and investors were highly optimistic about 2025. The main challenge had been exiting the backlog of portfolio companies profitably so capital can be returned to investors who can then recycle it into new commitments or meet cashflow needs.

The optimism is now tempered by trade war and stagflation risks. Near-term GDP outlook for the US has deteriorated relative to Europe. Expectations for Fed rate cuts this year have also been dialled back due to inflation concerns driven by tariffs and immigration policies. A more gradual recovery in transactional activity than the market expected at the start of the year is therefore likely, in our view.

Nevertheless, corporates and private equity managers are cash-rich – managers alone currently have $2tn dry powder[1]. As such we expect capital to continue being deployed. PE activity could pick up in H2 2025 once the market has adjusted to the new environment and we get more clarity on the proposed deregulation policies.

In our view, deal activity is likely to concentrate on high-quality companies able to ride out the storm – those with resilient cashflows, good pricing power, needs-based demand etc.

We believe beneficiaries of President Trump’s policies, such as domestic manufacturing or European defence, are also likely to be attractive. The current environment re-emphasises the importance of operational improvement and value creation versus financial engineering.

The venture capital (VC) sector has experienced a large fall in investment activity and fundraising since 2022 with AI-related sectors one of a few bright spots. The new administration’s emphasis on deregulation and AI investments should support its recovery. However, the US government’s decision to reduce funding for healthcare research and pull back from the Inflation Reduction Act may be negative for biotech and cleantech firms, in our view. Against this backdrop – and combined with restrictive immigration policies – start-ups may be more drawn to the relative stability and access to global talent offered by innovation hubs in Europe and Asia, which could boost valuations of VC companies in these geographies.

Private credit: monitor impact on borrower performance

Private credit had been enjoying elevated returns since 2022 when central banks raised interest rates. This could go on for a little longer if rates remain elevated. US and UK credit spreads have been creeping wider recently and we think there is scope for further widening given the macro uncertainty and tight valuations. Demand/supply could dampen this – we expect demand for private credit to remain strong, but issuance volumes could be affected by higher volatility and weaker than expected M&A activity.

Price inflation and supply chain disruption will, however, weigh on credit quality. Previously, businesses largely passed Covid-related price increases to consumers which generated solid revenue growth. Our view is that the scope to pass through price rises driven by the Trump administration’s policies will be limited for most sectors as the cost-of-living crisis lingers and economic growth is softening. This implies a drag on margins and thus debt serviceability. Stress-testing borrowers against a stagflation scenario will therefore be an important part of underwriting and ongoing monitoring, in our view.

The investment-grade (IG) private credit market includes larger, more global firms that are likely to be more exposed to a trade war. However, we believe the credit quality and structural protections of these assets should immunise investors from losses. Indeed, market activity suggests that this segment remains robust with a busy pipeline. The sub-IG private credit market tends to be more domestically focused. However, sub-IG borrowers are more vulnerable to rising yields and macro weakness. We see upside risk for default rates and expect managers to proactively monitor operational performance for signs of stress and engage with borrowers.

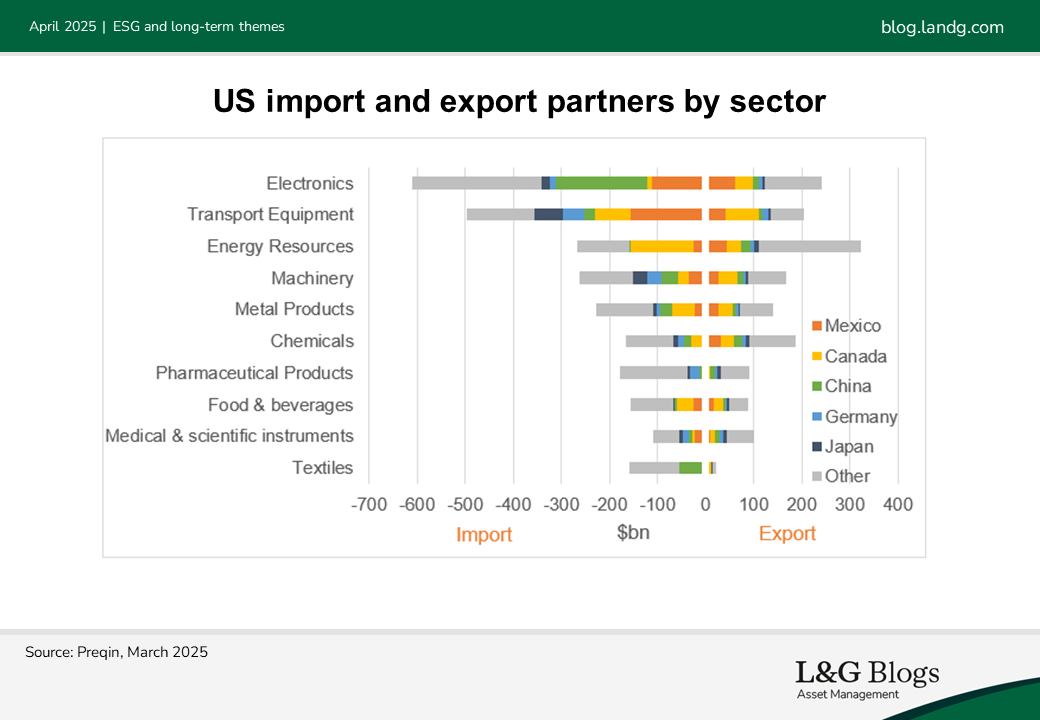

[1] Source: Preqin, March 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.