Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Carbon market unification: A post-Brexit reconciliation

Unification of EU and UK carbon markets could offer economic benefits and increased investment in clean technologies, but it could also lead to higher power prices for industrial users.

In May 2025, the European Commission and the UK government announced their joint commitment to establish a link between their respective emissions trading systems (ETS), both of which function as cap-and-trade systems. This integration means that carbon emissions permits issued under either the EU ETS or the UK ETS will be mutually recognised for compliance in both systems.

This move could be significant for sectors mandated to use carbon permits, such as electricity generation and energy-intensive industries.

Benefits

One of the most-cited benefits of a harmonised carbon market for the UK is the reduction in costs for exporters by avoiding the EU’s Carbon Border Adjustment Mechanism (CBAM). The CBAM, set to come into effect in 2026, is essentially a tax that adjusts the price of certain imports to account for CO2 emissions embedded in their production. By ensuring importers pay the same carbon price as domestic producers, the CBAM aims for equal treatment for products made in the EU and imports with lower emissions standards. Initially, it will apply to importers of cement, steel, aluminium, fertilisers, and electricity due to the high production emissions and potential for carbon leakage.

Exemption from the EU's CBAM is estimated to potentially save UK exporters up to £100 million in 2030 in carbon border taxes based on June 2024 pricing[1], thus aiding UK export competitiveness, as well as reducing the administrative burden of compliance with CBAM. Despite the explicit cost savings, this is somewhat negated by the higher cost of carbon emission from the linking of the two schemes, which reduces the positive impact of the exemption. (See below.)

Beyond cost savings, linking the two ETSs creates a larger, more liquid market, which could reduce volatility and improve price stability, particularly for the UK, whose market is roughly a tenth the size of the EU’s. Fungible emissions permits means that companies have more flexibility to buy and sell carbon allowances. The integration promises to attract more investment in clean technologies and renewable energy projects, driving innovation and supporting the transition to a low-carbon economy.

Drawbacks

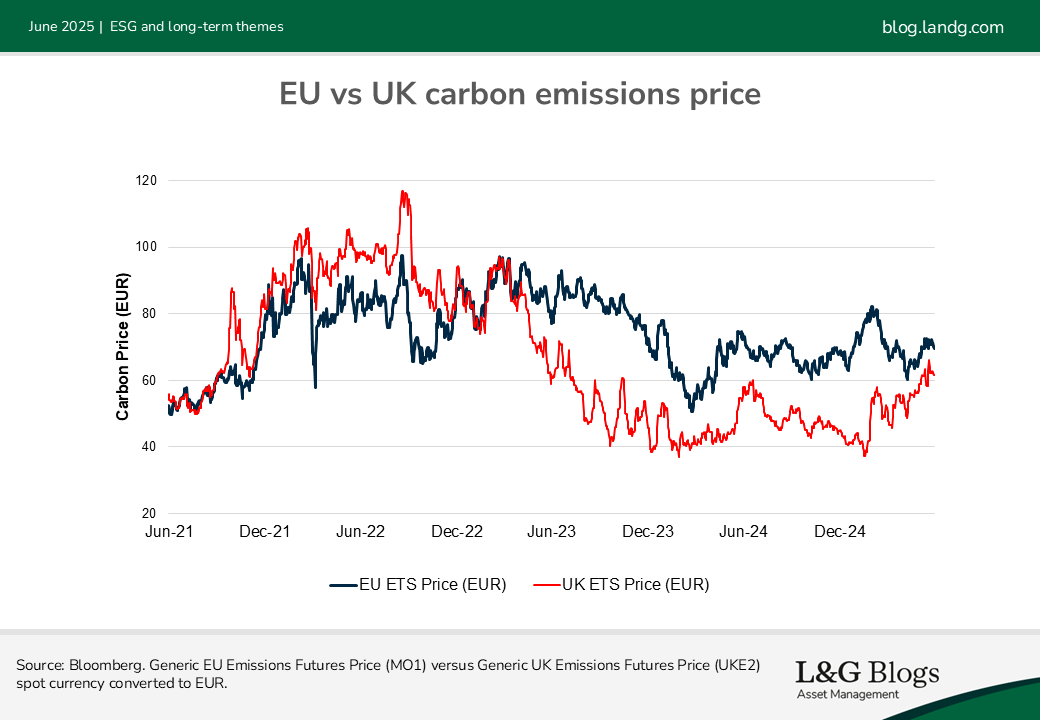

Linking with the EU ETS is expected to result in higher carbon prices in the short term, as the EU market tends to have higher prices than the UK. As of the end of May 2025, UK carbon emissions prices were trading at a discount of approximately €8 per ton compared with European prices.

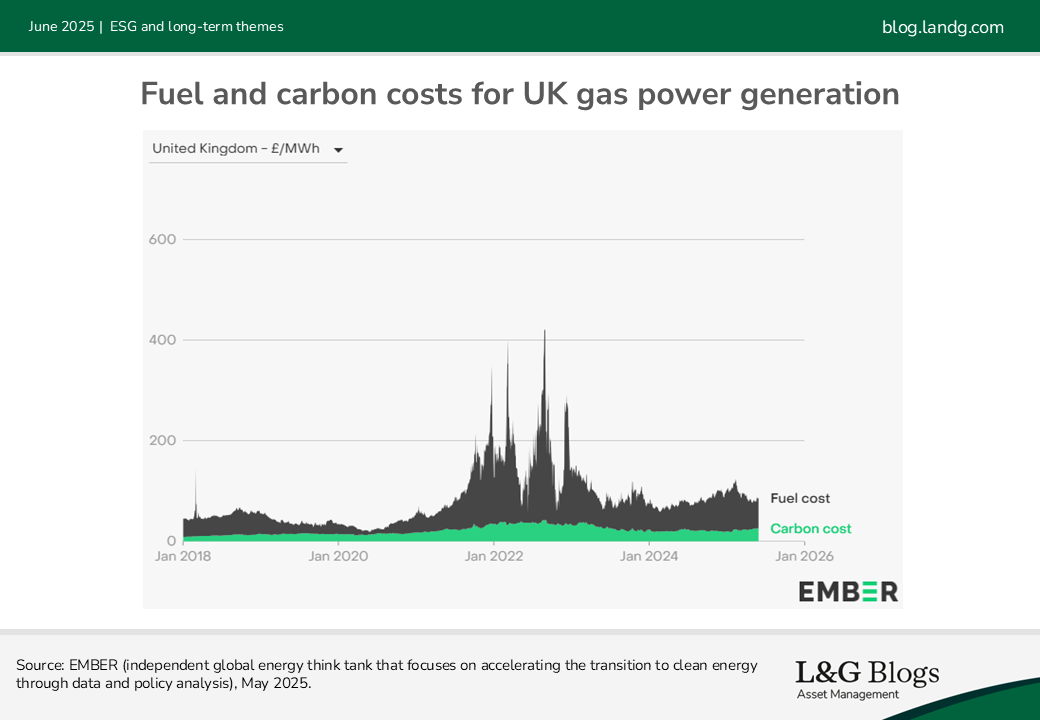

Carbon pricing contributes significantly to UK power prices, making up around 30% of the total cost of gas power generation as of 29 May 2025. Hence, power generators may pass on the increased costs of carbon allowances to consumers, resulting in higher electricity bills. The main impact is likely to be on energy-intensive industries such as steel, cement and aluminium, which are major industrial users of electricity, or those that directly consume gas or coal. In contrast, residential consumers are likely to experience a smaller impact on their electricity bills due to the diverse components included in their pricing structure, such as network charges and supplier margins.

Summary

The unification of the EU and UK carbon markets has the potential to provide significant benefits, including cost reductions for UK exporters, economic efficiency, and increased investment in clean technologies.

However, it also poses challenges such as potential increases in power prices for industrial users. Balancing these factors will be crucial for maximising the benefits while mitigating the drawbacks.

We believe that not decarbonising brings with it direct regulatory costs for firms. Therefore, we continue to encourage the companies we invest in to address their emissions profile and plan for the transition. This proactive approach not only helps mitigate regulatory risks, but also supports the broader goal of transitioning to a low-carbon economy.

[1] Source: Frontier Economics, Linking UK and EU carbon markets, August 2024

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.