Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Capital allocation in Housing Associations

As well as their core objective of providing affordable housing, Housing Associations (HAs) must increasingly allocate capital to building safety and net-zero commitments.

As a large debt investor in the UK HA space, it has been interesting to observe recent developments concerning capital allocation. What is evident is HAs all have the same social purpose: providing affordable and social housing. What is more difficult is monitoring the different strategies adopted to fulfil this purpose.

There is not enough money to go round to fulfil all aspects of their social requirements in the not-for-profit sector, even with new and innovative delivery models. The future spending budgets of HAs in the UK revolve primarily around building safety, decarbonisation/ energy performance certificate (EPC) spending and the need to provide new affordable homes.

But they can’t do it all. Clarion, the largest HA in the UK, has already stated it will be building 1,800 fewer properties over the next five years as a result of the building safety crisis. Specifically in London, the largest HAs have estimated they need to spend £3.6 billion on post-Grenfell repairs in the next 14 years, which is the equivalent of roughly 70,000 new homes.

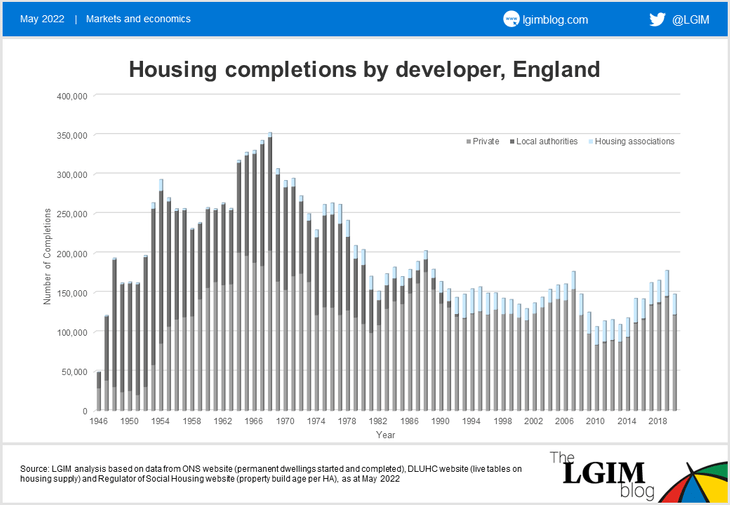

Housing completions continue to massively lag the government target of 300,000 per year. In addition, research commissioned by the National Housing Federation and Crisis identified a need for 145,000 new affordable homes each year to 2031. The chart below shows we are not even close.

When coupling this undersupply with spending requirements around EPCs, as well as the building safety costs outlined above, it is clear that HAs face a huge strain on future budgets and have a decision to make around capital allocation.

So how are we looking at this?

Management attitudes to this problem vary considerably. Some are focusing entirely on remediation and EPC costs of existing stock. Some are recognising the need to build new homes, but only in the context of their current balance-sheet capacity. Others are seeing their social need to provide new affordable homes as the overriding factor in their business model.

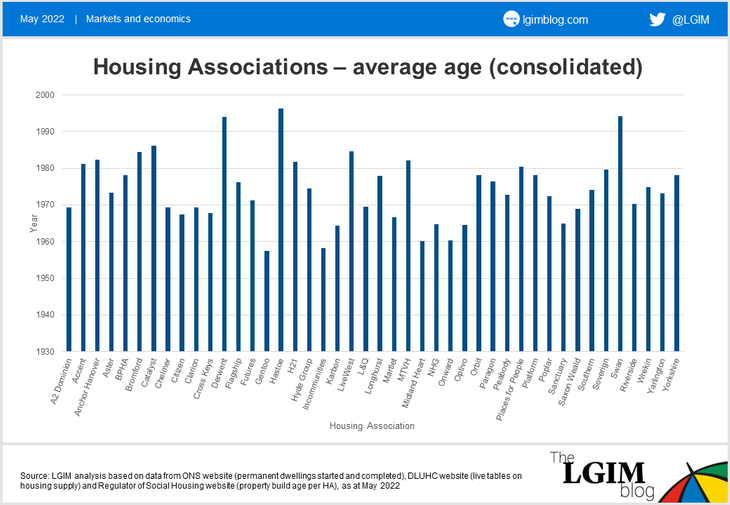

From an investment point of view, we need to understand how realistic future budgeting is, and the starting point for this is existing housing stock. Using data provided by the Regulator of Social Housing we have put together a chart outlining the average age of the housing stock owned by each Housing Association under our public coverage:

With the benefit of this data, we are engaging with each provider with the understanding that older properties require much higher remediation spend around both EPC and building safety. With this in mind, we can then assess how realistic each issuer is being by framing budgets against the current age and quality of their housing stock. Do they match? And more pertinently, if they don’t, why not?

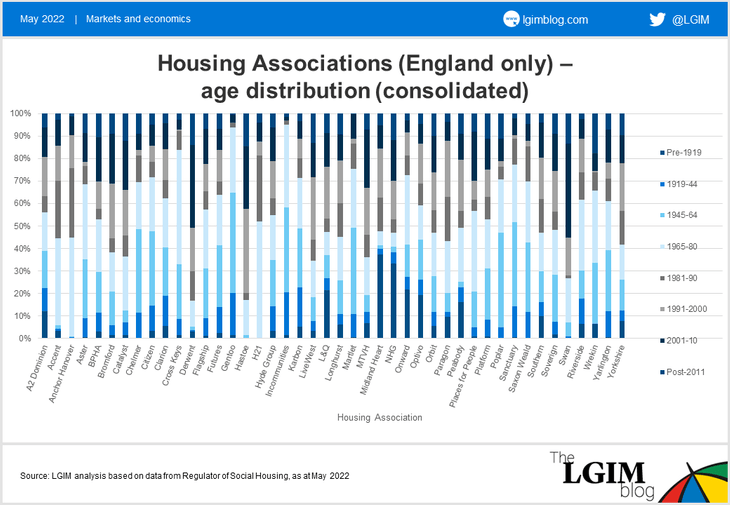

We are sending engagement letters to all HAs under our coverage requesting disclosure on budgeting and thinking around average property age – which we believe to be a key driver on ongoing credit quality in the sector. We already have some data on this, but it is our aim to obtain full disclosure from each HA to obtain a detailed correlation with stock age. The average age of housing stock can be matched in the same way from the following chart:

It is clear from the data provided that many HAs own very old properties built pre-1919. Is it realistic to try to get these to EPC acceptability? This then begs the question of how to match the overriding shortfall in UK social requirements around the government’s push for carbon neutrality by 2050. Similarly, when looking at properties of intermediate age, what is the true cost of building safety here? Are any sacrifices being made in terms of thoroughness and quality?

Rising rates

In a rising interest-rate environment this data also give us an inside track on balance-sheet risk. Borrowing costs are increasing given recent rate and spread volatility; we believe any credit downgrades to BBB (from what is now an A rated sector) would lead to unsustainable capital structures in many cases. There are rising risks in the sector and the exercise we are undertaking should indicate a vital way of getting to the bottom of how they are being addressed.

HA debt used to be seen as a safe haven. It isn’t any more. While it remains a fundamentally attractive, nationally important, defensive sector that will no doubt continue to attract different forms of institutional capital, in our view, how boards and management teams deal with the increasing pressures on limited capital will be critical to future success.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.