Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Branching out: The interesting case for forests in portfolios

Forestry assets have long been valued as essential national reserves. In Britain, usage laws can be traced to the 13th century Magna Carta and the Charter of the Forest, which established citizens’ rights to access Royal Forests. Today, forests are prized not only for their historical role but also for their ability to help diversify portfolios and potentially support nature and climate if managed sustainably.

Diversification

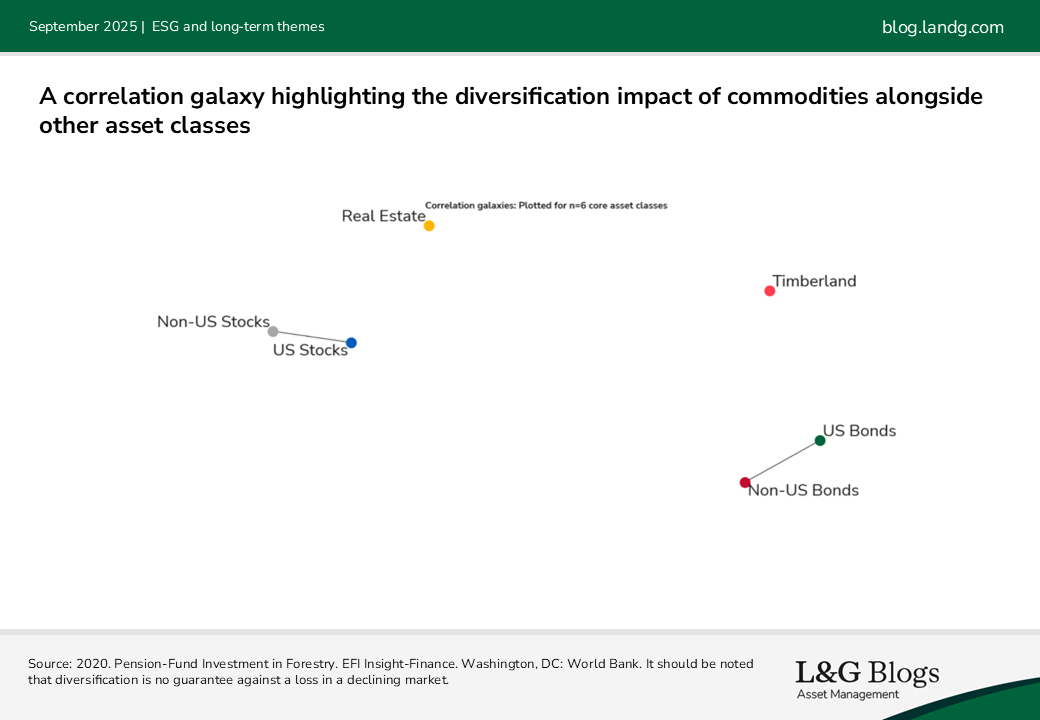

Investment strategies increasingly value forestry assets for portfolio diversification*. Research by Gao and Nardari suggests that adding commodities can enhance risk-adjusted returns. Within the forestry asset class, there is significant diversification too as elasticity of supply depends on product type—biomass trees can be harvested after just 10 years, whereas lumber requires at least 40 years of growth.

Valuing forests

Forests offer the potential for diverse return streams*, generating income from harvested wood and capital appreciation from the underlying land. The versatility of forest outputs include:

- Paper products

- Packaging

- Lumber

- Biomass

- Carbon credits from afforestation

- Bioethanol from manufacturing waste

Timber’s end use shapes its cyclicality—biomass for energy has stable demand, while lumber’s value is tied to the property market. During low demand, harvesting slows, preserving future yields. As trees mature their versatility increases, raising prices. Forestry companies may also improve long-term returns by withholding supply when prices are low.

Market valuation

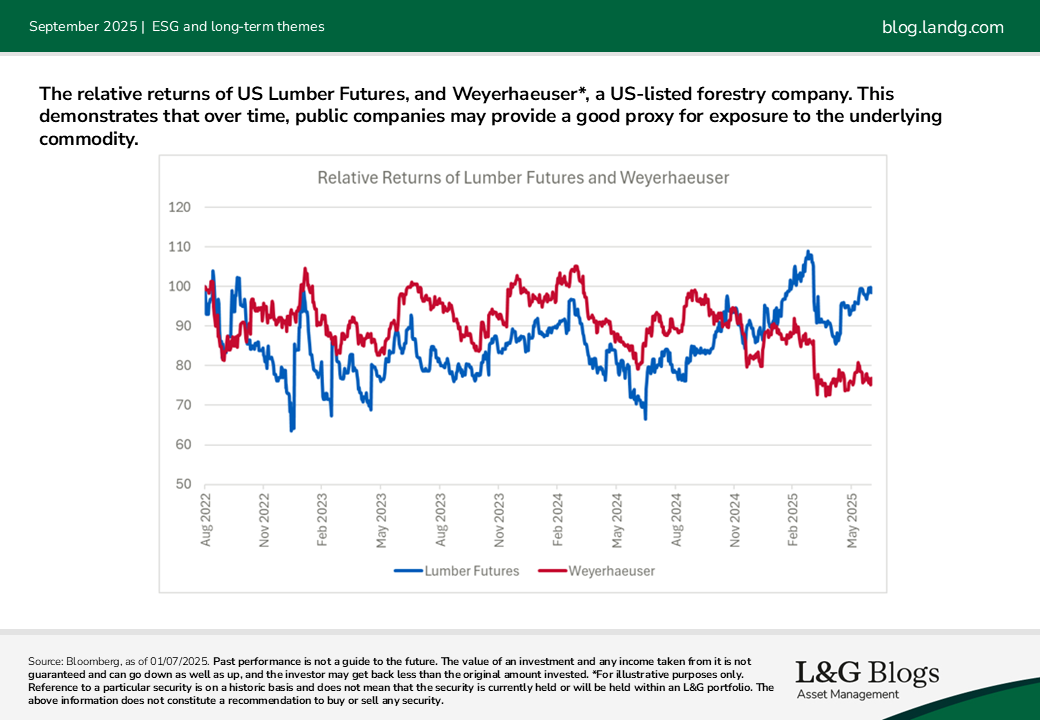

Gaining exposure to forestry assets can be complex; many timber companies are integrated, also owning mills or packaging businesses. Mill earnings are more cyclical than forest values, so market prices tend to fluctuate more with broader economic cycles^.

Publicly listed forestry assets often trade at a discount to NAV, potentially appealing to long-term investors who can see past short-term volatility. This discount is driven by three factors:

· The opportunity cost of holding forestry assets versus typically faster-growing investments like technology companies

· Listed forestry assets aim to offer enhanced liquidity versus private asset equivalents, which can be seen as a potential benefit, but their prices are also much more volatile, and investors may then require a discount for accepting that additional short-term risk

· Forestry is a niche sector with few listed firms, which can lead to lower valuations due to gaps in investors' familiarity with them

Commitment to sustainability

In 2021, our then CEO signed the COP26 Commitment on Eliminating Agricultural Commodity Driven Deforestation from Investment Portfolios. This commitment emphasises active ownership and ongoing stewardship, aiming for portfolios free from forest-risk agricultural commodity-driven deforestation activities. Furthermore, we updated our Deforestation Policy in September 2024 to reflect best practice guidance and align with the latest industry standards on deforestation.

L&G's Active Ownership report highlights our commitment to sustainable investing. In 2024, our Investment Stewardship team engaged with 3,447 companies, addressing key issues such as climate change, biodiversity, and governance. We voted on 142,000 resolutions worldwide, reflecting our dedication to responsible investment.

In our view, sustainably managed forestry assets present an interesting case for potential inclusion in multi-asset portfolios by offering both diversified returns and alignment with nature and deforestation targets.

* It should be noted that diversification is no guarantee against a loss in a declining market.

^ Past performance is not a guide to the future.

Whilst L&G has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.