Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Better disclosure needed

Scope 3 data quality still creates challenges for investors.

Measuring and managing corporates’ Scope 3 emissions will be an important part of the energy transition. However, our analysis shows that available Scope 3 data is not currently a reliable metric due to missing and incomplete company disclosure. Given these data quality issues, we believe investors should prioritise improving Scope 3 disclosure within their portfolio. If investors wish to integrate Scope 3 data into investment decisions, we suggest that they carefully consider potential inaccuracies and estimation bias.

Scope 3 in the spotlight, but data issues persist

As a quick refresher, Scope 3 emissions refer to all greenhouse gases produced by the upstream or downstream activities within an organisation’s value chain. Scope 3 emissions can be broken down into 15 different categories, defined by the GHG Protocol, ranging from upstream purchased goods and services, to end-of-life treatment of sold products.

Companies do not directly control these emissions, but they can manage them downwards in various ways – such as engaging with suppliers, adjusting product specifications, and developing end-of-life solutions. Because Scope 3 emissions represent over 80% of total emissions for a median MSCI ACWI company[1], reducing these emissions will be an incredibly important piece of the energy transition puzzle.

However, investors still face several challenges when considering company-level Scope 3 emissions. Our analysis indicates that Scope 3 emission data is plagued by two key data quality issues, which will be the focus of the blog: lack of disclosure and incomplete coverage of relevant categories.

Additionally, the IIGCC explains how Scope 3’s inherent double-counting across entities creates other serious challenges which investors should think through. Therefore, we believe investors must be very cautious when using Scope 3 data for investment decisions. For now, investors may benefit more by focussing on improving Scope 3 disclosure within their portfolio – as called out in the ISSB S2 standard.

Key data issue #1: Most companies do not disclose Scope 3, forcing investors to rely on unreliable third-party estimates

Due to the inherent challenges with measuring and managing these emissions, many reporting frameworks have historically made Scope 3 disclosure optional[2]. While several jurisdictions are now phasing in Scope 3 disclosure requirements[3], many companies still only disclose on Scope 1 and 2. As a result, investors must often rely on third-party estimates to fill in Scope 3 data gaps.

We can see this phenomenon reflected clearly in the MSCI ACWI. For 34% of the index’s market value, the issuing company did not disclose Scope 3 in their CDP or annual reports. When compared with Scopes 1 and 2, we see far less prevalence of third-party estimates – constituting only 4% of the index value.

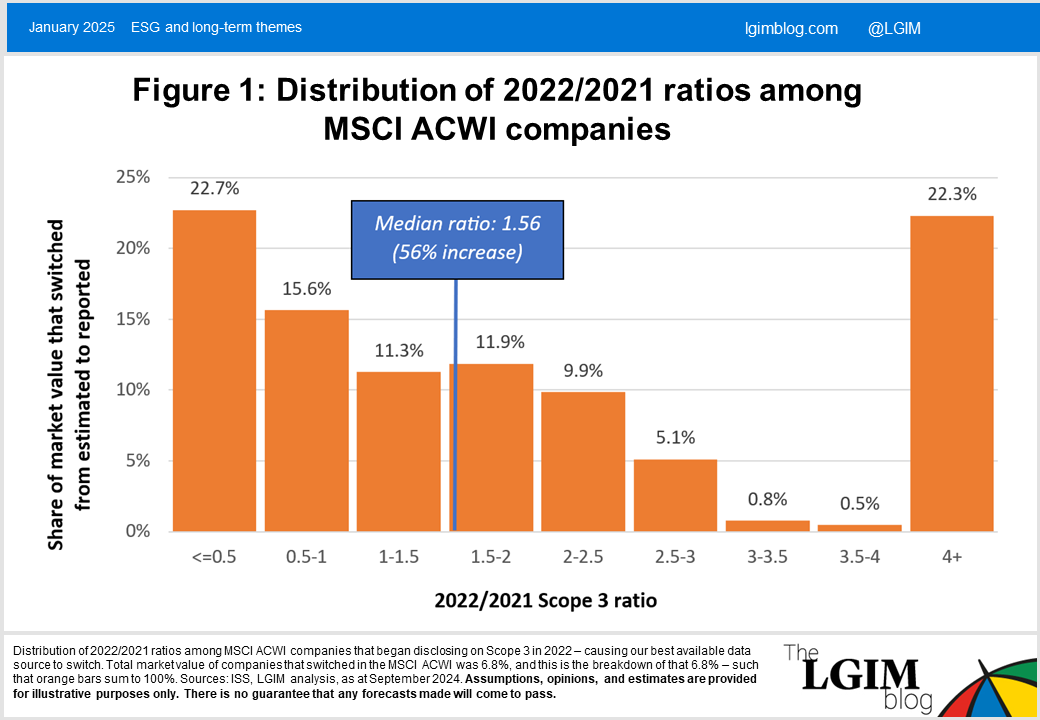

This is problematic as Scope 3 estimates are highly uncertain, and they appear to be systematically underestimating real-world emissions. Based on our analysis of companies who did not disclose Scope 3 in 2021 and then began doing so in 2022 (as shown in Figure 2 below), we see a median increase in Scope 3 emissions of 56%. Such an increase is significantly larger than what could typically be attributed to usual year-to-year changes (usually between 0-10%), indicating the change is most likely due to flaws in the estimation methodology.

Key data issue #2: Companies exclude material categories from Scope 3 disclosure

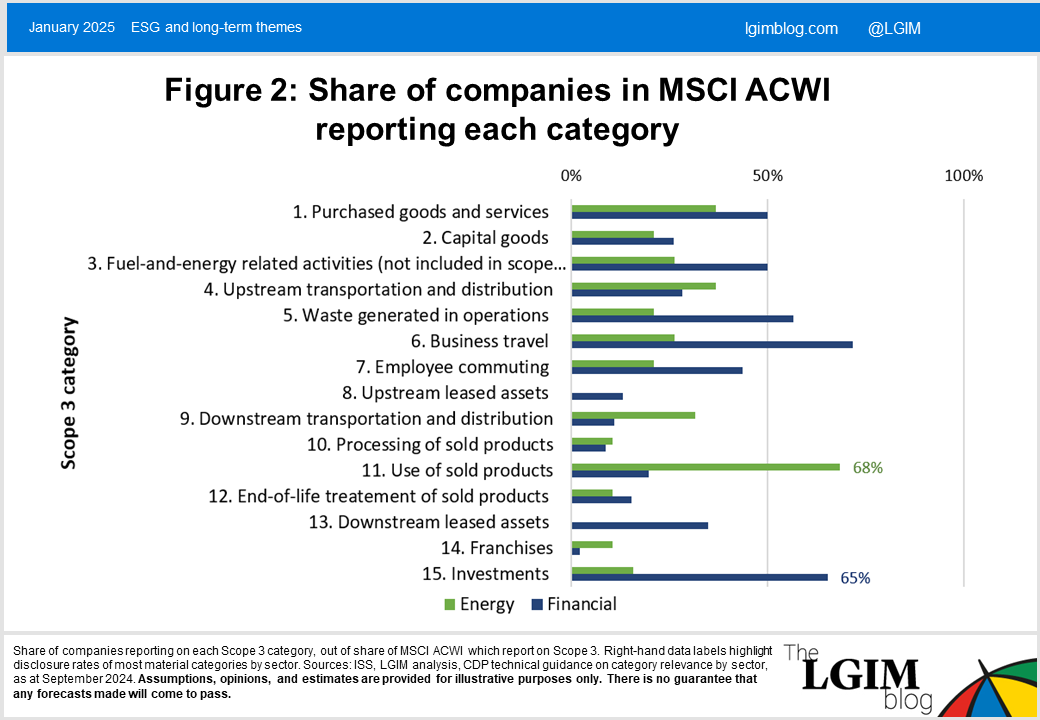

The other main issue with Scope 3 data is that companies who do disclose often exclude material categories. They often do so because of difficulties with measuring upstream and downstream emissions – and the fact that the preeminent carbon accounting framework (the GHG Protocol) allows category exclusions if accurate measurement is not feasible[4]. These exclusions can be seen in the category breakdown of Scope 3 disclosures in Figure 2 below.

Share of companies reporting on each Scope 3 category, out of share of MSCI ACWI which report on Scope 3. Right hand data labels highlight disclosure rates of most material categories by sector. Sources: ISS, LGIM analysis, CDP technical guidance on category relevance by sector, as at September 2024. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

The right-hand side of Figure 3 focuses on the energy and financial sectors, as their emissions are highly concentrated in specific Scope 3 categories. For financials, over 99% of total emissions come from category 15 (investments) and for energy ~81% of total emissions come from category 11 (use of sold products)[5]. However, as shown above, only 65% of financials and 68% of energy companies report their most material categories. Therefore, companies in these sectors who exclude their most material category essentially publish a Scope 3 data point which is meaningless.

The challenge(s) around using Scope 3 data for portfolio decarbonisation targets

These two data issues create serious challenges for investors seeking to make investment decisions based on Scope 3 data. Due to the high prevalence of third-party estimates and incomplete category disclosure, it is hard to discern whether differences between companies are driven by real-world performance or data-related factors.

What’s more, if investors do consider Scope 3 emissions, they could end up discriminating against companies with better disclosure as these tend to have higher reported emissions. Therefore, without careful consideration of the accuracy and completeness of Scope 3 data, investors could have the opposite impact of what they intend.

We also note that even as companies work to decarbonise their value chains, their reported Scope 3 emissions often increase often due to improved disclosure. The MSCI ACWI’s Scope 3 emissions increased by 25% from 2021-2022, while Scope 1 and 2 emissions decreased slightly. Over the next few years, as we expect disclosure to increase, it will remain very difficult to accurately detect real-world decarbonisation trends based on reported Scope 3 emissions.

Focus on improving disclosure, not on-paper decarbonisation…for now

Weighing these challenges, we believe that investors may wish to incorporate Scope 3 data into investment decisions with careful consideration of inaccuracy and estimation bias. Additionally, if clients are monitoring their portfolio’s Scope 3 emissions, they may see increases in reported Scope 3 emissions as disclosure improves.

Over the next several years, we believe investors may benefit from focussing their attention on improving their portfolio’s Scope 3 disclosure – as per the ISSB S2 standard – rather than managing their reported Scope 3 emissions. By improving disclosure, and therefore overall data quality, Scope 3 data could be systematically integrated a wider range of investment decisions in the future.

[1] LGIM analysis as at September 2024, ISS

[2] ISSB, GHG Protocol

[3] Columbia Law

[4] Corporate Value Chain (Scope 3) Standard | GHG Protocol

[5] CDP technical guidance

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.