Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Agriculture risk in the EU’s Sustainable Finance Taxonomy

During the COP26 negotiations, there were reports that an important proposal for the EU Taxonomy was circulating among policymakers. The paper, titled the ‘Complementary climate delegated act’, proposes a number of criteria for agriculture that had been omitted from the delegated act for climate change mitigation and adaptation published in April this year.

Much of the response to the paper has focused on the gas and nuclear sector, including comments from our friends at the UN Principles for Responsible Investment and the Net Zero Asset Owner Alliance. However, and rather worryingly, less attention has been drawn to the suggested proposals for agriculture.

To put the significance of agriculture in context, the sector accounts for a third of global greenhouse gas (GHG) emissions and 10% of the EU’s GHG emissions. It also accounts for over half of the EU’s methane emissions – the second biggest contributor to climate change, with a warming potential 84 times that of CO2. Put simply, the sector plays a key role in the transition if we are to limit global warming to 1.5°C by 2050.

While the paper suggests the Commission use similar criteria for agriculture as proposed in March 2021, it also suggests important concessions. Specifically, it proposes that economic activities will ‘automatically’ qualify if:

i. They fall under the EU’s Common Agricultural Policy (CAP) “eco-schemes and agri-environmental and climate measures”, or

ii. The production system is organic.

A glaring issue with these proposals is that they intend to qualify CAP eco-schemes and organic agriculture without considering the principle of ‘do no significant harm’. The proposals also allow for a qualification loophole, risking weaker criteria being agreed in a CAP reform or on organic farming. Given that organic farming can result in environmental trade-offs, and that CAP reforms have not been hailed for their ambition on tackling climate issues, this is a real risk.

Finally, CAP schemes – the EU’s mechanism for agricultural subsidies – will be decided at the national level. Should EU Taxonomy criteria defer to national CAP implementation, it would result in the same activities being considered sustainable in some countries and not sustainable in others, distorting markets and undermining investors’ trust.

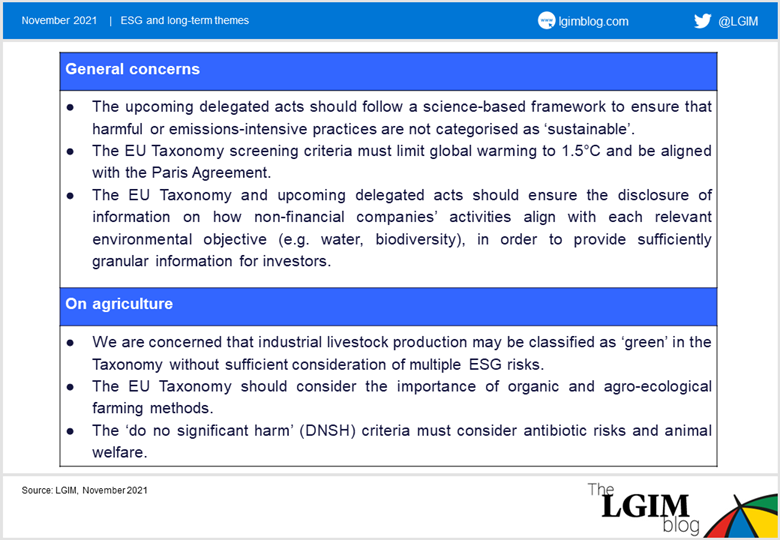

In October, a group of investors, investor representatives and advisers representing $3.5 trillion in assets (including LGIM) expressed concerns over certain elements of the Taxonomy to the EU Commission. The letter highlights the importance of a science-based Taxonomy and of the role of the agricultural sector within it. The key points are listed in the table below.

The full text of the letter is available here

This is certainly not the first time that we have voiced our concern. In March, we wrote to the Commission with recommendations for how Europe can align CAP reforms with the Paris Agreement. In July, the European Court of Auditors found virtually none of the CAP funds attributed to climate action could be shown to be good for the climate.

Whilst the recent proposal may appear to improve EU policy alignment, we believe it would undermine the robustness of the EU Taxonomy if approved and impede investors’ ability to identify and direct capital towards environmentally sustainable activities. In turn, investors would not want to build their investment decision-making on a tool whose scientific credibility is tarnished. This must be avoided by ensuring that the EU Taxonomy uses robust, scientific and evidence-based criteria.

This was co-authored by Helena Wright and Eline Reintjes of FAIRR, an investor network focusing on ESG risks in the global food sector.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.